Income-Generating ETFs in a Low-Yield Environment: Evaluating JPMorgan U.S. Research Enhanced Large Cap ETF's Dividend Consistency

In a world where traditional fixed-income assets struggle to outpace inflation, income-focused investors are increasingly turning to equities and exchange-traded funds (ETFs) to supplement their returns. The JPMorganJPM-- U.S. Research Enhanced Large Cap ETF (JUSA) has emerged as a focal point for such investors, particularly after its recent quarterly distribution of $0.1521 per share on September 23, 2025[3]. This payout, while modest, raises critical questions about the fund's dividend consistency and its strategic positioning in a low-yield environment.

The Low-Yield Dilemma and the Role of ETFs

For decades, U.S. Treasury yields and corporate bond returns have languished near historic lows, forcing income-seeking investors to stretch for yield in riskier corners of the market. ETFs, particularly those targeting large-cap equities, have become a go-to solution. Large-cap stocks, while not traditionally high-yield, offer the stability of established companies and the potential for dividend growth. However, JUSA's performance highlights the challenges of relying on such vehicles for consistent income.

JUSA's Dividend Track Record: A Mixed Bag

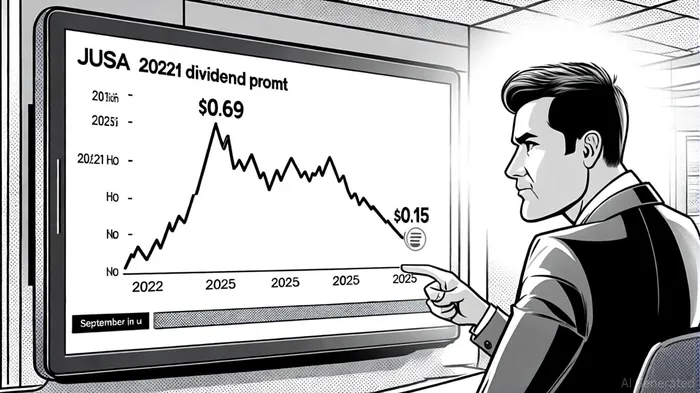

JUSA's dividend history over the past four years reveals a pattern of volatility rather than consistency. According to data from DividendSpot, the ETF has issued four dividend payments since 2021, with an average payout of $0.31 per share[3]. The highest recorded payout was $0.69 per share, starkly contrasting with the recent $0.1521 distribution[3]. This disparity suggests a lack of predictable growth in dividend yields, which is a red flag for income-focused investors.

The trailing twelve-month (TTM) dividend yield of 0.19%[2] further underscores JUSA's limitations. For context, the S&P 500's average dividend yield hovers around 0.7% as of 2025[1]. While JUSA's portfolio of large-cap stocks may offer exposure to high-growth companies, its dividend returns fall far short of traditional benchmarks.

Strategic Positioning: Growth vs. Income

JUSA's recent $0.1521 payout, announced on September 22, 2025[3], appears to align with a quarterly distribution schedule. However, this regularity is undermined by historical inconsistencies. For instance, the fund's dividend growth rate has been negative over the past three years, with a -45.42% decline[3]. A closer look at the data reveals a sharp drop in payouts: from $0.282 per share in December 2021 to $0.689 per share in February 2022[3], followed by a steep decline to $0.11 per share in June 2025[1]. Such volatility complicates long-term planning for investors seeking stable income streams.

The fund's strategy—focused on large-cap U.S. equities—prioritizes capital appreciation over dividend growth. This is evident in its low yield and the absence of consecutive years of dividend increases[3]. While large-cap stocks can offer defensive qualities, JUSA's dividend profile suggests it is not optimized for income-focused investors.

The Bigger Picture: Alternatives and Considerations

For investors in a low-yield environment, JUSA's performance underscores the importance of diversification. While the ETF's recent payout may signal a return to quarterly distributions, its historical volatility and low yield suggest it should not be the cornerstone of an income portfolio. Alternatives such as high-yield corporate bond ETFs or real estate investment trusts (REITs) may offer more attractive returns, albeit with higher risk.

Moreover, JUSA's strategic positioning as a large-cap growth vehicle means its value lies in capital appreciation rather than income generation. Investors must weigh this against their risk tolerance and income needs.

Conclusion

The JPMorgan U.S. Research Enhanced Large Cap ETF's recent quarterly distribution of $0.1521 per share[3] is a modest signal of its dividend consistency, but one that must be viewed in the context of a broader, inconsistent history. With a TTM yield of 0.19%[2] and a negative three-year growth rate[3], JUSA is not a reliable source of income for investors seeking stability. In a low-yield environment, this ETF should be evaluated as a growth-oriented holding rather than a dividend play. For income-focused investors, the lesson is clear: prioritize assets with proven track records of consistent and growing payouts.

Comentarios

Aún no hay comentarios