InterGlobe Aviation’s Profit Surge and Global Ambition: A Compelling Investment Case?

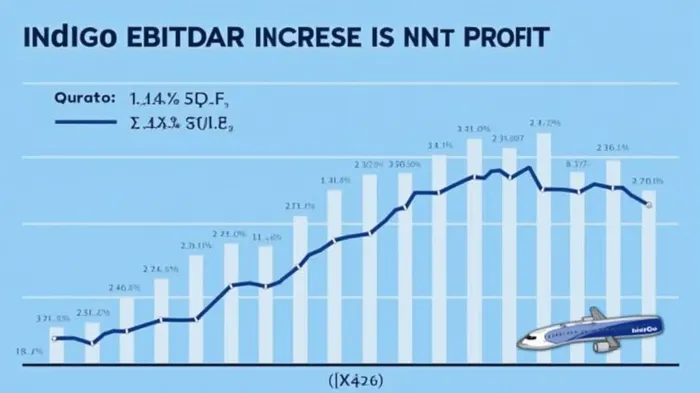

InterGlobe Aviation, operator of India’s leading budget airline IndiGo, has delivered a stellarSTEL-- financial performance in Q4FY25, with a 62% year-on-year (YoY) jump in net profit to ₹3,067.5 crore. This surge, fueled by operational excellence, cost discipline, and a 31.4% EBITDAR margin—up from 24.8% a year ago—underscores the airline’s resilience in a volatile market. With ₹48,170.5 crore in cash reserves, a proposed ₹10/share dividend, and bold plans to expand into Europe, IndiGo presents a compelling investment opportunity. However, investors must weigh its growth ambitions against risks like rising fuel costs and regulatory hurdles.

Operational Efficiency: The Engine of Profit Growth

IndiGo’s Q4 results highlight its mastery of cost leadership. Despite a 19% YoY rise in passengers to 31.9 million, the airline slashed its fuel CASK (cost per available seat kilometer) by 6.6% to ₹1.60, demonstrating superior fleet management and procurement strategies. This efficiency, paired with a 24.3% revenue growth to ₹22,151.9 crore, enabled an EBITDAR margin expansion to 31.4%—a robust indicator of profitability.

The airline’s technical dispatch reliability of 91% and 87.4% on-time performance further validate its operational prowess. These metrics are critical in an industry where delays and cancellations directly erode customer loyalty and revenue.

International Expansion: Tapping into New Markets

IndiGo’s announcement of European market entry marks a bold step beyond its dominant domestic footprint (64.3% market share). By leveraging its low-cost model—which has kept fares 30-40% below full-service competitors—IndiGo aims to capitalize on underpenetrated routes in Europe, where budget travel demand is surging.

The airline’s 434-aircraft fleet, including fuel-efficient A320/321 NEOs, positions it well to serve long-haul routes. Management has also emphasized strategic partnerships and route diversification to mitigate risks from overreliance on domestic demand.

Dividend Potential and Financial Fortitude

With ₹33,153.1 crore in free cash reserves, IndiGo’s proposed ₹10 per equity share dividend—pending shareholder approval—reflects its confidence in liquidity. This payout, if executed, would return ₹7,258 crore to shareholders, rewarding investors for the airline’s post-pandemic recovery.

The investment-grade credit rating (BBB-) and 38.7% YoY cash reserve growth further bolster its financial health. While debt rose 30.3% to ₹66,809.8 crore, the airline’s debt-to-equity ratio remains manageable at 1.3x, supported by ₹5,465.65 share price gains (up 28.95% YTD).

Risks to Consider

- Fuel Cost Volatility: Despite improved fuel efficiency, crude oil prices remain a wildcard. A 10% rise in fuel costs could erode ₹668 crore from annual profits.

- Engine-Related Groundings: Issues with Pratt & Whitney engines on older aircraft—though limited to 3% of the fleet—could disrupt operations.

- Regulatory Hurdles: Entering the EU may face challenges like slot allocation and stringent safety norms.

Why Act Now?

IndiGo’s strong balance sheet, dividend catalyst, and 10-12% YoY capacity growth forecast for FY26 create a virtuous cycle of reinvestment and shareholder returns. With domestic travel demand steady at 87.4% load factor and international ambitions on track, the stock’s 22.2% YTD surge hints at investor optimism.

Conclusion: A Buy with Caution

InterGlobe Aviation’s Q4 results and strategic moves paint a compelling picture of a high-margin, growth-oriented airline poised to dominate both domestic and international markets. While risks like fuel prices and engine issues linger, the airline’s cost discipline, cash reserves, and dividend potential make it a high-conviction buy for investors seeking exposure to Asia’s travel recovery.

The clock is ticking: With a P/E ratio of 12x (vs. peers at 15-18x) and a dividend yield of 1.8%, now may be the time to board this opportunity before the runway runs out.

Comentarios

Aún no hay comentarios