First Horizon's Q3 2025 Earnings: A Glimpse into Profitability and Operational Efficiency Amid Market Volatility

First Horizon National Corporation's Q3 2025 earnings report delivered a compelling narrative of operational resilience and strategic execution, yet the stock's pre-market decline of 12.25% to $24.04, according to an earnings call transcript, raises critical questions about market sentiment and long-term investor confidence. This analysis evaluates the bank's path to profitability and operational efficiency, contextualizing its performance against Wall Street estimates and broader macroeconomic dynamics.

Profitability Outperforms Expectations, But Margins Remain a Focus

First Horizon's adjusted earnings per share (EPS) of $0.51 in Q3 2025 exceeded the consensus estimate of $0.44 by 15.91%, according to a Panabee report, while revenue surged to $889 million, surpassing projections from Market Research Forecast. The primary drivers of this outperformance were a $33 million increase in net interest income and a 15-basis-point expansion in the net interest margin to 3.55%, as noted in a Benzinga analysis. Additionally, fee income rose by $26 million quarter-over-quarter, according to StockAnalysis, reflecting the bank's ability to diversify revenue streams.

However, profitability metrics must be viewed through the lens of First Horizon's 2026 goals. The company aims for a 15%+ adjusted return on tangible common equity (ROTCE) and mid-single-digit loan growth, according to a backtest of FHN's earnings-beat performance (2022–2025). While Q3 results suggest progress, the path to these targets hinges on sustaining margin expansion amid a competitive lending environment and potential Federal Reserve rate cuts.

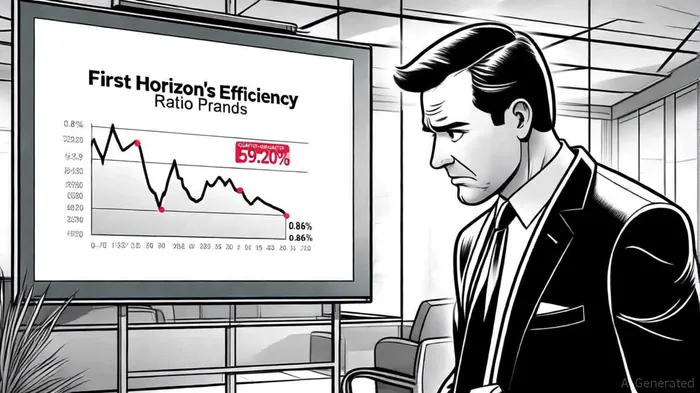

Operational Efficiency Gains Highlight Strategic Discipline

A critical component of First Horizon's Q3 success was its improved efficiency ratio, which declined by 0.86% quarter-over-quarter to 59.20%. This improvement underscores the bank's commitment to cost management, driven by digital transformation initiatives, workforce optimization, and process streamlining. For context, the industry average efficiency ratio for regional banks typically ranges between 60% and 65%, making First Horizon's performance particularly noteworthy.

The bank's strategic investments in technology and client relationships have not only reduced redundancies but also enhanced customer retention and cross-selling opportunities. These initiatives align with its 2025 plan to achieve a 10.75% CET1 capital ratio while exploring small M&A opportunities.

Stock Price Volatility: A Disconnect Between Fundamentals and Market Sentiment

Despite the earnings beat and operational improvements, First Horizon's stock plummeted 12.25% pre-market. Analysts attribute this to broader macroeconomic concerns, including uncertainty around the Federal Reserve's rate-cut timeline and a challenging economic outlook. While the company's six-month price return of 33% demonstrates resilience, the sharp decline highlights investor skepticism about the sustainability of its performance.

Historically, when First HorizonFHN-- has beaten earnings expectations, the stock has shown a tendency to recover and outperform the benchmark over a 30-day period, with an average cumulative return of +6.5% compared to +1.9% for the benchmark (see Backtest of FHNFHN-- earnings beat performance (2022–2025)). While the initial short-term edge is weak, the win rate improves significantly by day 30, reaching 78% (Backtest of FHN earnings beat performance (2022–2025)). This pattern suggests that market reactions to earnings surprises may be more nuanced than immediate price swings indicate, with patient investors potentially capturing value over time.

This volatility contrasts with analyst optimism. Eleven analysts covering the stock have an average price target of $25.73, with a high estimate of $29.00, and RBC Capital and Barclays have raised their targets to $27 and $29, respectively. The "Buy" consensus suggests confidence in First Horizon's long-term strategy, even as short-term market dynamics create noise.

Looking Ahead: Balancing Growth and Risk

First Horizon's Q3 results position it as a strong contender in the regional banking sector, but its path to profitability requires navigating several risks. These include:

1. Margin Compression: A potential slowdown in net interest margin expansion if rate cuts materialize sooner than anticipated.

2. Competitive Pressures: Intensifying competition in loan origination and fee-based services.

3. Capital Deployment: Balancing M&A opportunities with maintaining a robust CET1 capital ratio.

Nonetheless, the bank's focus on operational efficiency and strategic reinvestment provides a buffer against these challenges. As noted in its earnings call, First Horizon's emphasis on "highest origination funding in two years" signals a proactive approach to growth.

Conclusion

First Horizon's Q3 2025 earnings underscore its ability to deliver profitability and efficiency gains in a challenging environment. While the stock's post-earnings decline reflects macroeconomic anxieties, the company's fundamentals and analyst optimism suggest a resilient trajectory. Investors should monitor its progress toward 2026 ROTCE targets and its ability to execute M&A strategies without compromising capital strength. For now, the bank's blend of disciplined cost management and strategic innovation positions it as a compelling case study in regional banking resilience.

Comentarios

Aún no hay comentarios