Mr D.I.Y. Group: A Tale of Growth and Valuation Divergence

In the world of retail, few stories have captivated investors as much as that of Mr D.I.Y. Group (KLSE:MRDIY). The Malaysian discount retailer has become a symbol of resilience and growth, expanding its footprint to 190 new stores in 2025 alone while navigating macroeconomic headwinds, according to a Yahoo Finance report. Yet, as the company's stock price hovers near RM1.62 as of September 28, 2025, according to its historical price page, a critical question emerges: Is the market overpaying for its success, or is there room for further appreciation?

The Fundamentals: A Company on the Rise

Mr D.I.Y. Group's financial performance in 2025 has been nothing short of stellar. For the first quarter of the fiscal year ending December 2025, net profit surged 20.2% year-over-year to RM174.15 million, driven by festive sales, margin improvements, and aggressive store expansion (per the company's historical price page). Second-quarter results, while slightly softer at RM158.6 million, still outperformed expectations, with management attributing the dip to seasonal fluctuations rather than structural issues, as noted in an i3investor overview.

The company's balance sheet is equally robust. A current ratio of 2.24 and a debt-to-equity ratio of 0.73, according to StockAnalysis, suggest prudent financial management, while a return on equity (ROE) of 31.33% underscores its ability to generate shareholder value. These metrics paint a picture of a well-capitalized, high-margin business with a clear strategy for scaling.

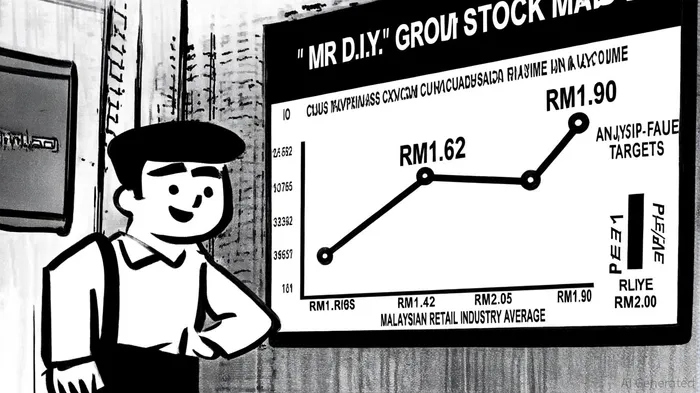

Intrinsic Value: The DCF Divide

To assess whether the stock is fairly valued, we turn to intrinsic value estimates. A two-stage discounted cash flow (DCF) model from Simply Wall St suggests a fair value of RM1.42 per share, based on projected free cash flows of RM7.7 billion over the next decade and a terminal value of RM12 billion. This implies that the current market price of RM1.62 is trading at a 14% premium to that intrinsic value. However, another DCF analysis from ValueInvesting.io arrives at a starkly different conclusion, estimating a fair price of RM0.82, which would suggest a 100% overvaluation.

The discrepancy between these models highlights the uncertainty surrounding Mr D.I.Y.'s long-term growth prospects. The higher DCF estimate assumes continued expansion and margin stability, while the lower estimate incorporates more conservative assumptions about market saturation and operational risks. Analysts, meanwhile, offer a middle ground: a consensus price target of RM1.90-32% above the Simply Wall St DCF fair value-reflects confidence in the company's ability to outpace industry growth (per the Yahoo Finance report).

Valuation Ratios: A Mixed Picture

Mr D.I.Y.'s valuation multiples tell a nuanced story. The stock trades at a forward P/E ratio of 23.40, which appears elevated when compared to the Malaysian retail industry's average P/E of 33.96. However, this ratio is significantly lower than the broader Malaysia Stock Market's P/E of 13.90, suggesting that the retail sector is being valued at a premium relative to the overall market.

The PEG ratio of 2.08 further complicates the picture. While the company's earnings are growing at a healthy clip (6–10% in 2025, per the Yahoo Finance report), the PEG ratio implies that the stock is overvalued relative to its growth rate. This divergence between fundamentals and multiples is a classic sign of valuation mispricing-a situation where market sentiment either overestimates or underestimates a company's future potential.

The Road Ahead: Growth vs. Caution

Mr D.I.Y. Group's management remains optimistic, citing a 14–17% annualized revenue growth forecast-well above the industry's 7.6% average, according to the Yahoo Finance report. With 190 new stores planned for 2025, the company is betting on its ability to capture market share in Malaysia's USD 94.99 billion retail sector. Yet, this expansion comes with risks. The retail industry is notoriously competitive, and rising U.S. tariffs on Malaysian exports could indirectly impact consumer spending (the company's historical price page discusses related macroeconomic notes).

For investors, the key question is whether the current valuation reflects these risks. At RM1.62, the stock sits between the DCF estimates of RM1.42 and RM2.05, and below the analyst price target of RM1.90. This suggests that while the market acknowledges the company's strengths, it may not be fully pricing in its long-term potential.

Conclusion: A Stock at a Crossroads

Mr D.I.Y. Group embodies the tension between growth and valuation. Its financials are strong, its expansion plans ambitious, and its market position secure. Yet, the stock's P/E and PEG ratios, coupled with divergent DCF estimates, signal a valuation that is neither clearly undervalued nor grossly overpriced.

For value investors, the RM1.42 DCF fair value represents a potential entry point if the stock corrects. For growth-oriented investors, the analyst price target of RM1.90 offers a compelling upside, provided the company can sustain its expansion and margin discipline. In the end, Mr D.I.Y.'s story is a reminder that intrinsic value is not a fixed number-it is a moving target shaped by both numbers and narrative.```

Comentarios

Aún no hay comentarios