GSST: A Strategic Middle Ground Between U.S. Treasury Bills and Corporate Credit

In the ever-evolving landscape of fixed-income investing, the Goldman Sachs Ultra Short Bond ETF (GSST) has emerged as a compelling hybrid, bridging the gap between the safety of U.S. Treasury Bills (T-Bills) and the yield potential of corporate credit. As investors navigate a post-pandemic economy marked by shifting interest rates and credit spreads, GSSTGSST-- offers a strategic middle ground—balancing capital preservation with income generation. This analysis explores how GSST's structure, risk profile, and performance metrics position it as a nuanced alternative to traditional short-term government securities and corporate bonds.

Understanding GSST: Structure and Objectives

GSST is an actively managed exchange-traded fund (ETF) that invests in a diversified portfolio of short-term, investment-grade debt, including U.S. Treasury securities, securitized debt, and corporate bonds. Its portfolio is engineered to maintain an effective duration of one year or less, minimizing exposure to interest rate fluctuations while prioritizing liquidity and credit quality [1]. Unlike T-Bills, which are direct obligations of the U.S. government with fixed maturities, GSST's holdings include a broader range of securities, allowing it to generate higher yields without sacrificing safety. For instance, GSST's 1-year return of 5.24% as of 2025 outperforms the typical 2–3% yields of T-Bills, while its volatility remains exceptionally low at 0.50% [2].

Risk and Return: A Nuanced Trade-Off

The key distinction between GSST and corporate bonds lies in risk exposure. Corporate bonds, particularly high-yield (junk) bonds, offer higher returns but come with elevated credit and default risks. From 2020 to 2025, corporate bonds saw tighter credit spreads due to strong earnings and low default rates, reducing their risk premium [3]. However, even investment-grade corporate bonds carry greater volatility than GSST. For example, speculative-grade corporate bonds experienced mixed credit quality in 2025, with some issuers facing refinancing risks and downgrades [4]. In contrast, GSST's focus on short-term, investment-grade debt ensures minimal credit risk, making it a safer alternative to corporate bonds without sacrificing yield.

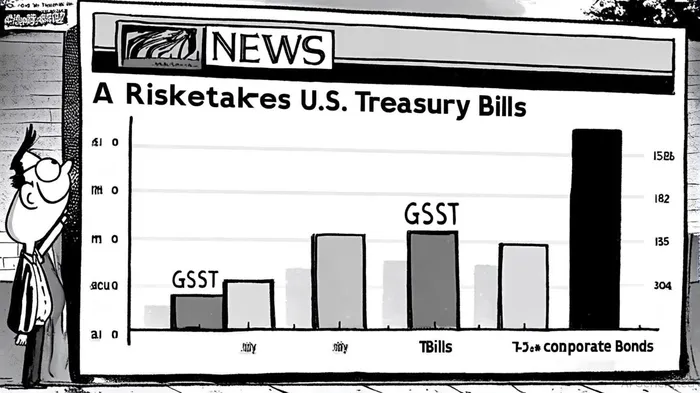

Risk-Adjusted Returns: The Sharpe Ratio Advantage

GSST's superior risk-adjusted returns are underscored by its Sharpe ratio of 6.83 for the 1-year period ending in 2025—a stark contrast to corporate bonds, which typically have Sharpe ratios ranging from 0.5 to 1.2 [5]. This metric highlights GSST's ability to generate substantial returns relative to its minimal volatility, outperforming both T-Bills and corporate bonds. T-Bills, while nearly risk-free, offer negligible Sharpe ratios due to their low yields, whereas corporate bonds, despite higher returns, are penalized for their added volatility and credit risk. GSST's high Sharpe ratio reflects its unique positioning: it captures incremental yield from corporate-like securities while mitigating downside risks through short maturities and active management [6].

Market Context: 2020–2025 Dynamics

The narrowing credit spreads between corporate and government bonds since 2020 have complicated investment decisions. Investors historically demanded higher yields from corporate bonds to compensate for additional risk, but this premium has diminished as economic resilience and low default rates reduced perceived risks [3]. Meanwhile, concerns over U.S. government debt and a 2023 Moody's downgrade of Treasuries have introduced uncertainty into the safety of long-term government bonds [7]. GSST, with its ultra-short duration and diversified holdings, thrives in such environments. It avoids the interest rate sensitivity of longer-term bonds while sidestepping the credit risks of corporate debt, making it an attractive option during periods of macroeconomic volatility.

Strategic Implications for Portfolios

For conservative investors, GSST serves as a versatile tool to enhance portfolio resilience. Its low volatility and high Sharpe ratio make it ideal for capital preservation, while its yield advantage over T-Bills provides a buffer against inflation. In contrast to corporate bonds, GSST reduces the need for extensive credit analysis, as its holdings are pre-vetted for investment-grade quality. This makes it particularly appealing to institutional investors and retail investors seeking simplicity and stability. Furthermore, GSST's liquidity and low fees (0.15% expense ratio) enhance its appeal as a cost-effective alternative to actively managed corporate bond funds [8].

Conclusion

GSST exemplifies the growing demand for middle-ground solutions in fixed-income investing. By blending the safety of government-backed securities with the yield potential of corporate credit, it addresses the limitations of both asset classes. Its exceptional risk-adjusted returns, as evidenced by its Sharpe ratio, and its adaptability to shifting market conditions position it as a strategic cornerstone for investors prioritizing stability and income. As the 2020s transition into the 2030s, GSST's role as a balanced alternative will likely grow in relevance, particularly in an environment where traditional safe-haven assets face structural challenges.

Comentarios

Aún no hay comentarios