High P/E Stocks with Muted Volatility: Strategic Put Option Positioning in Overvalued Sectors

In the volatile investment landscape of 2025, identifying sectors with high price-to-earnings (P/E) ratios but muted volatility offers a unique opportunity for strategic put option positioning. These sectors, while seemingly overvalued, exhibit structural stability that could mitigate downside risks, making them attractive for hedging or speculative plays. This analysis explores the Information Technology and Real Estate sectors—both trading at elevated P/E ratios—as prime candidates for such strategies, supported by granular data on earnings, volatility, and macroeconomic dynamics.

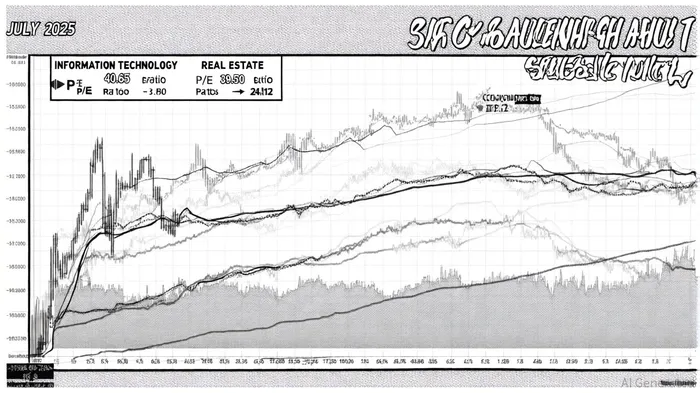

Information Technology: High Valuations Amid Structural Resilience

The Information Technology sector commands a trailing P/E ratio of 40.65 as of July 2025, reflecting robust investor confidence in its AI-driven growth trajectory [1]. Despite a 12.8% decline in Q1 2025 amid trade policy uncertainties, the sector demonstrated resilience in Q2 and late 2025, buoyed by surging demand for cloud infrastructure and semiconductor innovation [2]. This duality—high valuations paired with stabilizing fundamentals—creates a compelling case for put options.

While the sector's beta remains unquantified in recent data, its PEG ratio of 1.57 (relative to the XLK ETF) suggests it is undervalued compared to its earnings growth [3]. This metric implies that, despite a high P/E, the sector's earnings expansion could justify its valuation, reducing the likelihood of a sharp correction. However, risks such as trade tensions and supply chain disruptions persist [4]. For put option strategies, this means positioning for moderate corrections rather than catastrophic declines, leveraging the sector's structural growth while hedging against macroeconomic headwinds.

Real Estate: Overvaluation in a Fragmented Market

The Real Estate sector trades at a P/E ratio of 39.50, driven by speculative investment in tokenized assets and AI-powered valuation models [5]. Yet, its volatility is unevenly distributed: industrial and data center real estate have shown stability, while office and retail sectors grapple with high vacancy rates and delinquency risks [6]. This fragmentation complicates volatility assessments but highlights opportunities in subsectors with durable demand.

Historical volatility metrics for the sector remain opaque, but CBRE's H1 2025 Cap Rate Survey notes that industrial real estate prices rose 15–20% in power markets like Texas and Virginia, insulated from broader economic jitters [7]. For put options, this suggests targeting real estate ETFs or REITs with concentrated exposure to resilient subsectors, while avoiding overleveraged office properties. The sector's sensitivity to interest rates further underscores the need for timing—put options may gain value as rate cuts in late 2025 ease financing costs and stabilize valuations.

Strategic Put Option Positioning: Balancing Risk and Reward

Put options in high P/E sectors require careful calibration. For Information Technology, a long-dated put with a strike price 10–15% below the current level could hedge against trade policy-driven selloffs while benefiting from the sector's earnings momentum. In Real Estate, shorter-term puts on industrial-focused REITs might capitalize on rate-driven volatility without overexposure to cyclical downturns.

Key considerations include:

1. Implied Volatility (IV): The VIX's spike to 7.69 in early 2025 [8] inflated option premiums, making puts expensive. However, declining IV in late 2025 could present cheaper entry points.

2. Earnings Diversification: Sectors with recurring revenue models (e.g., SaaS in IT) or inelastic demand (e.g., staples) offer more predictable downside scenarios.

3. Macro Triggers: Tariff announcements and Fed policy shifts remain critical catalysts. For instance, the April 2025 tariff shock saw the VIX surge to 99th percentile levels [9], underscoring the need for real-time macro monitoring.

Conclusion

High P/E sectors like Information Technology and Real Estate present a paradox: overvalued yet structurally stable. By leveraging put options, investors can hedge against macroeconomic risks while participating in long-term growth. The key lies in granular sector analysis—distinguishing resilient subsectors from vulnerable ones—and aligning option strategies with evolving volatility dynamics. As 2025 progresses, these sectors will likely remain at the intersection of innovation and uncertainty, offering fertile ground for disciplined, data-driven positioning.

Comentarios

Aún no hay comentarios