Growth Equity in Q3 2025: Uncovering Undervalued Tech Opportunities in a Shifting Landscape

The Q3 2025 growth equity market is navigating a complex inflection point. While private equity firms are cautiously optimistic about capital deployment, the sector's recovery remains uneven, with stark contrasts between late-stage AI-driven tech startups and small-mid buyouts. For investors seeking undervalued opportunities, the current environment offers a unique window to identify scalable private tech companies that align with long-term macro trends.

A Market in Transition: Recovery, Selectivity, and AI's Dominance

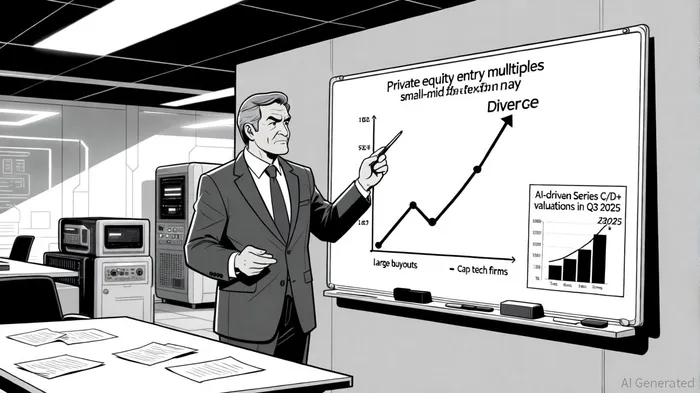

According to a Schroders Capital report, private equity fundraising in Q3 2025 has shown signs of stabilization, with capital increasingly favoring "proven strategies" and large buyouts over speculative bets. However, venture and growth equity fundraising remain subdued, reflecting lingering caution in early-stage investing. This selectivity has created a bifurcated market: while AI-focused tech startups in Series C and D+ rounds command inflated valuations, small-mid buyouts trade at a persistent 40–50% discount to their public market counterparts, a trend the Schroders Capital report highlights.

The shift toward AI is not merely speculative. As highlighted in Akin Gump's 2025 Perspectives, generative AI is now a strategic tool for enhancing operational efficiency in portfolio companies, rather than a standalone investment theme. This trend has spurred demand for energy-efficient infrastructure and cybersecurity solutions, creating new pockets of value in sectors like data centers and SaaS - with Blackstone's $16 billion acquisition of Airtrunk in Q3 2024 underscoring the sector's strategic importance.

Identifying Undervalued Tech Companies: Key Criteria

To pinpoint undervalued private tech firms, investors must focus on three interrelated factors: sector alignment with macro trends, operational scalability, and liquidity resilience.

Sector Alignment:

SaaS and AI infrastructure remain the most compelling areas. McKinsey's Global Private Markets Report notes that SaaS firms benefit from recurring revenue models and high gross margins, making them attractive in a higher-rate environment. Similarly, data centers are gaining traction as AI adoption accelerates, with Blackstone's $16 billion acquisition of Airtrunk in Q3 2024 underscoring the sector's strategic importance.Operational Scalability:

Undervalued companies often exhibit strong unit economics but lack the capital to scale. For example, Digital Engineering firms like CI&T are projected to deliver 2026 revenue growth rates exceeding 25%, trading at 12x revenue multiples-a premium to peers but justified by their ability to monetize AI-driven digital transformation, a dynamic noted in the Schroders Capital report. Investors should prioritize firms with defensible market positions and clear paths to EBITDA expansion.Liquidity Resilience:

With public market exits remaining muted, continuation funds and secondary transactions are becoming critical liquidity tools, a point the Schroders Capital report emphasizes. This dynamic favors companies with diversified capital structures and strong sponsor relationships. Small-mid buyouts, despite their valuation discounts, offer attractive risk-adjusted returns due to their ability to rapidly improve operating performance, as McKinsey's report also observes.

The Scalable Business Model Playbook

For growth equity investors, the focus must shift from pure revenue growth to profitability-driven scalability. The Schroders Capital report highlights that AI-driven deals in later-stage rounds have outperformed, with valuations rising 18% year-to-date. This suggests that investors are prioritizing companies with tangible use cases for AI, such as automation in supply chains or predictive analytics in healthcare.

Moreover, the energy-efficient infrastructure segment is gaining traction. As AI workloads surge, firms that provide low-carbon data storage or edge computing solutions are attracting capital. These companies benefit from both technological and regulatory tailwinds, making them prime candidates for undervaluation in the current market.

Conclusion: Navigating the Q3 2025 Opportunity Set

The Q3 2025 growth equity landscape is defined by duality: optimism in AI and SaaS, tempered by caution in early-stage and venture capital. For investors, the path to outperformance lies in identifying private tech companies that combine sector relevance, scalable unit economics, and liquidity resilience. While the market remains selective, the current valuation discounts in small-mid buyouts and the surge in AI-driven innovation present a compelling case for strategic capital deployment.

As interest rates stabilize and credit markets ease, the next 12–18 months could see a surge in take-private activity and cross-border tech deals. Investors who act now-targeting undervalued firms with defensible moats and AI-enabled growth-will be well-positioned to capitalize on the next phase of the private equity cycle.

Comentarios

Aún no hay comentarios