U.S.-India Trade Tensions and Geopolitical Risk in Emerging Markets

The U.S.-India trade dispute, now at a critical juncture as the August 1, 2025, deadline looms, is reshaping global supply chains and investor strategies in Asia. President Trump's imposition of 20%-25% tariffs on Indian exports—framed as a tool to address the $45 billion U.S. trade deficit—has triggered volatility in the Indian rupee, foreign portfolio outflows, and a recalibration of capital flows across emerging markets. Yet, this geopolitical chess game is not merely a bilateral issue; it is a harbinger of broader shifts in global trade dynamics, with profound implications for investors navigating Asia's growth engines.

The Indian Dilemma: Tariffs, Currencies, and Strategic Autonomy

India's refusal to fully align with U.S. positions on Russia's war in Ukraine has made it a target of Trump's “Liberation Day” trade policies. The proposed tariffs, which could hit 40% on pharmaceuticals and textiles, have already pushed the Indian rupee to a five-month low of 87.51 against the dollar. This devaluation reflects not just trade uncertainty but a deeper geopolitical tension: India's strategic pivot toward energy security through Russian oil (a $56 billion purchase in Q4 2024) has been weaponized by the U.S. as leverage in trade negotiations.

For investors, the immediate risks are clear. India's manufacturing and agricultural sectors face exposure to retaliatory measures, while the rupee's fragility adds pressure on corporate earnings and debt sustainability. However, India's “Atmanirbhar Bharat” (Self-Reliant India) initiative, which has spurred domestic manufacturing in semiconductors and solar energy, offers a counterbalance. The country's FDI inflows reached $81.04 billion in FY 2024–25, a 14% increase, as global firms seek to diversify away from China.

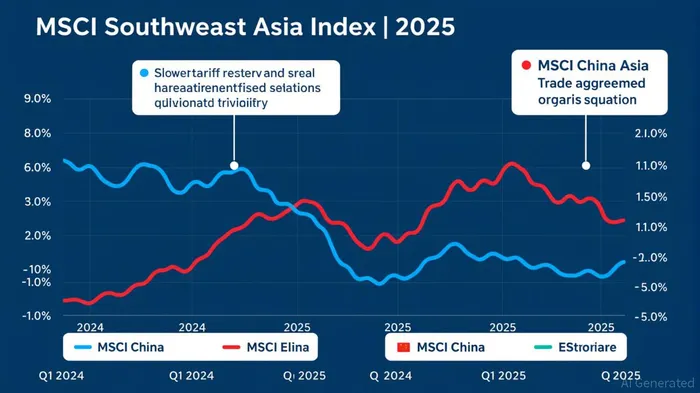

The Asian Reallocation: Southeast Asia's Rise and China's Resilience

While India grapples with U.S. tariffs, Southeast Asia has emerged as a beneficiary of trade reallocation. Vietnam's recent trade agreement with the U.S., setting tariffs at 20%, has stabilized investor expectations, while Indonesia and Malaysia are attracting capital for their lower labor costs and growing industrial bases. The MSCIMSCI-- Southeast Asia Index, up 12.7% year-to-date in Q2 2025, reflects this shift, with copper demand from the region rising as U.S. manufacturers diversify supply chains.

China, despite facing a 104% U.S. tariff on its exports, has shown unexpected resilience. The MSCI China Index rose 17.3% in Q2 2025, buoyed by government stimulus and trade negotiations. However, internal challenges—such as deflation and a debt-laden property sector—remain a drag. The yuan's appreciation against the dollar, now at 7.2, has further complicated China's position as a manufacturing hub.

Strategic Implications for Investors: Diversification and Geopolitical Hedging

The U.S.-India trade dispute underscores a broader realignment of global supply chains. Investors must now balance optimism about India's long-term growth potential with caution over short-term volatility. Diversifying across sectors and geographies—allocating capital to Vietnam's manufacturing or Indonesia's raw materials—can mitigate risks.

- Sectoral Diversification: India's services sector (19% of FDI inflows in 2024–25) remains a stronghold, particularly in IT and business process outsourcing. Meanwhile, Southeast Asia's industrial and commodity sectors offer exposure to non-U.S. demand.

- Currency Hedging: The Indian rupee's volatility and the yuan's appreciation highlight the need for currency diversification. Exposure to the Vietnamese dong or Indonesian rupiah could offset U.S. dollar risks.

- Geopolitical Awareness: Trade policy is increasingly a tool of diplomacy. A U.S.-India agreement could unlock $500 billion in bilateral trade by 2030, while a breakdown risks retaliatory tariffs and capital shifts to other Asian markets.

Conclusion: Navigating the New Trade Order

The U.S.-India trade tensions are a microcosm of the broader U.S.-China rivalry and the reconfiguration of global trade. For investors, the key lies in agility and deep regional expertise. While India's strategic autonomy and domestic reforms present long-term opportunities, the near-term risks of tariffs and geopolitical friction require careful hedging. Southeast Asia's growing role as a manufacturing hub and China's technological advancements in AI and EVs offer complementary opportunities.

As the August 1 deadline approaches, the outcome of U.S.-India negotiations will be a pivotal determinant of market stability. In a world where trade policy is as much diplomacy as economics, investors must remain attuned to both the macroeconomic currents and the geopolitical undertows shaping Asia's growth engines.

Comentarios

Aún no hay comentarios