The Implications of a Declining 5-Year JGB Yield for Global Bond Markets

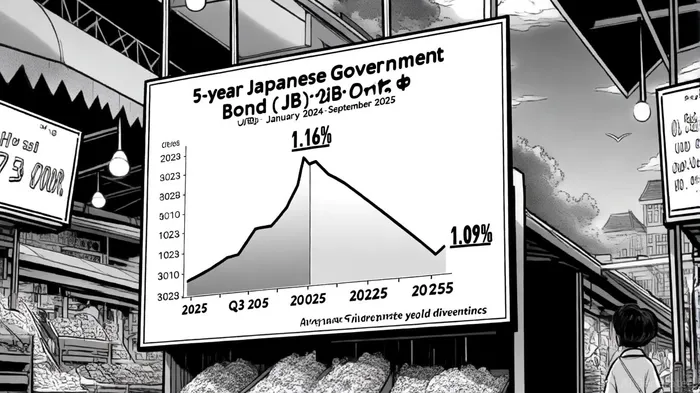

The Japanese Government Bond (JGB) market has long served as a barometer for global bond dynamics, and the recent trajectory of the 5-year JGB yield underscores its growing influence on international investment strategies. As of September 2025, the 5-year JGB yield stood at 1.230%, a sharp increase from 0.48% in the same period in 2024[3]. However, market forecasts suggest a potential reversal, with analysts projecting a decline to 1.09% by the end of the third quarter and 1.01% within 12 months[1]. This projected decline, if realized, would mark a pivotal shift in a market that has been central to global capital flows and risk-return trade-offs.

The Rise and Its Drivers

The upward trend in JGB yields through 2025 reflects a confluence of factors. Reduced central bank intervention, particularly by the Bank of Japan (BoJ), has amplified market forces, while fiscal pressures from Japan's substantial debt load—now exceeding 260% of GDP—have heightened borrowing costs[2]. Additionally, technical imbalances, such as weak demand at a five-year note auction (bid-to-cover ratio of 2.5x, the lowest in 13 years[6]), have exacerbated volatility. These dynamics have pushed the 5-year yield to 1.16% as of August 21, 2025[3], a level not seen in over a decade.

Projected Decline: A New Equilibrium?

Despite the recent surge, forward-looking indicators hint at a potential correction. By late September 2025, the yield briefly dipped to 1.215%[3], signaling tentative market skepticism about the sustainability of higher rates. Analysts attribute this to several factors:

1. Policy Interventions: The Japanese Ministry of Finance's proposal to cut super-long-dated JGB issuance in 2025 aims to stabilize liquidity and curb excessive volatility[1].

2. Global Rate Divergence: The widening gap between Japanese and U.S. yields (4.418% for the 10-year Treasury[3]) has created arbitrage opportunities, drawing capital to higher-yielding assets and easing pressure on shorter-dated JGBs.

3. Investor Behavior: Foreign investors, recognizing the "twist" in Japan's yield curve, have begun reallocating capital to exploit relative value opportunities[5].

Strategic Asset Allocation in a Low-Yield Environment

A declining 5-year JGB yield would have profound implications for global bond strategies. Historically, JGBs have been a cornerstone of low-risk, low-return portfolios, but their recent volatility has forced investors to reassess.

- Duration Rebalancing: Shorter-duration bonds, which are less sensitive to interest rate fluctuations, are likely to gain favor. For instance, investors may shift from 5-year JGBs to 2-year notes or even U.S. Treasuries, where yields remain significantly higher[3].

- Diversification into Alternatives: As JGB yields decline, the opportunity cost of holding cash or equities may rise. This could spur increased allocations to alternative assets like infrastructure bonds or private debt, which offer higher yields in a low-interest-rate world[4].

- Geographic Rotation: A weaker yen and divergent monetary policies may drive capital toward emerging markets or European sovereign bonds, where yields are more attractive relative to Japan's shrinking returns[2].

Risk-Return Trade-Offs and Market Volatility

The projected decline in JGB yields also reshapes risk-return dynamics. Higher yields typically correlate with increased market stability, as they attract capital and reduce the appeal of riskier assets. Conversely, a drop in yields could reignite concerns about liquidity and fiscal sustainability in Japan, potentially spilling over into global markets[2].

For example, a 1.09% yield by late 2025 would represent a 140-basis-point decline from its August peak[1]. This could trigger a reevaluation of Japan's fiscal health, particularly as its debt-to-GDP ratio remains among the highest globally. Such uncertainty might prompt investors to prioritize liquidity and credit quality, favoring U.S. Treasuries or German Bunds over JGBs[3].

Conclusion: Navigating the New Normal

The interplay between JGB yields and global bond markets highlights the fragility of a low-yield environment. While the projected decline in 5-year JGB yields offers a glimpse of normalization, it also underscores the need for adaptive asset allocation strategies. Investors must balance the allure of higher-yielding assets with the risks of market dislocation, particularly in a world where central bank policies and fiscal pressures remain intertwined.

As the BoJ and Japanese Ministry of Finance recalibrate their approaches, global investors will need to remain agile, leveraging tools like dynamic duration adjustments and geographic diversification to navigate the evolving landscape. The coming months will test whether the JGB market can stabilize—or if its turbulence will ripple across the broader fixed-income universe.

Comentarios

Aún no hay comentarios