Identifying Undervalued Growth Stocks in Digital Transformation: A 2025 Momentum and Fundamentals Analysis

In the volatile markets of 2025, investors seeking growth must balance momentum with fundamentals. The digital transformation sector-driven by AI, cloud computing, and automation-offers fertile ground for such opportunities. By analyzing key players like AccentureACN--, IBMIBM--, MicrosoftMSFT--, OracleORCL--, and SAPSAP--, we can identify undervalued stocks where strong financials align with transformative innovation.

Accenture: GenAI Growth Amid Booking Weakness

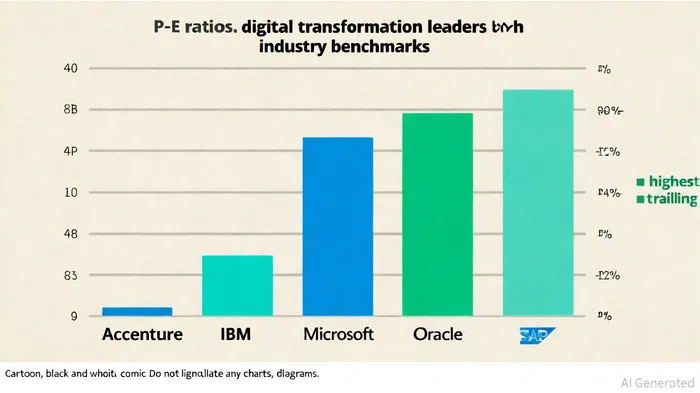

Accenture's Q3 2025 results revealed mixed signals: revenue grew 7% year-over-year to $17.7 billion, but new bookings fell 6% to $19.7 billion, according to a Forbes report. However, the Forbes piece also noted that its GenAI business surged, generating $700 million in the quarter and $4.1 billion in year-to-date bookings. This specialization in AI-driven solutions positions Accenture as a critical player in enterprise digitalization. Despite a P/E ratio of 28.98, per the Microsoft Q2 report, its operating margin expansion to 16.8% and $3.52 billion in free cash flow suggest disciplined execution. The challenge lies in sustaining booking momentum, but its AI focus could justify a premium valuation.

IBM: Rebuilding a Legacy with AI and Cloud

IBM's Q2 2025 revenue rose 8% to $17.0 billion, driven by Software and Infrastructure segments, as shown in IBM's Q2 results. Its cloud infrastructure revenue grew 52% year-over-year, and operating margins hit 18.8% (Non-GAAP). While IBM's P/E ratio of 44.87, per IBM financial ratios, appears high, its debt-to-equity ratio of 2.46 (noted in the same financial ratios) reflects manageable leverage. The company's reinvestment in AI (e.g., Watson, hybrid cloud) and quantum computing signals long-term potential. For investors, IBM's ability to convert R&D into recurring revenue streams will determine its undervaluation thesis.

Microsoft: Cloud and AI Dominance at a Discount

Microsoft's Q2 2025 revenue reached $69.6 billion, with cloud revenue growing 21% to $40.9 billion, as described in a Microsoft Q2 deep dive. That analysis also highlights the AI business surpassing a $13 billion annual run rate, up 175% year-over-year. A P/E ratio of 28.98 and a debt-to-equity ratio of 0.21 make Microsoft a standout in the sector. Despite a 29% drop in free cash flow due to capital expenditures, its low leverage and 31% Azure growth (excluding AI) underscore resilience. Microsoft's disciplined approach to balancing innovation with profitability makes it a compelling undervalued play.

Oracle: Cloud Leap, High P/E, and Leverage Risks

Oracle's Q2 2025 revenue grew 9% to $14.1 billion, with cloud infrastructure revenue surging 52% to $2.4 billion, according to the Oracle Q2 report. Its operating margin of 43% (Non-GAAP) and $4.2 billion in net income highlight profitability. However, a P/E ratio of 40.92 and a debt-to-equity ratio of 4.53 raise concerns about valuation and leverage. Oracle's aggressive cloud push, including AI integration, could justify these metrics if execution remains strong. Investors must weigh its growth potential against financial risks.

SAP: High P/E but Strong Cloud Momentum

SAP's Q2 2025 revenue rose 9% to €9.03 billion, with cloud revenue up 24% to €5.13 billion, as reported in the SAP Q2 statement. Its non-IFRS operating profit of €2.57 billion and 32% year-over-year growth in cloud ERP revenue reflect disciplined cost control. However, a trailing P/E of 58.65 and forward P/E of 46.74 suggest it trades at a premium to peers. SAP's debt-to-equity ratio of 0.65 is moderate, but its valuation hinges on sustaining AI-driven cloud growth.

Industry Benchmarks and Strategic Takeaways

The digital transformation sector's average debt-to-equity ratio is 0.64, based on industry debt-to-equity data, with SAP and IBM slightly above but still manageable. Microsoft's 0.21 D/E and Oracle's 4.53 highlight divergent capital structures. For P/E ratios, Microsoft's 28.98 and Accenture's 28.98 appear undervalued relative to the sector's 35.00 benchmark. IBM and Oracle trade at premiums, while SAP's high P/E reflects investor optimism about its cloud transition.

Key Takeaway: Microsoft and Accenture stand out as undervalued growth stocks. Microsoft's low P/E, robust cloud margins, and AI momentum offer a margin of safety. Accenture's GenAI focus, despite booking challenges, aligns with long-term digital trends. IBM and Oracle require closer scrutiny of leverage and execution risks, while SAP's premium valuation demands confidence in its cloud ERP growth.

In a market where volatility tests patience, digital transformation leaders with strong fundamentals and clear innovation pathways-like Microsoft and Accenture-provide a compelling case for long-term growth.

Comentarios

Aún no hay comentarios