Implications of PDVSA's Legal and Financial Turmoil on Gold Reserves and Sovereign Debt Markets

The legal and financial turmoil surrounding Venezuela's state-owned oil giant, PDVSA, has escalated into a systemic risk for emerging market debt and global gold markets. As the U.S. government intervenes in PDVSA's 2020 bondholder disputes and the Citgo auction process, the interplay between sovereign debt vulnerabilities, gold reserve depletion, and contagion risks is becoming increasingly pronounced. For investors, the implications demand a strategic reevaluation of asset allocation in emerging markets and precious metals.

PDVSA's Legal Quagmire and Sovereign Debt Contagion

PDVSA's 2020 bonds, issued under the Maduro regime, remain at the center of a legal storm. The U.S. government has affirmed its recognition of Venezuela's 2015 National Assembly as the legitimate authority, which has repeatedly declared the 2020 bonds invalid under Venezuelan law[1]. This stance has emboldened bondholders to pursue litigation in New York courts, seeking to protect their claims against Citgo, PDVSA's U.S. subsidiary valued at $13 billion[3]. Meanwhile, a $7.4 billion bid for Citgo's parent company, PDV Holding, by a group led by Gold Reserve has been recommended as the auction winner—but it excludes any obligation to pay bondholders[4]. This omission has triggered objections and potential injunctions, stalling the auction process and amplifying uncertainty for creditors.

The U.S. District Court for the District of Delaware, overseeing the auction, faces a delicate balancing act. A recent ruling by Judge Katherine Polk Failla upheld the validity of the 2020 bonds, complicating the auction's timeline and reinforcing bondholders' claims[1]. This legal limbo underscores a broader issue: PDVSA's debt crisis is no longer confined to Venezuela. As a key player in global oil markets, its instability risks spillover effects. A study by the OECD notes that rising sovereign risk—measured by credit default swap (CDS) spreads—correlates with declines in both local and foreign stock markets, with an average 0.027% drop in foreign markets[2]. If PDVSA's debt defaults cascade into broader emerging market defaults, the contagion could destabilize regions already grappling with high debt-to-GDP ratios, such as Argentina and Colombia[5].

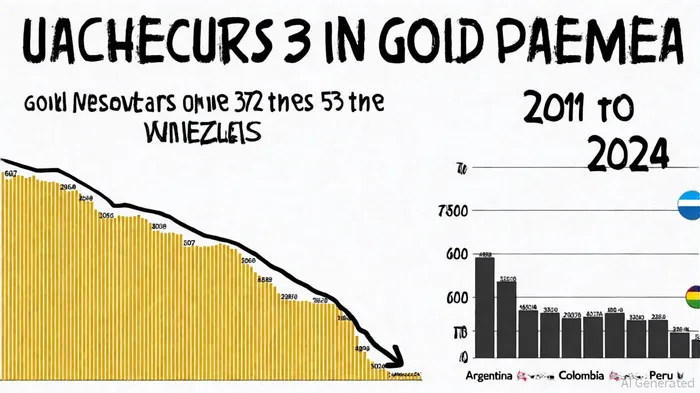

Venezuela's Gold Reserve Depletion: A Systemic Red Flag

Venezuela's gold reserves have plummeted from 372.93 tonnes in 2011 to 53 tonnes in 2024—a 13% drop in 2024 alone[6]. This depletion, driven by economic collapse, U.S. sanctions, and the government's use of gold as collateral for loans, signals a loss of fiscal credibility. Gold, traditionally a safe-haven asset, now reflects Venezuela's deepening crisis. The Central Bank of Venezuela's dwindling reserves exacerbate vulnerabilities in emerging markets, where gold serves as a critical stabilizer for trade balances and foreign exchange[6].

The decline is part of a global trend: central banks are increasingly prioritizing gold over U.S. Treasuries. Under Basel III regulations, gold has been reclassified as a Tier 1 reserve asset, allowing banks to count it at 100% of its market value toward core capital[2]. This shift reflects waning confidence in the dollar, particularly as geopolitical tensions and rising global debt—now $324 trillion—heighten refinancing risks[3]. For countries like Venezuela, the loss of gold reserves compounds their exposure to capital outflows and currency depreciation, creating a feedback loop of instability.

Tactical Repositioning: Gold and Debt Hedging Strategies

The PDVSA saga and Venezuela's gold depletion present a compelling case for tactical asset reallocation. Investors should consider the following strategies:

Gold as a Hedge Against Sovereign Risk: With central banks adding 1,000 metric tons of gold annually and 43% planning further purchases[3], physical gold offers a buffer against currency devaluation and geopolitical shocks. The reclassification of gold as a Tier 1 asset under Basel III further validates its role in portfolios.

Selective Exposure to Emerging Market Debt: While high-yield emerging market bonds remain volatile, opportunities exist in countries with manageable debt levels and structural reforms. However, investors must avoid jurisdictions with heavy foreign-currency debt, such as Argentina and Peru, which face acute refinancing risks[5].

Shorting PDVSA-Linked Instruments: Given the legal uncertainties and default risks, short positions in PDVSA bonds or Citgo auction-related derivatives could capitalize on prolonged volatility. However, this requires close monitoring of U.S. court rulings and sanctions developments.

Diversification into Commodity-Linked Assets: Beyond gold, investors might explore copper or lithium, which are less correlated with sovereign debt cycles and benefit from green energy transitions.

Conclusion: Navigating a Fractured Landscape

PDVSA's legal battles and Venezuela's gold reserve collapse are not isolated events but symptoms of a broader systemic fragility in emerging markets. As sovereign debt vulnerabilities and global financial volatility converge, investors must adopt a dual strategy: hedging against contagion through gold and selectively reallocating to resilient emerging market assets. The coming months will test the resilience of both PDVSA's creditors and global markets, but those who act decisively now may position themselves to weather—and profit from—the turbulence ahead.

Comentarios

Aún no hay comentarios