High-Yield Fixed-Income Opportunities in a Rising Rate Environment: The Tactical Bond Strategy Edge

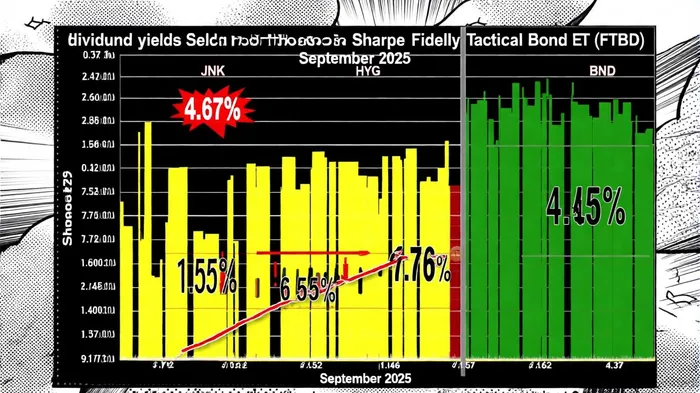

In 2025, as central banks continue to navigate inflationary pressures and rising interest rates, fixed-income investors face a paradox: higher yields offer enticing income potential, but prolonged rate hikes threaten bond prices. Tactical bond strategies, however, are emerging as a compelling solution to balance these competing forces. The Fidelity Tactical Bond ETF (FTBD), with its recent $0.1840 per-share April 1, 2025 distribution (April 1, 2025 distribution), underscores the growing appeal of active management in this environment. This payout, part of a trailing twelve-month (TTM) yield of 4.67% (trailing twelve-month yield), highlights how tactical strategies can generate income while adapting to shifting market conditions.

The Case for Tactical Strategies

Traditional bond ETFs like the Vanguard Total Bond Market ETF (BND) and iShares Core U.S. Aggregate Bond ETF (AGG) have delivered modest returns in 2025, with 10-year annualized returns of 1.76% and 1.85%, respectively (see Best bond ETFs for 2025). However, their fixed allocations to long-duration bonds leave them vulnerable to price declines in a rising rate environment. In contrast, tactical strategies like FTBD dynamically adjust exposure to sectors such as high-yield corporate debt, emerging market bonds, and short-term securities. For instance, FTBD's 7.29% year-to-date return as of September 2025 outpaces BND's 4.7% YTD gain, demonstrating the advantages of active duration management.

The key differentiator lies in risk-adjusted performance. While FTBD's Sharpe ratio of 0.72 over the past year is average, its flexibility allows it to mitigate volatility. For example, during periods of steepening yield curves—where long-term rates rise faster than short-term rates—FTBD can reduce exposure to longer-duration assets. This contrasts with high-yield ETFs like the SPDR Bloomberg High Yield Bond ETF (JNK), which, despite a 6.55% yield, carries a Sharpe ratio of 1.46 per the JNK historical returns report and faces greater price sensitivity due to its average effective duration.

Risk and Duration Considerations

Duration, a measure of interest rate sensitivity, is critical in rising rate environments. Traditional high-yield ETFs like JNKJNK-- and HYG (iShares iBoxx $ High Yield Corporate Bond ETF) typically have durations of 5–6 years, making them prone to price declines as rates climb. FTBD, though an actively managed fund, does not disclose a fixed duration, but its portfolio's intermediate-term focus and hedging of foreign currency exposures—per its Yahoo Finance profile—suggest a shorter, more adaptive duration profile. This aligns with expert recommendations to shorten duration in 2025, as highlighted by Morgan Stanley's Fixed Income Outlook 2025.

However, tactical strategies are not without risks. FTBD's exposure to emerging market debt and high-yield sectors increases credit risk compared to investment-grade-focused ETFs like BND (see the FTBD profile). Additionally, its active management introduces tracking error and higher operational complexity. Investors must weigh these factors against the potential for income generation and capital preservation.

Expert Insights and Market Outlook

Analysts emphasize the importance of active selection in 2025. As noted by Janus Henderson, high-yield bonds in Europe and the U.S. offer attractive yields (5.5% and 7.2%, respectively), but require careful credit analysis. FTBD's ability to shift allocations—such as increasing exposure to short-term, floating-rate securities—positions it to capitalize on these opportunities while managing rate risk. Meanwhile, ultra-short duration ETFs like JPMorgan Ultra-Short Income ETF (JPST), with a Sharpe ratio of 7.73, highlight the appeal of minimal duration in volatile markets.

The Federal Reserve's anticipated rate cuts later in 2025 could further tilt the playing field. While longer-duration bonds may rebound, tactical strategies like FTBD can pivot to take advantage of yield curve steepening or sector rotations. This agility, combined with its 0.55% expense ratio, makes FTBD a cost-effective option for investors seeking income without locking into static allocations.

Conclusion

The Fidelity Tactical Bond ETF's recent $0.1840 distribution and 4.67% yield exemplify the income potential of tactical bond strategies in a rising rate environment. While traditional high-yield ETFs like JNK offer higher yields, their duration risk and volatility may outweigh benefits for risk-averse investors. FTBD's active management, though less transparent, provides a balanced approach to navigating 2025's uncertainties. As central banks remain data-dependent and inflation trends remain mixed, tactical strategies will likely play a pivotal role in optimizing fixed-income portfolios.

Comentarios

Aún no hay comentarios