Is Intuitive Surgical's Premium Valuation Justifiable in Light of Its Growth Prospects and Competitive Edge?

Financial Performance: A Tale of Explosive Growth and Recurring Revenue

Intuitive Surgical's third-quarter 2025 results underscore its dominance in the surgical robotics sector. Revenue surged 23% year-over-year to $2.51 billion, driven by a 20% increase in worldwide procedures and robust system placements according to earnings reports. The da Vinci platform, the company's flagship product, saw procedure growth of 19%, while the newer Ion system exploded by 52%. Free cash flow for the quarter reached $736 million, with $8.4 billion in cash and investments on hand as reported by Seeking Alpha. These figures highlight Intuitive's ability to generate recurring revenue from consumables (instruments and accessories, which account for 60% of revenue) and capitalize on its installed base of 10,763 da Vinci systems as detailed in earnings release.

However, challenges persist. International rollout delays for the da Vinci 5 system and concerns over third-party refurbished instruments have tempered some optimism according to market commentary. Despite these headwinds, the company raised its 2025 procedure growth guidance to 17–17.5%, reflecting confidence in its product pipeline and market penetration as reported by Barron's.

Intrinsic Valuation: Can the Numbers Justify the Premium?

To assess whether Intuitive Surgical's valuation is rational, we turn to discounted cash flow (DCF) analysis. Key inputs include:

- Free Cash Flow (FCF): $736 million in Q3 2025, with capital expenditures projected at $625–675 million for 2025 as reported by Seeking Alpha.

- Growth Rates: Procedure growth of 17–17.5% in 2025, potentially tapering to 10–12% in later years as markets mature.

- Discount Rate: Assuming a 9% weighted average cost of capital (WACC), reflecting the sector's moderate risk profile.

A simplified DCF model suggests that Intuitive's intrinsic value hinges on sustaining high-margin growth. For instance, if the company maintains 12% annual FCF growth for a decade and a 3% terminal growth rate, its intrinsic value would approximate $250–$270 per share. At the time of writing, the stock trades at ~$320, implying a 20–25% overvaluation based on these assumptions according to Seeking Alpha analysis.

Yet, this calculation assumes linear growth and ignores Intuitive's structural advantages. Its 90%+ gross margins on consumables and the network effect of its installed base create a moat that few competitors can match. Medtronic and Johnson & Johnson, for example, operate in more commoditized segments of medtech, where pricing pressures and lower margins constrain valuation multiples according to market data.

Market Optimism vs. Realities: A Double-Edged Sword

The recent 22.5% price surge following Q3 earnings reflects investor enthusiasm for Intuitive's technological edge. The da Vinci 5 system, with its enhanced precision and AI-driven features, has already driven 240 placements in Q3 alone as reported by Barron's. Moreover, the company's pro forma gross margin guidance of 67–67.5% signals disciplined cost management and pricing power as reported by Seeking Alpha.

However, skepticism remains. The Virtus Large Cap Growth SMA portfolio flagged "transitory" challenges, including international rollout delays and sector rotation out of medtech according to market commentary. Additionally, the rise of third-party refurbished instruments could erode Intuitive's consumables revenue over time. While the company has invested in proprietary instrument designs to mitigate this risk, the long-term impact remains uncertain as noted in market analysis.

Competitive Landscape: A High Bar to Clear

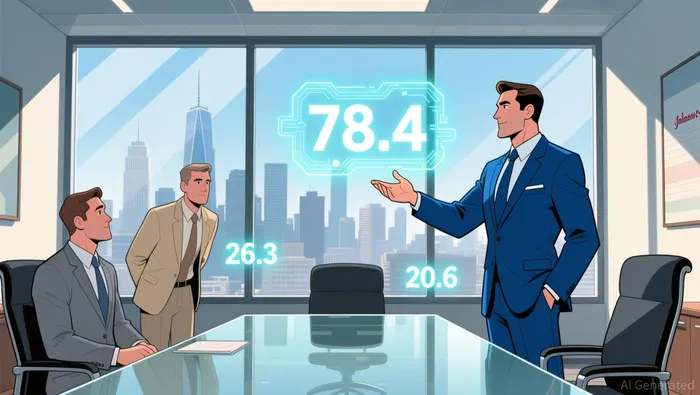

Intuitive Surgical's valuation premium must also be contextualized against its peers. Medtronic and Johnson & Johnson, with their diversified portfolios and defensive cash flows, trade at lower multiples because they lack Intuitive's high-growth, high-margin business model. For example, Medtronic's 26.3 P/E ratio implies a 7% earnings yield, whereas Intuitive's 78.4 P/E implies just 1.3% according to market data. This disparity reflects divergent growth expectations: investors are paying a premium for Intuitive's potential to redefine surgical care, even as they discount the more predictable, albeit slower, growth of its rivals.

Conclusion: A Calculated Bet on the Future of Surgery

Intuitive Surgical's valuation is a double-edged sword. On one hand, its intrinsic metrics-driven by recurring revenue, high margins, and a dominant installed base-justify a premium. On the other, the current P/E ratio of 78.4 demands that the company not only meet but exceed growth expectations for years to come. For long-term investors, the key question is whether Intuitive can sustain its innovation cycle and defend its market share against both traditional competitors and disruptive technologies.

If the company continues to execute on its da Vinci 5 rollout, expands internationally, and mitigates risks from third-party instruments, its valuation may prove justified. However, those who view the current price as a "buy" should prepare for volatility and ensure their investment horizon aligns with the long-term trajectory of surgical robotics adoption. In the end, Intuitive Surgical's story is not just about numbers-it's about betting on a future where precision medicine and AI-driven tools become the new standard of care.

Comentarios

Aún no hay comentarios