The High-Yield Gamble: Evaluating MFA Financial's 15.49% Dividend in a Risk-Adjusted Framework

In the world of high-yield investments, few instruments capture the imagination like business development companies (BDCs). These entities, designed to provide capital to small and mid-sized businesses, often tout double-digit dividend yields that shimmer like beacons in a low-interest-rate environment. Yet, as with any financial alchemy, the question remains: Are these returns worth the risks? MFA FinancialMFA--, Inc. (MFA), a BDC with a 15.49% dividend yield as of October 14, 2025[2], offers a case study in the tension between reward and volatility.

The Allure and the Arithmetic

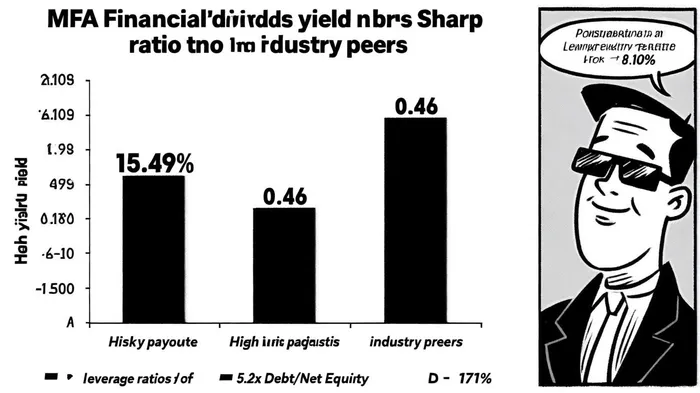

MFA's quarterly dividend of $0.36 per share, last paid on July 31, 2025[4], appears enticing at first glance. However, the math tells a more precarious story. According to a report by PortfoliosLab[3], the company's dividend payout ratio-defined as the percentage of earnings allocated to dividends-stands at 171% against GAAP earnings. This means MFAMFA-- is distributing more in dividends than it generates in profits, a red flag for long-term sustainability. Compounding this issue, operating cash flow has plummeted 76% year-over-year to $23.9 million[3], raising questions about the company's ability to maintain its payout without external support.

Portfolio Composition: A House of Cards?

MFA's investment strategy hinges on a portfolio of $10.8 billion in residential investment assets[1], including non-qualified mortgage (Non-QM) loans, single-family rental (SFR) loans, and transitional loans. These instruments, while potentially lucrative, carry inherent risks. Non-QM loans, for instance, lack the regulatory safeguards of traditional mortgages, exposing MFA to higher default rates. Meanwhile, the company's $1.7 billion in Agency MBS[1]-backed by Fannie Mae and Freddie Mac-offers relative safety but yields less than the riskier segments of its portfolio.

The leverage ratios further amplify the stakes. As of June 30, 2025, MFA's Debt/Net Equity Ratio stands at 5.2x[1], significantly higher than the industry average for BDCs. While leverage can amplify returns in favorable conditions, it magnifies losses during downturns. Recourse leverage of 1.8x[1] adds another layer of complexity, as it ties the company's obligations to specific assets rather than its entire balance sheet.

Risk-Adjusted Returns: A Negative Proposition

The Sharpe ratio, a critical metric for evaluating risk-adjusted returns, paints a grim picture. MFA's Sharpe ratio of -0.46 for the 1-year period ending October 2025[3] indicates that the company's returns have not compensated investors for the level of risk undertaken. This negative ratio underscores the volatility of MFA's strategy, particularly in a market where interest rates remain elevated and credit cycles are unpredictable.

Investor Considerations: High Yield or High Risk?

For income-hungry investors, MFA's 15.49% yield is undeniably attractive. Yet, the company's financial metrics suggest a precarious balance sheet. The combination of a payout ratio exceeding 100%, declining cash flow, and a negative Sharpe ratio signals a high-risk proposition. While MFA's management may argue that its expertise in mortgage instruments and aggressive leverage can drive returns, the current data does not support a confident endorsement of its risk-adjusted performance.

Investors must weigh these factors against their risk tolerance. For those seeking stable, predictable income, MFA's volatility and leverage may be untenable. For others willing to accept short-term fluctuations in pursuit of outsized yields, the company could represent a speculative opportunity-but one that demands constant vigilance.

Conclusion

MFA Financial's 15.49% dividend yield is a siren song in a market starved for income. However, the company's financial health-marked by a payout ratio exceeding earnings, declining cash flow, and negative risk-adjusted returns-casts doubt on the sustainability of its current trajectory. As with any high-yield investment, the key lies in aligning the opportunity with one's risk profile. For now, MFA remains a case study in the delicate dance between reward and ruin.

Comentarios

Aún no hay comentarios