Intuitive Surgical's Valuation Dilemma: Structural Risks and the Robotic Surgery Sector's Crossroads

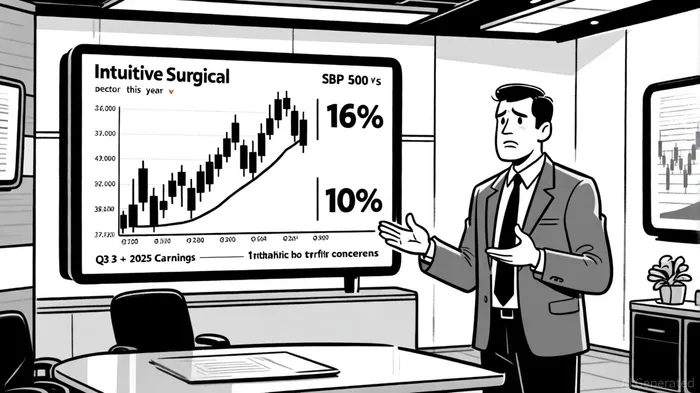

Intuitive Surgical (ISRG) has long been a poster child for innovation in healthcare, its da Vinci Surgical System revolutionizing minimally invasive procedures. Yet, the stock's 16% decline in 2025-lagging the S&P 500's 10% gain-has sparked debate about whether this pullback reflects a compelling entry point or a warning of deeper structural risks. To answer this, investors must weigh the company's robust fundamentals against headwinds in the robotic surgery sector, including slowing adoption, regulatory complexity, and intensifying competition.

Financial Fundamentals: Growth Amid High Valuation

Intuitive Surgical's Q3 2025 earnings report underscored its enduring strength. Global Da Vinci procedures rose 17%, revenue climbed 21% to $2.4 billion, and GAAP net income grew 25%, according to a Monexa analysis. The launch of the Da Vinci 5 system, with 10,000 times the computing power of earlier models, signals a technological leap that could enhance efficiency and procedure volumes, per a GlobeNewswire report. Yet, these gains come against a backdrop of a stratospheric valuation. ISRG's price-to-sales (P/S) ratio of 17.4 and price-to-earnings (P/E) ratio of 61.0 far exceed the S&P 500's 3.3 and 23.9, respectively, as highlighted in a Forbes analysis. Such a premium demands that the company consistently outperform expectations, a tall order in a sector facing structural challenges.

Structural Risks: Cost Barriers and Regulatory Quicksand

The robotic surgery market's growth is being throttled by two critical factors: cost and regulation. A single da Vinci system costs $1.5–$2 million, with maintenance and training adding to the burden, according to Grand View Research. For hospitals, the return on investment hinges on high procedure volumes and favorable reimbursement rates-both of which are under pressure. In the U.S., value-based care models partially offset costs by rewarding outcomes, but in Europe and emerging markets, reimbursement remains fragmented. For instance, Germany lacks standardized payment models, while Latin America sees 68% of robotic procedures paid out-of-pocket, per an iDataResearch report.

Regulatory hurdles further complicate expansion. The EU's Medical Device Regulation (MDR) has imposed stringent CE certification requirements, delaying market entry for new systems, as noted in the Forbes analysis. In the U.S., FDA approvals for advanced robotic platforms often take over 10 months, slowing innovation cycles, Grand View Research finds. Meanwhile, the absence of a legal framework for telesurgery in the EU-a capability that could democratize access-creates uncertainty for long-term growth, a point raised in the Forbes piece.

Competitive Pressures: The Rise of Cost-Effective Alternatives

Intuitive Surgical's dominance-60% global market share in 2024, per Monexa-is being challenged by rivals offering cheaper alternatives. Medtronic's Hugo RAS and CMR Surgical's Versius system aim to reduce upfront costs by 30–66% compared to the da Vinci, Grand View Research reports. In China, local players like MicroPort leverage leasing models to slash initial expenses by 60–70%, according to iDataResearch. These innovations threaten ISRG's recurring revenue model, which relies on high-margin instruments and service contracts.

Is the Pullback a Buying Opportunity?

The current valuation discount reflects justified concerns about these structural risks. However, Intuitive Surgical's 28.5% net income margin and 21.4% year-over-year revenue growth, noted in the Forbes analysis, suggest it remains a formidable player. The company's focus on AI integration and expansion into emerging markets-where Asia-Pacific is projected to grow at 15% annually through 2034, according to the GlobeNewswire report-could unlock new value. For long-term investors, the key question is whether ISRG can maintain its innovation edge while navigating regulatory and competitive pressures.

A compelling entry point would require a significant multiple contraction-say, a P/S ratio closer to 10-to align with sector risks. Until then, the stock's premium reflects both its historical dominance and the market's hope that Intuitive SurgicalISRG-- can overcome structural headwinds. For now, the pullback is a caution sign, not a green light.

Comentarios

Aún no hay comentarios