Housing Stocks and Interest Rate Cuts: Sector-Specific Exposure and Earnings Momentum

The Federal Reserve's monetary policy has long been a critical determinant of housing sector performance. As the central bank navigates rate-cutting cycles, investors must dissect sector-specific dynamics to gauge the potential for earnings momentum and macroeconomic alignment. Historical data reveals a nuanced relationship between interest rate cuts and housing stocks, with sub-industries like homebuilders and real estate services exhibiting divergent responses to monetary easing.

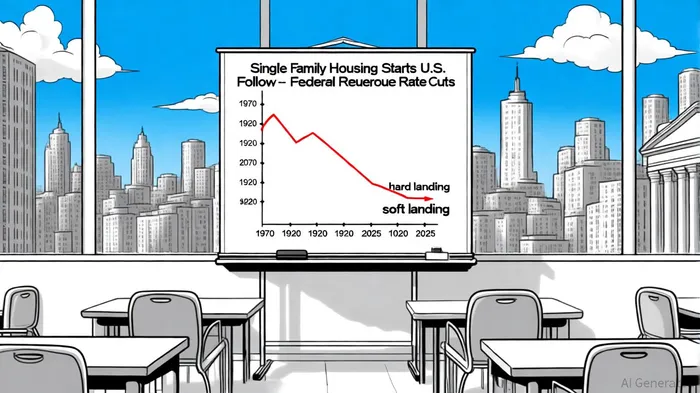

Historical Trends: Housing Starts and Rate Cuts

According to a jbrec analysis, single-family housing starts have historically increased by an average of 12% within 12 months of the first Federal Reserve rate cut, excluding the 2007 global financial crisis. This growth persisted even during "hard landing" scenarios, where recessions coincided with falling rates; in 1984 and 1995 "soft landing" cycles, housing starts either declined modestly or grew slightly, underscoring the sector's sensitivity to both monetary policy and broader economic conditions, the jbrec analysis notes.

A Northern Trust analysis finds the S&P 500 Index has averaged 14.1% returns in the 12 months following the first rate cut since 1980, though volatility often peaks around the timing of cuts. Northern Trust also highlights that quality and low-volatility stocks have historically outperformed during these cycles, suggesting that housing sector players with strong balance sheets and pricing power may benefit disproportionately from rate cuts.

Sector-Specific Dynamics: Homebuilders and Real Estate Services

Lower federal funds rates directly reduce short-term borrowing costs for homebuilders, particularly those reliant on Acquisition, Development, and Construction (AD&C) loans, as the NAHB blog explains. This easing can alleviate supply constraints and improve margins. However, long-term mortgage rates-more influenced by the 10-year Treasury yield and inflation expectations-often lag behind Fed actions, creating a disconnect between immediate policy benefits and consumer affordability, the NAHB blog adds.

A Chicago Fed letter observes that a significant portion of fixed-rate mortgages remain well below market rates, locking in homeowners and suppressing existing home sales. This "lock-in effect" has redirected demand toward new construction, even as overall housing demand wanes. For example, the National Association of Home Builders (NAHB) notes that reduced turnover among existing homeowners has amplified pressure on new homebuilders to fill supply gaps.

Company-Level Analysis: Earnings and Margin Pressures

Recent earnings reports from major homebuilders highlight the sector's mixed response to rate cuts. Lennar CorporationLEN-- (LEN), in its Q2 2025 results, reported Q2 2025 net earnings of $477 million, down from $954 million in Q2 2024, amid soft demand and affordability challenges. Gross margins on home sales fell to 17.8% from 22.6% the prior year, reflecting higher marketing expenses and reduced leverage, according to Lennar's Q2 2025 results.

KB Home (KBH), however, demonstrated resilience. Despite a 3.1% year-over-year revenue decline in Q2 2024, its net income rose 2.4% to $168.42 million, with EPS growing 10.8% to $2.15. A Kavout analysis attributes this to strategic cost efficiencies and a forward non-GAAP P/E ratio of 10.31x, well below the industry average. However, historical backtesting of KB Home's earnings beats from 2022 to 2025 reveals limited statistical significance, with average returns underperforming the stock's baseline and mixed short-term outcomes[^backtest]. Specifically, only two qualifying "beat" events occurred in the window, and while the 1- to 3-day win rate reached 50%, mid-term drawdowns (>-6%) and muted upside suggest a simple "buy on beat" strategy has not recently been rewarded for KBHKBH--.

D.R. Horton (DHI) faced headwinds, projecting 2025 revenue between $36 billion and $37.5 billion-below the estimated $39.41 billion-due to weak demand and aggressive buyer incentives, according to a Yahoo Finance report. The company revised its home delivery forecast downward to 90,000–92,000 units, signaling margin compression in the near term, the Yahoo Finance report states.

Macroeconomic Linkages and Cap Rate Implications

The Fed's rate cuts also influence real estate capitalization rates. A CBRE brief estimates that for every 100-basis-point change in the 10-year Treasury yield, cap rates for multifamily assets shift by roughly 75 bps, while office assets move by about 70 bps. CBRECBRE-- forecasts cap rates for industrial and multifamily sectors to stabilize at 4.5% by 2025, reflecting downward pressure from rate cuts.

However, structural challenges persist. High supply costs, labor shortages, and tariffs have constrained housing supply growth, even as borrowing costs decline, an Investopedia article argues. For example, new housing starts fell 8.4% in 2024 compared to 2023, despite Fed easing, the Investopedia article notes.

Strategic Implications for Investors

While rate cuts offer near-term relief to homebuilders through lower AD&C financing costs, their impact on mortgage rates remains uncertain. Projections from Gallagher Mohan suggest mortgage rates could dip below 6% by 2025, but affordability hurdles-such as elevated home prices relative to incomes-will linger. Investors should prioritize companies with strong balance sheets and geographic diversification, as these firms are better positioned to weather cyclical volatility.

Conclusion

The housing sector's response to Fed rate cuts is shaped by a complex interplay of macroeconomic factors, sub-industry dynamics, and company-specific fundamentals. While historical data suggests that single-family housing starts and homebuilder earnings can benefit from rate cuts, structural challenges like labor shortages and affordability constraints temper the upside. Investors must remain vigilant, balancing optimism about monetary easing with caution regarding persistent supply-side bottlenecks.

Comentarios

Aún no hay comentarios