Hock Lian Seng Holdings: Capital Allocation Challenges and the Road to ROCE Recovery

Hock Lian Seng Holdings (SGX:J2T) has long been a fixture in Singapore’s construction and infrastructure landscape, but its recent financial performance raises critical questions about its capital allocation strategy and long-term growth potential. With a ROCE (Return on Capital Employed) of 3.5% as of June 2025—well below the industry average of 7.5%—the company faces mounting pressure to justify its reinvestment initiatives and reverse declining returns [1]. This analysis evaluates whether Hock Lian Seng’s current strategy can address these challenges or if structural inefficiencies threaten its ability to deliver value to shareholders.

A Decline in ROCE: Structural or Cyclical?

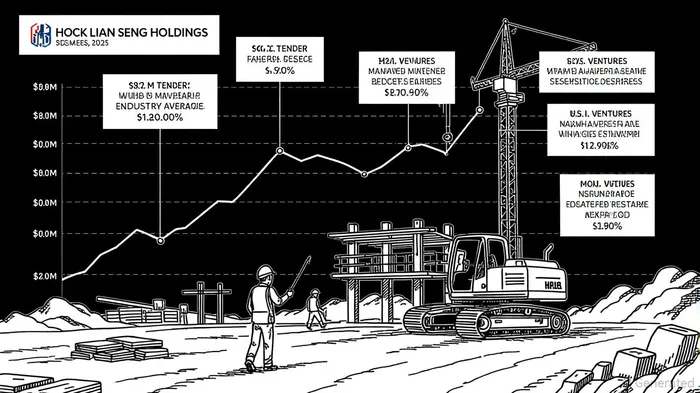

Hock Lian Seng’s ROCE has steadily declined from 4.7% in 2020 to 3.5% in 2025, a trend that outpaces the broader industry’s performance [1]. While the company has maintained earnings growth (21.4% CAGR over five years), its net profit margin of 10.8% lags historical benchmarks, suggesting capital is not being deployed as efficiently as possible [4]. The EPS drop in 1H 2025 (S$0.017 vs. S$0.04 in 1H 2024) further underscores operational headwinds, particularly in capital-intensive projects [1].

The root cause of this decline appears multifaceted. First, the construction sector in Singapore is grappling with tight foreign-worker quotas, rising labor costs, and the logistical complexities of vertical builds in a land-constrained environment [3]. These industry-specific challenges have compressed margins and delayed project timelines, limiting the ability to scale returns. Second, Hock Lian Seng’s capital allocation decisions—while ambitious—have yet to translate into meaningful ROCE improvements. For instance, the company’s $4B investment in U.S.-based ventures, aimed at diversifying its economic footprint, lacks transparency in terms of ROI expectations and timelines [1]. Similarly, the recent $88.2M tender for an industrial site, while aligned with national infrastructure goals, has not yet driven significant sales growth [1].

Reinvestment Initiatives: Promise vs. Execution

Hock Lian Seng’s management has emphasized reinvestment as a core growth strategy, but the results remain underwhelming. The company’s capital employed has increased, yet this has not translated into higher sales or ROCE, indicating that reinvestment projects may be long-term in nature [1]. For example, the $88.2M tender aligns with Singapore’s National Day Rally 2025 agenda, which prioritizes urban rejuvenation in areas like Woodlands and Sembawang [2]. While such projects are expected to drive demand for engineering services, their impact on ROCE will depend on execution efficiency and cost management.

The U.S. reinvestment strategy, meanwhile, reflects a broader trend of firms recalibrating global portfolios amid shifting economic dynamics. However, the lack of specificity around ROI expectations and alignment with ROCE goals raises concerns. As noted in global buyback discussions, companies often face scrutiny over management’s ability to act as effective capital allocators [2]. Hock Lian Seng’s absence of buyback initiatives in the recent quarter further highlights a reliance on organic growth, which may not be sufficient to offset declining returns [1].

Management’s Track Record: A Mixed Bag

Hock Lian Seng’s historical capital allocation decisions reveal a mixed record. While the company has demonstrated resilience in securing large-scale tenders and expanding its capital base, its ability to convert these investments into sustainable returns remains unproven. The EPS decline in 1H 2025, coupled with a ROCE that lags the industry average, suggests that management’s strategic priorities may not be fully aligned with shareholder value creation [1].

This is not to dismiss the company’s potential. The construction sector in Singapore is poised for growth, driven by urbanization and infrastructure modernization. Hock Lian Seng’s involvement in projects like the Woodlands industrial site tender positions it to benefit from these trends. However, the absence of clear metrics to evaluate the success of its U.S. ventures and the lack of transparency in capital allocation rationale create uncertainty.

Valuation and Long-Term Outlook

Hock Lian Seng’s current valuation appears to reflect a balance of optimism and caution. While the company’s reinvestment initiatives and alignment with national infrastructure goals are positives, the weak ROCE and declining EPS suggest that investors are pricing in execution risks. For the stock to justify its valuation, management must demonstrate that its capital allocation strategy can reverse the ROCE decline and deliver consistent returns.

Key watchpoints include:

1. ROI from U.S. investments: If these ventures generate meaningful cash flows within the next 12–18 months, they could offset domestic challenges.

2. Execution on the $88.2M tender: Timely project delivery and cost control will be critical to improving margins.

3. Management transparency: Clear communication on capital allocation rationale and performance metrics will be essential to rebuilding investor confidence.

Conclusion

Hock Lian Seng Holdings’ capital allocation challenges highlight the delicate balance between long-term reinvestment and short-term profitability. While the company’s involvement in high-potential infrastructure projects and U.S. diversification efforts offer growth avenues, the current ROCE trajectory and operational inefficiencies pose significant risks. Investors must weigh the potential for future returns against the company’s historical struggles in capital efficiency. For now, the stock appears to carry a speculative premium, justified only if management can prove its ability to execute on its strategic vision.

Source:

[1] Hock Lian Seng Holdings (SGX:J2T) Could Be Struggling To Allocate Capital Effectively, [https://simplywall.st/stocks/sg/capital-goods/sgx-j2t/hock-lian-seng-holdings-shares]

[2] NATIONAL DAY RALLY 2025: Five Singapore Stocks to Watch, [https://sgstocksinvesting.com/national-day-rally-2025-five-singapore-stocks-to-watch/]

[3] Singapore Construction Market Size, Share & 2030 Growth, [https://www.mordorintelligence.com/industry-reports/singapore-construction-market]

Comentarios

Aún no hay comentarios