Indian IT Sector's Fragile Equilibrium: Navigating H-1B Policy Shifts and Regulatory Uncertainty

The Indian IT sector, long a linchpin of global technology outsourcing, now faces a precarious crossroads. For decades, firms like Tata Consultancy Services (TCS), InfosysINFY--, and HCLTech thrived on a model predicated on cost arbitrage, U.S. market dominance, and the H-1B visaV-- program. But recent policy shifts under the Trump administration—most notably a fivefold increase in H-1B visa fees to $100,000 per worker—have exposed the fragility of this model. The implications for stock valuations, operational strategies, and long-term profitability are profound.

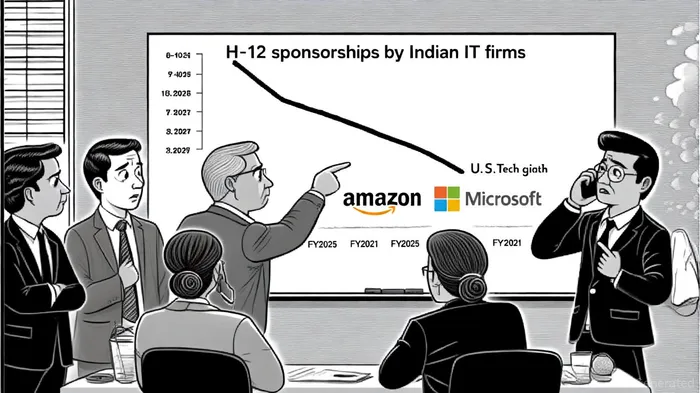

Strategic Shifts in H-1B Reliance

Indian IT firms have begun to recalibrate their dependence on the H-1B program. Between FY2021 and FY2025, sponsorships dropped by nearly 46%, with TCS reducing its filings from 10,525 to 5,505 and Infosys shrinking its U.S. onsite workforce mix from 30% to 24% through nearshoring and automation[4]. HCLTech, meanwhile, has reported that 80% of its U.S. workforce now comprises local hires[2]. These adjustments reflect a pragmatic response to stricter immigration policies and rising costs, but they also signal a departure from the traditional “offshore-onsite” delivery model that underpinned the sector's growth.

The shift is not without trade-offs. Automation and nearshoring require upfront capital expenditures and may delay project timelines, while local hiring in the U.S. competes with a tight labor market. For firms like WiproWIT-- and CognizantCTSH--, which have historically relied on H-1B deployments for high-margin consulting roles, the margin erosion from these changes could be acute[3].

Financial Impact of Policy Changes

The $100,000 H-1B fee hike has already triggered a seismic financial shock. For the top Indian IT firms, combined visa costs could surge from $13.4 million to $1.34 billion annually—a burden equivalent to 10% of their FY2025 net profits[1]. Smaller firms, with less diversified revenue streams, face even steeper challenges. The immediate market reaction was telling: Infosys and Wipro's American Depository Receipts (ADRs) fell by 3.41% and 2.10%, respectively, following the policy announcement[3]. Analysts estimate a 6–7% margin erosion industry-wide, with mid-sized firms bearing the brunt[5].

The fee hike also threatens to disrupt client relationships. U.S. clients, already pressuring IT firms for cost reductions, may demand contract renegotiations or service re-scoping to offset the added costs[1]. This dynamic could accelerate the shift toward offshore delivery, but it risks alienating clients who value onshore collaboration for complex projects.

Regulatory Risks and Legislative Threats

Beyond the H-1B fee, the Indian IT sector faces a broader regulatory onslaught. The proposed HIRE Act, which would impose a 25% excise tax on outsourcing payments to foreign entities, could add up to 46% in costs when combined with state taxes[1]. For firms deriving 60% of their revenue from the U.S., this would erode cost arbitrage advantages and force a reevaluation of pricing models[4].

Compounding these risks are proposals to limit H-1B visas to 15% of a firm's U.S. workforce and enforce “local hiring mandates” for every H-1B worker[1]. Such measures would further constrain Indian IT firms' ability to deploy specialized talent, while the RESTRICT Act's focus on national security reviews could disrupt supply chains involving sensitive technologies[1].

Mitigation Strategies and Future Outlook

To navigate this turbulence, Indian IT firms are pivoting toward AI-driven automation, global capability centers (GCCs), and onshore expansion. TCS and Infosys have accelerated investments in AI and machine learning to reduce labor intensity, while HCLTech and Tech Mahindra are expanding U.S. delivery hubs to avoid tariffs[5]. These strategies, however, require significant capital and time to yield returns.

For investors, the key question is whether these firms can adapt quickly enough to offset regulatory headwinds. Diversification into emerging markets—such as Southeast Asia and the Middle East—offers a partial hedge, but the U.S. remains indispensable. The sector's resilience will ultimately depend on its ability to innovate beyond traditional outsourcing and embrace value-added services like cloud integration and AI consulting.

Conclusion

The Indian IT sector's vulnerability to U.S. policy shifts underscores a broader truth: globalization's benefits are increasingly contingent on political will. For now, the sector is adapting through cost optimization and technological reinvention. But as regulatory risks mount, investors must weigh not just short-term margin pressures but the long-term viability of a business model built on cross-border labor arbitrage. The path forward demands agility, but in an era of protectionism, even agility has its limits.

Comentarios

Aún no hay comentarios