Institutional Confidence in Byline Bancorp (BY): A Strategic Buy for Retail Investors

Byline Bancorp (BY) has long been a sleeper stock in the financial sector, but recent developments suggest it's time for retail investors to take notice. . When heavyweights like BlackRockBLK--, Dimensional Fund Advisors, and Vanguard pile into a stock, it's not just a vote of confidence; it's a signal that the fundamentals are worth a second look. Let's break down why BY could be a strategic buy for those willing to think like the pros.

Institutional Ownership: A Proxy for Quality

Institutional investors don't just follow the crowd—they create it. As of September 2025, , , . The recent buying spree by Boston Partners (adding 643,630 shares in Q2 2025[3]) and T. Rowe Price underscores a growing conviction. These aren't passive bets; they're active statements that BY's management is navigating a challenging interest rate environment with discipline.

But here's the kicker: Insider ownership is equally compelling. , , . When insiders and institutions align, it's a rare alignment of incentives.

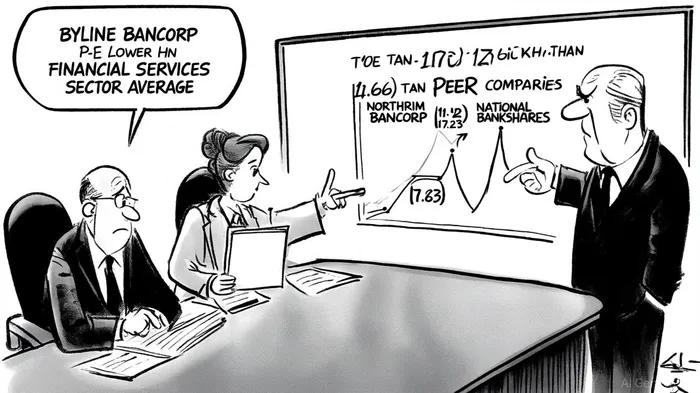

Financials That Beat the Sector

. . At this price, , .

, but it still outperforms the industry average. , . BY's balance sheet is a fortress, .

Risks: Crowded Trade or Catalyst?

Of course, heavy institutional ownership carries risks. If BlackRock, Dimensional, or Vanguard decide to trim their positions, BY's float could shrink dramatically, amplifying volatility. But here's the twist: The same institutions that could sell are also the ones that could buy more. , there's little retail-driven noise to distort the stock's price.

Moreover, KBRA's recent upgrade of BY's senior debt to BBB+[1]—a nod to its “strong earnings capacity and prudent risk management”—should stabilize sentiment. This isn't just a ratings game; it's a real-world signal that BY's creditworthiness is improving, which could attract more institutional capital.

The Bottom Line: Buy the Dip, Not the Hype

For retail investors, BY represents a rare opportunity to piggyback on institutional wisdom. Its undervalued metrics, conservative leverage, and insider alignment make it a compelling case for long-term growth. Yes, the stock could face short-term headwinds if interest rates spike or loan defaults rise, but the fundamentals are robust enough to weather those storms.

In a market where “buy the dip” has become a cliché, BY's institutional backing is the kind of concrete evidence that separates hype from opportunity. As the old adage goes, “When the pros are in, it's time to follow.”

Comentarios

Aún no hay comentarios