Inspirato Inc's Capital Restructuring: Strategic Flexibility and Risk Mitigation in a High-Stakes Merger

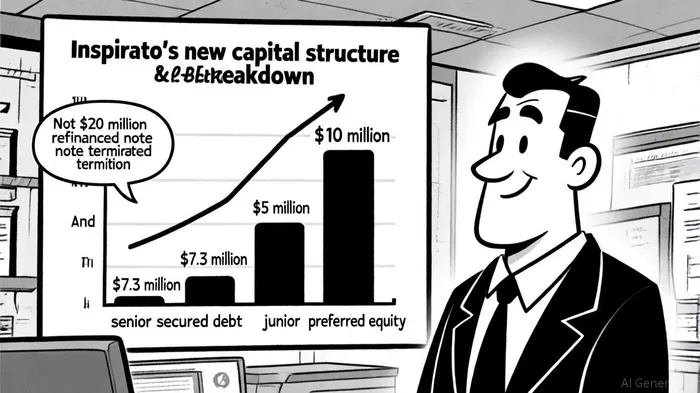

Inspirato Inc. (NASDAQ: ISPO) has embarked on a high-stakes financial maneuver to restructure its capital and facilitate a merger with Buyerlink, Inc. By securing $22 million in financing—comprising $10 million in senior secured debt, $5 million in junior debt, and $7.3 million in preferred equity—the company aims to terminate its $20 million 8% Senior Secured Convertible Note with Oakstone Ventures (via Capital One) and clear the path for the merger [1]. This strategic move underscores the company's focus on reducing leverage, avoiding costly termination risks, and enhancing operational flexibility in a volatile market.

Capital Structure and Leverage: A Delicate Balancing Act

Inspirato's debt-to-equity ratio for Q2 2025 stood at -2.95, reflecting a stockholder deficit and negative equity [2]. This metric, which has fluctuated between -2.86 and -3.16 over recent quarters, highlights the company's precarious financial position. The new financing package is designed to stabilize this imbalance by refinancing the existing Capital One note and reducing reliance on high-cost debt. According to a report by Nasdaq, the combined company is expected to maintain a “prudent and manageable” debt-to-EBITDA ratio post-merger, a critical factor for sustaining profitability in the luxury travel sector [3].

The CEO, Payam Zamani, emphasized that the revised capital structure would “enhance operational freedom and strengthen the profitability profile,” enabling reinvestment in growth initiatives [1]. This aligns with broader industry trends where companies in the travel and leisure sector prioritize liquidity and flexibility to navigate economic uncertainties.

Avoiding Termination Risks: A Strategic Priority

The termination agreement with Oakstone Ventures is a pivotal element of Inspirato's strategy. By paying $20 million to retire the 2023-issued note upon the merger's closing, the company avoids potential reverse termination fees that could arise if the deal falters. As outlined in the August 15, 2025, agreement, failure to complete the merger by December 15, 2025, would allow Capital One to sell or transfer the note, with InspiratoISPO-- obligated to cooperate [4]. This contingency underscores the urgency of securing the $22 million in financing, which includes non-binding term sheets that provide a buffer against liquidity constraints.

The financial commitment also mitigates the risk of a reverse termination fee—a costly scenario where the company would pay Oakstone Ventures to exit the agreement. By proactively refinancing the note, Inspirato reduces its exposure to such fees and aligns its capital structure with merger requirements. This approach reflects a calculated risk management strategy, prioritizing short-term financial discipline to unlock long-term value.

Operational Implications: Growth vs. Debt Servicing

While Inspirato's negative equity remains a concern, the new capital structure is expected to alleviate pressure on cash flow. The $22 million infusion will not only cover the $20 million note payoff but also provide additional resources for operational investments. A report by Panabee notes that the merger with Buyerlink is anticipated to streamline Inspirato's business model, leveraging synergies in the luxury travel marketplace [5].

However, the company's ability to sustain profitability will depend on its capacity to convert these structural improvements into revenue growth. With a history of negative equity and high leverage, Inspirato must demonstrate that its debt-to-EBITDA ratio can improve post-merger. The CEO's optimism about “greater financial flexibility” hinges on the successful integration of Buyerlink and the effective utilization of the new capital [3].

Conclusion: A High-Risk, High-Reward Play

Inspirato's capital restructuring is a bold but necessary step to position itself for growth. By terminating the Oakstone Ventures note and securing diversified financing, the company addresses immediate liquidity risks while aligning with merger objectives. The success of this strategy, however, remains contingent on the timely closure of the Buyerlink deal and the ability to translate reduced leverage into operational efficiency. For investors, the key metrics to monitor will be the debt-to-EBITDA trajectory, merger integration progress, and the company's capacity to generate positive equity.

Inspirato's journey illustrates the delicate balance between strategic flexibility and financial prudence in a high-stakes merger. If executed successfully, the restructuring could transform the company into a more resilient player in the luxury travel sector.

Comentarios

Aún no hay comentarios