Intel's Strategic Turnaround: Why Skepticism Still Outweighs Optimism for Near-Term Investors

The semiconductor sector is riding a wave of optimism in 2025, fueled by AI-driven demand for high-bandwidth memory (HBM), data center expansion, and advanced manufacturing capabilities. Global revenue is projected to hit $697 billion this year, with AI-related applications alone driving a 70% surge in HBM sales, according to a Q3 2025 industry report. Yet, for IntelINTC-- (INTC), the narrative remains mired in skepticism. Despite aggressive strategic pivots-ranging from foundry ambitions to AI accelerator development-the company's valuation metrics and operational performance continue to raise red flags for near-term investors.

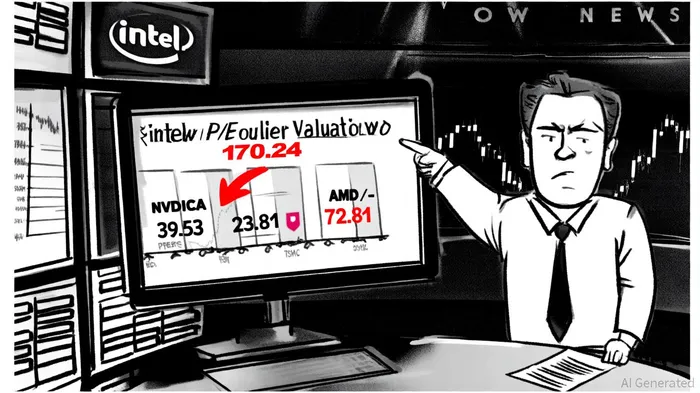

Valuation Realism: A Tale of Disconnection

Intel's forward P/E ratio of 170.24 and EV/EBITDA of 22.09 are staggering, especially when juxtaposed against its peers. NVIDIA trades at a forward P/E of 39.53, while TSMC, the foundry giant, commands a more modest 23.81, per FinanceCharts' PE averages. Intel's EV/EBITDA of 22.09 far exceeds its 3-year (15.29) and 5-year (13.32) averages, signaling a disconnect, per a FinanceCharts EV/EBITDA chart. The company's trailing twelve months (TTM) EBITDA of $9.2 billion, coupled with a -38.64% profit margin, underscores its inability to translate revenue into profitability, according to StockAnalysis statistics.

This valuation disconnect is further amplified by the sector's broader momentum. The average forward P/E for the semiconductor industry is 64.16, reflecting investor confidence in AI-driven growth, per CSIMarket industry P/E data. However, Intel's metrics suggest it is being valued more for potential than performance. With a foundry business still hemorrhaging cash-reporting a $2.9 billion GAAP net loss in Q2 2025-and a client computing segment shrinking year-over-year, the company's ability to justify such lofty multiples remains unproven, according to a Ricentral MarketMinute.

Sector Momentum vs. Execution Gaps

The semiconductor sector's growth is undeniably structural. AI demand has spurred a 30% revenue growth forecast for 2025, with NVIDIA's data center revenue hitting $41.1 billion in Q2 alone, according to that report. TSMC's 30% revenue growth projection and SK Hynix's 40% HBM market share highlight the sector's resilience, per the same report. Yet, Intel's strategic initiatives-while ambitious-lag in execution.

The company's foundry business, a cornerstone of its turnaround plan, is still unprofitable. Despite securing a $5 billion partnership with NVIDIA and an $8.9 billion government-backed equity stake, Intel's foundry division operates at a loss, with operating losses exceeding $3 billion in Q2 2025, as noted in MarketMinute coverage. Analysts like Citi question its ability to compete with TSMC, noting its "money-losing" status and reliance on anchor customers for its 14A process node, according to the Ricentral MarketMinute. Meanwhile, its AI ambitions-centered on Gaudi accelerators and enhanced Xeon processors-face an uphill battle against NVIDIA's dominance in the AI infrastructure space, according to a GPU Wars roundup.

Analyst Sentiment: A Cautionary Outlook

Recent analyst ratings reinforce the skepticism. Of 13 analysts covering Intel in Q3 2025, 10 issued neutral or bearish ratings, with the average 12-month price target at $22.31-a 5.55% drop from prior estimates, according to a Sahm Capital roundup. This cautious stance reflects concerns over Intel's profitability, debt load, and the time required to scale its foundry business. While the company's $20 billion 2025 capital expenditure plan and new manufacturing facilities in Ohio and Arizona signal long-term potential, the near-term investors are left grappling with the reality of declining margins and unmet operational targets, per an Investing.com transcript.

Conclusion: A Long-Term Bet, Not a Quick Win

Intel's strategic initiatives-foundry expansion, AI integration, and domestic manufacturing-position it for long-term relevance in a reshaped semiconductor landscape. However, the near-term outlook remains clouded by valuation overreach, operational losses, and a sector that is outpacing its execution. For investors, the key takeaway is clear: while the sector's momentum is undeniable, Intel's journey from a struggling chipmaker to a profitable growth story will require patience, capital, and a tolerance for risk that many may find unpalatable. Until the company can bridge the gap between ambition and performance, skepticism will likely outweigh optimism.

Comentarios

Aún no hay comentarios