Health Care Sector Volatility and Strategic Entry Points: Valuative Resilience Amid Near-Term Corrections

The health care sector in 2025 has emerged as a study in contrasts: a defensive industry grappling with near-term headwinds while simultaneously showcasing long-term resilience. Year-to-date returns for the sector stand at -1.11% as of June 2025, underperforming the broader market amid regulatory uncertainty, trade policy shifts, and supply chain fragility in key markets like China, according to a Morgan Stanley report. Yet, beneath this volatility lies a sector whose fundamentals remain anchored by demographic tailwinds and therapeutic innovation. For investors, the challenge lies in distinguishing between transient pain and enduring value.

Drivers of Near-Term Volatility

The sector's struggles in 2025 stem from a confluence of factors. Regulatory pressures, particularly around drug pricing and tariffs under the Trump administration, have disproportionately impacted pharmaceutical firms and managed care organizations. UnitedHealth GroupUNH--, for instance, has faced margin compression due to policy-driven reimbursement adjustments, the Morgan Stanley report notes. Meanwhile, life sciences firms like Thermo FisherTMO-- and DanaherDHR-- have contended with weakening demand from China, where lockdowns and economic slowdowns have dampened research and diagnostic spending, per the Morgan Stanley report.

Compounding these challenges, the venture capital landscape reveals a market in flux. According to Rock Health's Q3 overview, Q3 2025 saw $3.5 billion in healthcare venture funding-bringing year-to-date totals to $9.9 billion-the pace of fundraising has become uneven. The median time between Series A and B rounds now stretches to 27 months, up from 17 in 2023, reflecting investor caution and extended due diligence. Mega deals, however, have persisted, with 19 financings exceeding $100 million in 2025 alone. The Rock Health overview highlights that these include landmark rounds for Strive Health ($550M) and Judi Health ($400M), underscoring capital's focus on scalable infrastructure and workflow solutions.

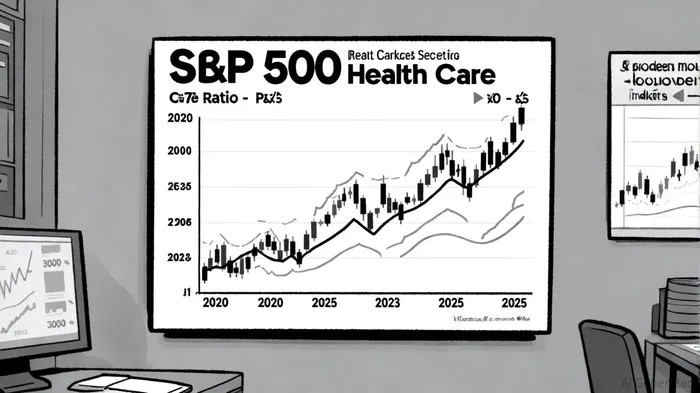

Valuative Resilience: A Historical Perspective

To assess the sector's resilience, one must compare current valuations to those during past corrections. As of September 2025, the S&P 500 Health Care Sector trades at a forward P/E ratio of 24.87, comfortably within its five-year average range of 18.20–28.04, per S&P 500 Health Care P/E data. This compares favorably to the 2008 financial crisis, when the sector's inelastic demand shielded it from the S&P 500's -57% peak-to-trough decline, according to an Invest Quest analysis. During the 2020 pandemic, the sector's P/E ratio hit 22.7-a relatively moderate multiple despite pandemic-driven volatility, per S&P 500 valuation multiples.

The current forward P/E of 24.87 suggests the market is pricing in cautious optimism. While earnings growth has slowed due to cost pressures, the sector's defensive characteristics-driven by aging demographics and non-discretionary demand-remain intact. That P/E data also suggests dividend yields are likely to retain their appeal as investors seek income in a high-interest-rate environment.

Strategic Entry Points: Navigating the Correction

For investors, the key to capitalizing on this correction lies in segment-level differentiation. Three areas stand out:

Digital Health and Workflow Innovation:

The shift toward healthcare workflows and infrastructure has captured 42% of sector funding in 2025, with clinical and non-clinical tools leading the charge, per the Rock Health overview. Startups leveraging AI-driven diagnostics or interoperability platforms are well-positioned to benefit from this trend.Locum Tenens and Staffing Solutions:

With labor shortages persisting, locum tenens staffing is projected to grow at 6% in 2025 and 5% in 2026, the Morgan Stanley report indicates. Firms specializing in temporary physician placements or AI-powered workforce management could see outsized demand.GLP-1-Driven Therapeutic Innovation:

Obesity treatments like GLP-1 agonists represent a paradigm shift in chronic disease management. Companies with robust pipelines in this space-such as Novo Nordisk and Eli Lilly-are likely to see long-term outperformance despite near-term regulatory scrutiny, the Morgan Stanley report suggests.

Risks and Considerations

Investors must remain mindful of macroeconomic headwinds. The Inflation Reduction Act's (IRA) cost controls, coupled with potential interest rate hikes, could pressure margins for payers and providers, according to a McKinsey analysis. Additionally, the "missing middle" in mid-stage financing-exacerbated by extended funding timelines-may delay the commercialization of promising technologies, the Rock Health overview warns.

Conclusion

The health care sector's 2025 volatility is a function of short-term policy and macroeconomic forces, not a fundamental shift in its long-term trajectory. With valuations anchored by historical norms and innovation pipelines intact, the current correction offers a disciplined entry point for investors who can differentiate between cyclical pain and structural opportunity. As the sector navigates these crosscurrents, those who focus on resilient sub-industries-digital health, staffing solutions, and therapeutic innovation-may find themselves well-positioned for the recovery.

Comentarios

Aún no hay comentarios