Implications of Deutsche Bank's Growth Downgrade for German Equity and Sectoral Exposure

The recent downgrade of Deutsche Bank's stock by Goldman Sachs to Neutral from Buy-citing a "broadly fair" valuation-has sent ripples through German equities and European markets, according to Investing.com. This move follows a 92% plunge in the bank's Q4 2024 net profit to €106 million, driven by litigation costs, higher loan losses, and strategic uncertainties, as detailed in a CTOL report. While Deutsche Bank's leadership remains optimistic about achieving a 10%+ return on tangible equity (RoTE) by 2025, the downgrade underscores growing investor skepticism about its ability to navigate structural challenges in the European banking sector, according to a Fitch update.

Structural Weaknesses and Sectoral Risks

Deutsche Bank's struggles are emblematic of broader risks facing Germany's economy. The bank's exposure to the automotive sector, already reeling from a slow transition to electric vehicles and U.S. tariff threats, has been flagged as a "growing risk" in a MarketsWatchers outlook. German automakers, including Daimler and BMW, face margin compression from supply chain disruptions and competition from Chinese EV manufacturers. This sectoral vulnerability extends to Deutsche Bank's corporate lending portfolio, which could suffer as borrowers grapple with declining profitability.

Similarly, the commercial real estate sector-a historical strength for German banks-has shown signs of fragility. While some stabilization has occurred, Deutsche Bank's previous warnings about this sector highlight the lingering risks of overleveraged borrowers and shifting demand dynamics. These sectoral headwinds, combined with Germany's projected 0.5% GDP growth in 2025 (per a DB Research note), paint a picture of a structural slowdown rather than a cyclical downturn.

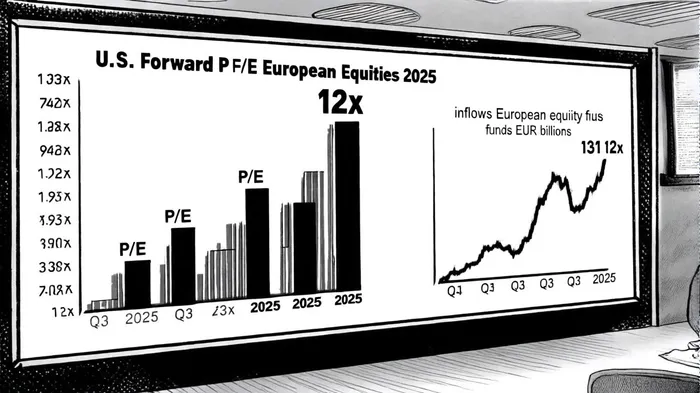

Strategic Reallocation in European Equities

Amid these challenges, investors are recalibrating their European equity exposure. Deutsche BankDB-- itself has advocated for a reallocation from U.S. to European stocks, citing favorable valuations and improving macroeconomic conditions in the Eurozone, per Proactive Investors. European equities, represented by the STOXX 600, trade at a forward P/E of 12x-nearly eight points lower than the U.S. benchmark-and offer higher dividend yields (3.3% vs. 1.3%). This valuation gap has attracted capital inflows, with European equity funds receiving €131 billion in Q2 2025 alone, according to Morningstar data.

The reallocation is not merely a valuation play. Structural shifts, including Germany's €500 billion fiscal stimulus for defense and infrastructure, are reshaping sectoral dynamics. Deutsche Bank's own cost-cutting measures-such as a revised cost-to-income ratio target of 65% by 2025-reflect a broader industry trend toward efficiency (as noted in the CTOL report). Investors are tilting toward sectors poised to benefit from this fiscal boost, including industrials, utilities, and defense. For example, the MDAX Index, which tracks mid-cap German stocks, has outperformed the DAX as companies like Siemens and ThyssenKrupp gain traction in infrastructure and energy transition projects, according to a Julius Baer note.

Institutional Moves and Portfolio Adjustments

Institutional investors are accelerating these shifts. Morningstar analysis notes that 20 new defense-focused ETFs and open-end funds launched in Europe since early 2024, capitalizing on Germany's increased defense spending. Similarly, BNP Paribas Wealth Management has advised clients to overweight European industrials and underweight U.S. tech stocks, citing "attractive entry points" in sectors like aerospace and renewable energy.

However, the reallocation is not without risks. The European Central Bank's (ECB) anticipated rate cuts, while supportive for equities, could compress net interest margins for banks like Deutsche Bank (as discussed in the CTOL report). Additionally, U.S. tariff threats and geopolitical tensions remain overhangs, particularly for export-dependent sectors like automotive and machinery (per the DB Research outlook).

Conclusion: Navigating the New Normal

Deutsche Bank's downgrade serves as a cautionary tale for investors navigating a fragmented European market. While the bank's strategic pivot-through cost cuts, share buybacks, and a focus on capital returns-offers a path to recovery, its success hinges on broader macroeconomic stability. For now, the reallocation to European equities appears justified by valuation gaps and fiscal tailwinds, but investors must remain vigilant against sector-specific risks and global trade uncertainties.

As Germany's fiscal stimulus begins to materialize in 2026, the focus will shift to execution. Until then, the European equity market's resilience-driven by strategic reallocation and sectoral rebalancing-offers a compelling counterpoint to the U.S. growth narrative.

Comentarios

Aún no hay comentarios