Inflation Pivot Fuels Sector Rotation: Navigating the S&P 500's Trajectory in a New Rate Environment

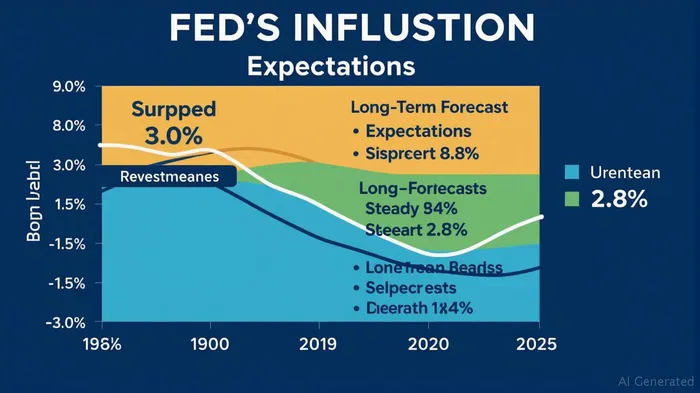

The Federal Reserve's June 2025 inflation survey reveals a critical shift: short-term inflation expectations have dipped to 3.0%, while long-term forecasts remain anchored between 3.0% and 2.6%. This divergence creates a unique opportunity for investors to pivot toward rate-sensitive sectors such as technology and consumer discretionary, even as risks from trade tensions and labor market resilience linger. Here's how to position portfolios for this evolving landscape.

The Inflation Pivot and Its Implications

The New York Fed's data highlights a key trend: consumers now anticipate slower price increases for essentials like gas and food, though fears of rising rents and medical costs remain elevated. Meanwhile, the Federal Open Market Committee (FOMC) projects PCE inflation to fall to 2.0% in the long term, aligning with its targetTGT--. This stabilization reduces the urgency for further rate hikes, creating a tailwind for sectors sensitive to borrowing costs.

Importantly, labor market resilience—voluntary job separations down 1.2 percentage points to 19.4%—suggests wage pressures are moderating, reinforcing the Fed's gradual easing path. However, the income/spending gap is widening: median one-year income growth stagnates at 2.45%, while inflation expectations for essentials like rent (9.1%) and medical care (9.3%) remain stubbornly high. This creates a dual challenge: households may rely more on credit to sustain spending, while companies face margin pressures in cost-sensitive sectors.

Rate-Sensitive Sectors: Tech and Consumer Discretionary Lead the Charge

The decline in short-term inflation expectations has already fueled a rotation into growth-oriented sectors. Here's where to focus:

Semiconductors: The AI Infrastructure Play

The tech sector, particularly semiconductors, is primed to benefit from lower rates and rising demand for AI-driven infrastructure. reflects this dynamic, with its AI chip sales surging 60% year-over-year. Firms like AMDAMD-- and IntelINTC--, which are expanding data center and cloud capabilities, also stand to gain as companies invest in generative AI tools.

Software: Subscription Models Thrive

Software companies with recurring revenue models—think AdobeADBE--, MicrosoftMSFT--, and Palantir—are insulated from near-term economic volatility. Their valuations, while elevated, are justified by steady cash flows and AI-driven growth. shows outperformance of 30% year-to-date, driven by enterprise adoption of AI platforms.

Consumer Discretionary: Service Over Goods

While goods-based retailers (e.g., WalmartWMT--, Target) face margin pressures from tariff-driven input costs, service-oriented companies like StarbucksSBUX-- and PelotonPTON-- are benefiting from stable discretionary spending. These firms leverage subscription models or experiential offerings, reducing sensitivity to inflation spikes.

Risks: Tariffs and Labor Market Resilience

The path to S&P 500 gains isn't without obstacles. President Trump's threatened 25% tariffs on Japanese and South Korean imports—now delayed until August—could disrupt supply chains and push input costs higher. shows a 10% valuation contraction if tariffs materialize.

Meanwhile, labor market resilience—unemployment expectations at 39.7%, a 5-year low—could delay the Fed's pivot to cuts. A stronger-than-expected jobs report or wage acceleration could force the central bank to pause easing, denting tech multiples.

Defensive Hedges: Utilities and REITs861104-- for Stability

To balance growth bets, allocate 20-25% of portfolios to defensive sectors insulated from rate and trade risks. Utilities, with their regulated earnings and dividend yields averaging 3.2%, offer ballast. shows a 15% underperformance but far less volatility.

REITs, particularly industrial and data center-focused names like EquinixEQIX--, benefit from low rates and rising corporate demand for storage and logistics space. Their dividend yields (4.1% average) and inflation-hedging properties make them a compelling alternative to bonds.

Strategic Recommendations

- Overweight Tech and Consumer Services: Target semiconductor leaders (NVIDIA, AMD), cloud-software firms (Microsoft, Adobe), and service-based consumer plays (Starbucks, Peloton).

- Underweight Tariff-Exposed Sectors: Avoid industrials and discretionary goods stocks until trade negotiations clarify.

- Hedge with Utilities and REITs: Use SPDR Utilities ETF (XLU) and Vanguard Real Estate ETF (VNQ) for downside protection.

- Monitor the Fed's September Policy Meeting: A cut or hawkish pivot will redefine sector leadership—stay agile.

Conclusion: A Balanced Approach to the 6,100 Target

Wall Street's median 2025 year-end target of 6,100 for the S&P 500 reflects cautious optimism. Achieving this will require navigating inflation's dual dynamics: falling short-term pressures and lingering long-term risks. Investors who focus on secular growth in tech and services, while hedging with defensive assets, are best positioned to capitalize on this pivot. As always, stay vigilant to tariff deadlines and labor market signals—they could redefine the trajectory.

Nick Timiraos

July 7, 2025

Comentarios

Aún no hay comentarios