Heron Therapeutics' $125M Mixed Shelf Filing: Strategic Capital Access and Growth Implications

Heron Therapeutics (NASDAQ:HRTX) has navigated a complex financial landscape in 2025, balancing debt reduction with strategic investments in its core therapeutic areas. The company's recent $125 million mixed securities shelf filing, announced in 2025[1], has sparked investor interest as a potential catalyst for growth. However, a closer examination of Heron's capital allocation and operational performance reveals a nuanced picture of how this financing aligns with its oncology and acute care expansion goals.

Strategic Capital Access: Flexibility Over Immediate Use

Heron's mixed shelf filing, part of its broader capital strategy, grants the company flexibility to raise funds in various forms—common stock, debt, or a combination—as market conditions evolve[1]. While the filing itself does not explicitly detail how proceeds will be allocated to oncology or acute care, the company's August 2025 capital restructuring provides critical context. This restructuring reduced total debt from $175 million to $145 million, extended maturities to 2030, and secured $110 million in new financing from Hercules Capital[2]. These moves prioritize financial stability, freeing up resources to fund commercial initiatives in high-growth areas like acute care.

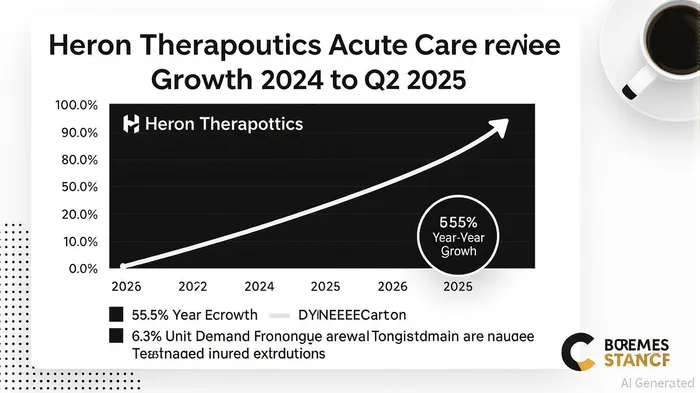

The acute care segment has been a standout performer. In Q2 2025, HeronHRTX-- reported a 55.5% year-over-year revenue increase in this segment, driven by ZYNRELEF and APONVIE[2]. ZYNRELEF's unit demand grew by 6.3% sequentially in Q2 2025, bolstered by a reorganized sales team and the introduction of a Vial Access Needle (VAN) to streamline hospital workflows[2]. APONVIE also saw a 19% rise in unit demand, reflecting growing adoption in hospital systems[2]. These gains underscore the acute care franchise's potential to drive long-term value, even as the oncologyTOI-- segment faces headwinds.

Oncology Challenges and Capital Prioritization

Heron's oncology segment, however, has underperformed. Revenue declined 9.0% year-over-year in Q2 2025, with SUSTOL and CINVANTI contributing to the weakness[2]. While the mixed shelf filing could theoretically support oncology R&D or product differentiation, the company's recent capital allocation has focused on stabilizing its balance sheet and accelerating acute care growth. For instance, the August 2025 restructuring included retiring $125 million in convertible notes and issuing $35 million in new 5.0% senior convertible notes due 2031[2]. These actions suggest a deliberate shift toward preserving liquidity for high-impact opportunities rather than broad-based expansion.

Market Implications and Investor Considerations

The mixed shelf filing's strategic value lies in its flexibility. By maintaining access to capital, Heron can respond to market dynamics—such as the October 2025 implementation of a permanent reimbursement code for ZYNRELEF[2]—which is expected to further boost acute care revenue. However, investors should remain cautious. The absence of detailed SEC filings specifying oncology/acute care allocations for the $125M offering raises questions about the immediacy of its impact[3]. For example, Caribou Biosciences' 2025 shelf filing (unrelated to Heron) highlights broad management discretion in allocating proceeds[3], a precedent that could apply to Heron's filing.

Conclusion: A Calculated Path Forward

Heron's capital strategy in 2025 reflects a calculated prioritization of acute care momentum and financial resilience. While the $125M mixed shelf filing offers a tool for future growth, its direct impact on oncology expansion remains speculative. Investors should monitor how the company leverages this flexibility, particularly as it seeks to address oncology challenges and capitalize on acute care tailwinds. For now, Heron's focus on debt reduction and acute care commercialization appears well-aligned with its operational strengths.

Comentarios

Aún no hay comentarios