Hyundai's Strategic Pivot: Navigating Tariffs and Policy Shifts in the U.S. Auto Industry

The U.S. auto industry is undergoing a fundamental restructuring, driven by a single, powerful policy catalyst. In March 2025, President Trump invoked Section 232 of the Trade Expansion Act to impose a 25% tariff on all imported vehicles and auto parts. This move was not merely a trade policy; it was a strategic directive that has reshaped corporate investment plans across the sector. The administration's clear principle-that "if you build in the United States, there is no tariff"-has become the central tenet of a massive reshoring wave.

The scale of the response has been immediate and substantial. Automakers and suppliers have announced billions in new domestic investment to localize production and mitigate the tariff burden. StellantisSTLA-- pledged $13 billion, FordF-- committed $2 billion, and General MotorsGM-- plans to move production from Mexico to three U.S. plants. This capital is flowing into a new reality where a domestic manufacturing footprint is no longer just an operational choice but a critical strategic advantage for long-term competitiveness.

Hyundai's $26 billion U.S. investment plan through 2028 stands as a prime example of this adaptation. The company's strategy explicitly aims to localize supply chains by building a new steel mill and expanding auto production. This pivot is a direct, multi-year response to the policy environment, embedding the "no tariff" principle into its long-term capital allocation. The move is a calculated bet that the structural advantages of U.S. manufacturing-reduced exposure to import duties, enhanced supply chain resilience, and alignment with national policy-will outweigh the costs of this massive domestic build-out.

The broader industry shift is now in motion. While the tariffs have introduced short-term costs and supply chain friction, they have also created a powerful incentive for reshoring. The initial shock has catalyzed a retreat from some electric vehicle ambitions and a focus on more profitable, domestic production. The thesis is clear: in this new policy landscape, a company's ability to manufacture its products within the United States is becoming a primary determinant of its financial health and strategic flexibility. The record sales Hyundai is targeting are a symptom of this larger structural realignment, where operational and policy advantages converge to define the next generation of automotive leaders.

The Product Mix Realignment: From EVs to Hybrids

The shift in consumer demand is a stark lesson in policy-driven market volatility. The elimination of federal EV tax credits has caused a significant slowdown, with Tesla's sales declining 16% in the final quarter of 2025. This policy reversal created a vacuum that Hyundai was strategically positioned to fill. The company's sales data for December 2025 tells the clear story of a pivot: while its electric vehicles, the Ioniq 5 and Ioniq 6, saw sales plummet 50% and 62% respectively, its hybrid sales surged 71% in the same month. This diversification into hybrids and core SUVs provided a crucial buffer against the policy shock and consumer demand shifts.

Hyundai's record-setting sales for the third consecutive year were not built on electric momentum, but on electrified and traditional powertrains. The company's core SUVs-Palisade, Santa Fe, and Tucson-drove strong growth, with the Santa Fe up 20% for the year. More broadly, sales of electrified models jumped 25% in the third quarter, led by hybrid demand. This flexible powertrain strategy allowed Hyundai to navigate the challenging environment and post record sales, demonstrating the resilience of a diversified product portfolio.

The bottom line is a masterclass in operational agility. While Tesla's heavy reliance on federal policy support left it vulnerable, Hyundai's broader mix of hybrids, SUVs, and traditional vehicles provided a stable foundation. This realignment wasn't a retreat from electrification, but a smart adaptation to a changed market. By meeting customers where they are-offering compelling hybrid options and popular SUVs-Hyundai maintained its sales momentum and profitability. The company's commitment to its 2025 guidance, despite a 29% year-over-year drop in operating profit, underscores its disciplined execution through the transition. In a volatile market, this product mix realignment is a key part of its competitive moat.

The 2026 Outlook: Sustaining the Realignment

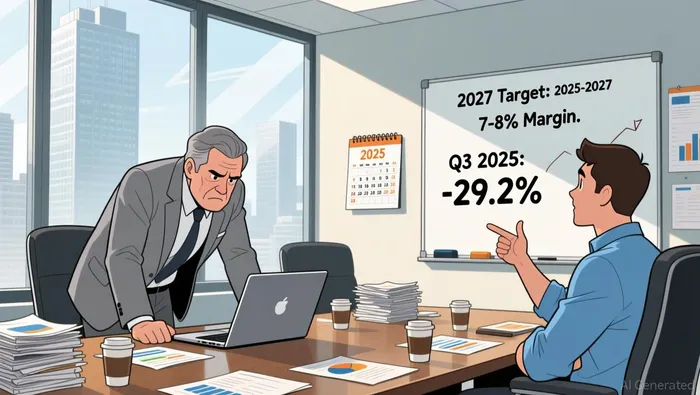

Hyundai's strategic pivot is now entering its execution phase, with 2026 serving as the critical year to translate ambitious plans into tangible profitability. The company's recent financials show the pressure of the transition: Q3 operating profit fell 29.2% year-over-year to 2.54 trillion won, with an operating margin of just 5.4%. This decline is directly tied to the headwinds of U.S. tariffs and higher incentives, a reality the company is actively managing through localisation and production optimization. The 2026 strategic plan, therefore, is not a new vision but a focused roadmap to navigate these challenges and build a more durable foundation.

The core of this roadmap is a two-pronged approach to insulate the business and build a new moat. First, Hyundai is doubling down on geographic and supply chain resilience. Its commitment to assembling 80% of its vehicles sold in the U.S. domestically by 2030 is a long-term, capital-intensive pledge to insulate itself from tariff and logistics risks. This is a defensive realignment, but one that also positions the company to capture more value within the North American market. Second, the company is aggressively pursuing an offensive transformation through technology. Executive Chair Euisun Chung has declared that AI integration will be central to the group's future, with the goal of embedding it into the organisation's "DNA." This isn't just about infotainment; it's about leveraging data from vehicles and manufacturing to drive innovation and efficiency. The parallel development of software-defined vehicles (SDVs) and robotics partnerships signals a bet on becoming a mobility technology leader, not just a carmaker.

The ultimate test of this strategy is margin recovery. The company has set a clear, forward-looking target: achieving a sustainable operating profit margin of between 7% and 8% by 2027. This implies a significant improvement from the current sub-6% level and indicates a strategic shift from pure volume growth to disciplined profitability. The path to this target will be measured by the pace at which localisation reduces costs, SDV initiatives drive premium pricing, and AI optimises operations. The recent 25% dividend increase shows management's confidence in the long-term trajectory, but the 2026 results will reveal whether the company can sustain its revenue momentum while simultaneously engineering this margin expansion.

The sustainability of Hyundai's realignment hinges on execution. The strategic priorities for 2026-customer focus, agile decision-making, and ecosystem competitiveness-are broad, but the company's actions must be specific. The key will be whether the investments in AI and local manufacturing begin to offset the ongoing tariff and incentive pressures. If successful, this could build a wider moat based on technological integration and supply chain control. If execution falters, the company risks getting caught between the high costs of transformation and the cyclical pressures of the global auto market. For now, 2026 is the year the company must prove its strategic pivot is more than a plan; it must become the engine of its future profitability.

Broader Industry Implications and Risks

The U.S. auto industry is in a state of profound realignment, driven by a protectionist policy shift that has created a stark competitive imbalance. The new equilibrium is one where German luxury brands face a 15% baseline tariff on every exported vehicle, a cost that is forcing them to absorb billions in additional expenses or pass them on to consumers. This has narrowed the pricing gap with domestic alternatives, shifting the calculus for buyers choosing between a BMW and a Cadillac. The result is a volatile environment where German automakers are raising prices across their 2026 lineups, while domestic competitors like Hyundai, which are largely exempt from these levies, can maintain more stable pricing. For dealers, this means watching closely for allocation changes and potential pullbacks in U.S. market investment as European brands prioritize viability over growth.

Hyundai's record sales in 2025, driven by a surge in hybrids and SUVs, is a direct beneficiary of this policy-driven shift. The company's ability to post its third straight year of record total sales while EV demand faded late in the year highlights a powerful consumer pivot. Buyers are spending their money on more traditional vehicles with electrified powertrains, a trend that Hyundai has successfully captured. This success is now being institutionalized through a major capital commitment, with the company increasing its U.S. investment to $26 billion through 2028. This reshoring trend, supported by policy incentives, is a long-term strategic bet on building domestic capacity and supply chains.

Yet, the sustainability of this new order faces two key risks. First, the current hybrid demand surge may prove to be a policy-driven buffer rather than a durable consumer preference. As the initial shock of tariffs settles, the market must determine whether this shift in spending is permanent or a temporary adjustment. Second, the long-term success of the reshoring trend depends entirely on the stability of the policy environment. The industry has already weathered chaotic tariff announcements and reversals, which have prompted automakers to scale back profit expectations and scramble to renegotiate costs. The significant capital investment required for new domestic capacity, like Hyundai's planned steel mill and robotics hub, is a multi-year bet on a political landscape that remains unpredictable. The industry's new equilibrium is fragile, built on a foundation of tariffs and reshoring promises that could be altered by the next administration.

Comentarios

Aún no hay comentarios