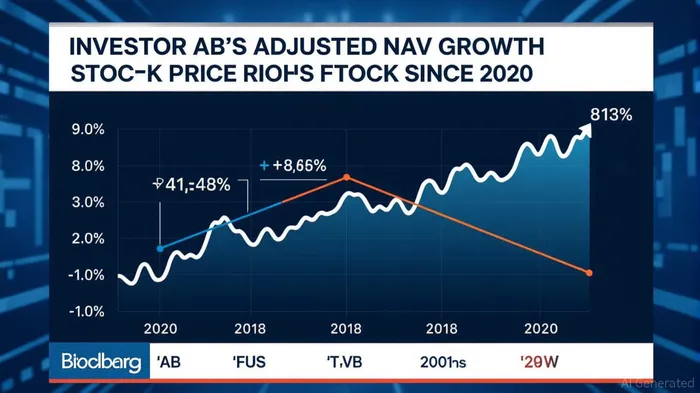

Investor AB's Q3 2024: NAV Growth Outshines Reported Earnings, Highlighting Undervalued Assets

Investor AB's Q3 2024 results reveal a striking disconnect between its adjusted net asset value (NAV) growth and reported net profit, creating an intriguing investment opportunity. While the company's adjusted NAV rose 2% quarter-on-quarter to SEK 317 per share (despite temporary headwinds), its net profit fell 30.5% year-over-year. This divergence underscores the potential for investors to capitalize on undervalued subsidiaries like Mölnlycke and Patricia Industries, whose underlying strength may not yet be reflected in the reported figures.

NAV Growth vs. Reported Earnings: A Tale of Two Metrics

Investor AB's adjusted NAV grew 20% year-on-year in 2024, driven by strong performances across its subsidiaries. However, its reported net profit for Q3 2024 dropped 30.5% compared to the prior year, largely due to currency headwinds and one-time impairments. For instance, the SEK -11.1 billion net loss in Q3 2023 turned into a SEK 12.8 billion profit in 2024, but this improvement was overshadowed by volatility in listed equities and temporary drags from currency fluctuations.

The key distinction lies in how these metrics are calculated. Adjusted NAV incorporates unrealized gains and excludes short-term impairments, while reported earnings reflect realized losses and operating expenses. This gap creates a compelling case for investors to focus on the former, as it better captures the long-term value of Investor AB's portfolio.

Subsidiaries: The Undervalued Engines of Growth

Patricia Industries delivered a 3% quarterly return (7% excluding cash), fueled by organic sales growth of 3% in constant currency. Its flagship subsidiary, Mölnlycke, reported an 8% organic sales expansion, with its Wound Care division surging 10%. Mölnlycke also distributed EUR 300 million to Patricia Industries, signaling strong cash flow generation.

Meanwhile, EQT AB, a key holding, saw its valuation rise 7% in Q3, despite short-term volatility. EQT's integration of Equitrans Midstream and asset sales in Pennsylvania bode well for future debt reduction and profitability.

The listed equities portfolio, however, lagged, with a -4% quarterly return. This underperformance, driven by broader market volatility, likely contributed to the reported net profit decline. Yet, over the full year, listed holdings still delivered an 18% return, suggesting the sector's value may rebound as macroeconomic conditions stabilize.

Why the NAV Is the True Benchmark

The reported NAV of SEK 277 per share (as of September 30, 2024) understates the portfolio's intrinsic value. Adjusted NAV excludes temporary impairments and captures the full potential of subsidiaries like Patricia and EQTEQT--. For example:

- Mölnlycke's 9% sales growth (when including acquisitions) suggests it could outperform even its already strong metrics.

- Patricia Industries' 32% full-year return (excluding cash) highlights the scalability of its operations.

- EQT's 8% annual valuation gain reflects strategic asset management, not just short-term swings.

Currency effects, which penalized reported earnings, are also reversible. A weaker Swedish krona in Q3 compressed foreign-currency gains, but a stabilization or reversal of this trend could boost future results.

Investment Outlook: Buying the Dip

Investor AB's shares trade at a discount to its adjusted NAV, offering a margin of safety. With leverage at just 1.2% and gross cash of SEK 28 billion, the balance sheet is resilient. The proposed dividend of SEK 5.20 per share further rewards investors.

Action Items for Investors:

1. Buy on dips: Use near-term volatility as an entry point, particularly if the krona strengthens or equity markets rebound.

2. Focus on fundamentals: Track Patricia Industries' organic growth and EQT's debt-reduction progress.

3. Monitor macro trends: A stabilization in energy prices or a rebound in healthcare demand could boost Mölnlycke's margins.

Conclusion

Investor AB's Q3 results highlight a temporary earnings stumble against a backdrop of robust NAV growth and subsidiary resilience. The disconnect between adjusted NAV and reported earnings creates an asymmetric opportunity: the risks of near-term volatility are outweighed by the long-term upside of its undervalued assets. For patient investors, this could be a rare chance to buy quality at a discount.

Comentarios

Aún no hay comentarios