Iran's Nuclear Pact and Geopolitical Risk in Energy Markets

The Middle East has long been a fulcrum of global energy markets, with Iran's nuclear diplomacy and regional tensions serving as critical drivers of oil price volatility and broader commodity investment dynamics. As the 2025 geopolitical landscape unfolds, the interplay between diplomatic stability, military escalation, and economic sanctions continues to reshape risk profiles for investors. This analysis examines how Iran's nuclear agreements and geopolitical risks influence energy markets and commodity opportunities, drawing on historical precedents and recent developments.

The Nuclear Diplomacy-Price Volatility Nexus

The 2015 Joint Comprehensive Plan of Action (JCPOA) demonstrated how diplomatic agreements can directly alter oil market fundamentals. By lifting sanctions, the deal enabled Iran to increase oil exports by approximately 500,000 barrels per day, contributing to a global oversupply that depressed Brent crude prices by over 20% in 2016[1]. Conversely, the U.S. withdrawal from the JCPOA in 2018 and the reimposition of sanctions disrupted Iranian exports, creating a supply deficit that pushed oil prices to a 3-year high[2].

Recent events underscore this pattern. U.S. military strikes in June 2025, targeting Iranian nuclear infrastructure, initially caused Brent crude prices to surge by 12% due to fears of retaliatory attacks and supply disruptions[3]. However, the long-term impact of such actions remains uncertain. While military force may delay Iran's nuclear ambitions, history shows that diplomacy—such as a potential 2025 nuclear deal—offers a more sustainable path to stability. A new agreement lifting sanctions could inject an additional 1.5 million barrels per day into global markets, potentially depressing prices in an already oversupplied environment[4].

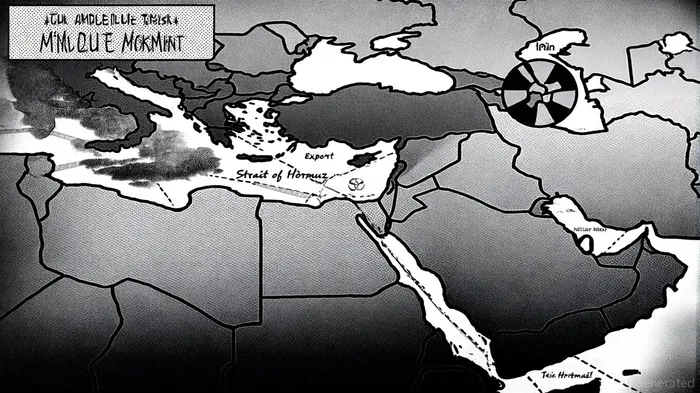

Geopolitical Risks and Commodity Diversification

Beyond oil, geopolitical instability in the Middle East has amplified risks for other commodities. Gold, a traditional safe-haven asset, reached an intraday high of $3,319.10 in May 2025 as investors sought refuge from escalating tensions between Israel and Iran[5]. Analysts project further gains if hostilities persist, given gold's inverse correlation with geopolitical stability[6].

Copper markets have also been affected. The U.S. dollar's strength during periods of risk-off sentiment has pressured copper prices, which fell 8% in June 2025 despite tightening fundamentals[7]. Meanwhile, agricultural commodities face indirect risks through energy-linked inputs. The Strait of Hormuz, a critical chokepoint for 20% of global oil and 40% of urea fertilizer trade, remains vulnerable to disruptions. A 30% closure of this route could push fertilizer prices to decade highs, directly impacting crop production costs[8].

Strategic Investment Considerations

For investors, the key lies in balancing exposure to energy markets with hedging against geopolitical shocks. Diversification into safe-haven assets like gold and high-quality equities is prudent, as historical data shows equities often recover post-conflict volatility[9]. Additionally, the potential for a new Iran deal introduces asymmetric risks: while oil prices could fall further, economic relief for Iran might stimulate demand for industrial commodities like copper and agricultural goods[10].

Conclusion

The Middle East's geopolitical dynamics remain a defining factor in global commodity markets. While diplomatic stability can mitigate price volatility, the region's history of conflict and sanctions underscores the need for adaptive investment strategies. Investors must monitor both the trajectory of nuclear negotiations and the potential for military escalation, as either could trigger sharp shifts in energy and commodity prices. In this environment, a diversified portfolio with exposure to safe-haven assets and energy-linked commodities offers a resilient approach to navigating uncertainty.

Comentarios

Aún no hay comentarios