Hess Midstream's Share Price Decline: Valuation Misalignment and Sector Resilience in Midstream Energy

The recent 3.3% drop in Hess MidstreamHESM-- (HESM) shares following UBS's downgrade from “buy” to “neutral” has sparked debate about the company's valuation and long-term prospects. While the downgrade reflects near-term concerns about reduced Bakken drilling activity and management transitions, a deeper analysis reveals a misalignment between Hess Midstream's current valuation and the structural resilience of the midstream sector.

Valuation Misalignment: A Contrarian Opportunity?

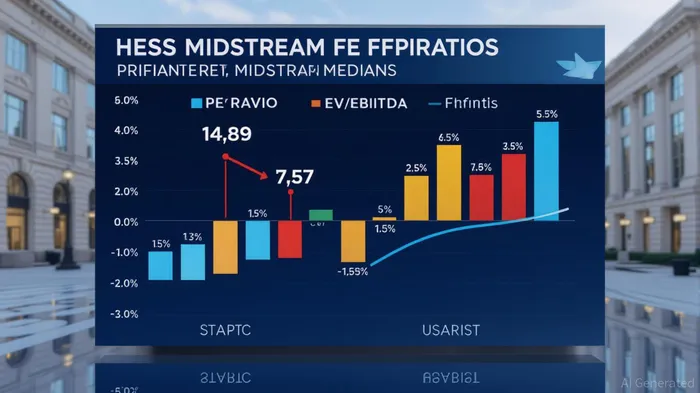

Hess Midstream's price-to-earnings (P/E) ratio of 14.89 as of 2025 exceeds that of peers like Monmouth Real Estate Investment Corporation (MNR) at 7.01 [3], while its enterprise value-to-EBITDA (EV/EBITDA) multiple of 7.57 is below the midstream sector median of 7-9x [2]. Even more striking is its forward EV/EBITDA of 5.97x, which suggests the market is discounting future cash flows at a significant margin of safety. This divergence may stem from UBS's concerns about Chevron's reduced Bakken rig count and broader commodity price pressures [1], but it overlooks Hess Midstream's strong Q2 2025 performance: $0.74 earnings per share and $414.2 million in revenue, both exceeding expectations [1].

Historical patterns reinforce the potential value of such outperformance. Over the past three years, Hess Midstream has beaten earnings expectations seven times, with a buy-and-hold strategyMSTR-- showing a rising win rate from 14% (day 1) to 57–83% by day 20–30. While abnormal returns are not statistically significant in the first two weeks, a longer holding window aligns with the company's structural strengths, suggesting patient capital may benefit from its operational discipline and sector tailwinds.

The undervaluation is further underscored by the sector's broader financial health. Midstream operators have deleveraged significantly since 2021, with debt/EBITDA ratios in the Solactive MLP & Energy Infrastructure Index falling to 4.35 from 5.6 [4]. Hess Midstream's disciplined capital allocation and focus on self-funding projects align with this trend, yet its valuation remains unloved by analysts.

Long-Term Resilience: Structural Tailwinds in Midstream Energy

The midstream sector's resilience is anchored in two pillars: inelastic demand for natural gas infrastructure and regulatory tailwinds. Natural gas consumption is projected to grow 25%–34% by 2030, driven by its role in power generation for data centers and AI computing [4]. Projects like Energy Transfer's Texas data center gas supply agreement and GE Vernova's expanded turbine production highlight this structural demand [4]. Hess Midstream, with its exposure to Bakken NGLs and potential LNG export infrastructure, is well-positioned to benefit.

Regulatory frameworks also bolster midstream stability. The Federal Energy Regulatory Commission (FERC) continues to approve critical projects, such as TC Energy's ANR Heartland pipeline, to address bottlenecks [4]. These approvals ensure predictable throughput for operators like Hess Midstream, which relies on long-term, fixed-fee contracts to insulate cash flows from commodity price swings.

Risks and Mitigants

UBS's downgrade underscores valid near-term risks: OPEC+ output increases have depressed commodity prices, and Chevron's four-rig operation in the Bakken could further strain Hess Midstream's earnings [1]. However, the sector's capital discipline—evidenced by a 22.3% decline in debt/EBITDA ratios since 2021 [4]—provides a buffer. Moreover, Hess Midstream's leadership transition, with Michael Bast succeeding John Gatling, may stabilize operations and restore investor confidence.

Conclusion: A Case for Strategic Buy-In

While the UBSUBS-- downgrade has triggered a short-term selloff, Hess Midstream's valuation appears misaligned with its fundamentals and the sector's long-term trajectory. The company's forward EV/EBITDA of 5.97x suggests a margin of safety, while midstream infrastructure demand and regulatory support create a durable floor for earnings. For investors willing to look beyond near-term volatility, this decline may represent an opportunity to capitalize on a sector poised for structural growth.

Comentarios

Aún no hay comentarios