Grindr's Take-Private Strategy and Its Implications for Tech Turnarounds

The recent turmoil in Grindr's capital structure has thrust the LGBTQ+ dating app into the spotlight as a case study for tech turnarounds in an era of heightened regulatory scrutiny. With its majority shareholders-Raymond Zage and James Lu-exploring a $15-per-share buyout backed by Fortress Investment Group, the company's path to privatization underscores the delicate interplay between private equity value creation and the constraints of post-PRC (People's Republic of China) regulatory environments. This analysis examines how Grindr's strategy reflects broader trends in tech company restructurings, while highlighting the unique challenges posed by cross-border ownership dynamics and evolving governance frameworks.

Financial Pressures and Capital Structure Rebalancing

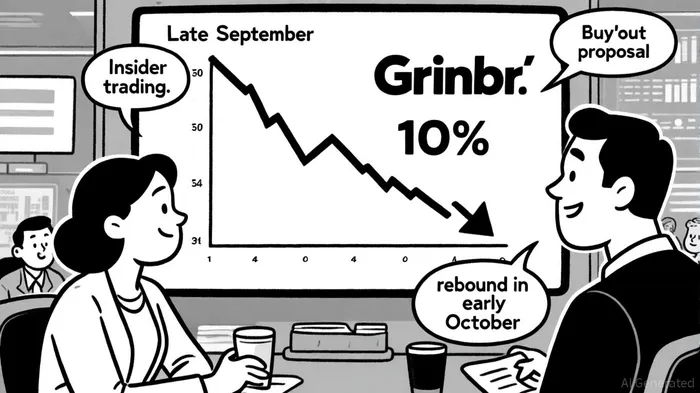

Grindr's decision to pursue a take-private transaction stems from a perfect storm of financial and regulatory pressures. According to a report by Invezz, the company's stock plummeted in late September 2025 after Zage and Lu, who collectively control 60% of GrindrGRND--, faced margin calls from a Temasek Holdings unit[2]. The forced sale of pledged shares exacerbated market volatility, eroding investor confidence and triggering a scramble to stabilize ownership. Fortress Investment Group's proposed $3 billion buyout-valuing Grindr at a 30% premium to its recent trading price-aims to insulate the company from short-term market swings while preserving its mission-driven focus[3].

This move aligns with a broader private equity playbook: leveraging debt to depersonalize ownership and refocus management on long-term value creation. However, the transaction's success hinges on Grindr's ability to navigate regulatory hurdles, particularly in markets where foreign ownership of tech platforms is under intense scrutiny.

Navigating PRC Regulatory Complexities

Grindr's history with Chinese regulators is fraught. Acquired by a Beijing-based company in 2016, the app was sold in 2020 under U.S. Committee on Foreign Investment (CFIUS) pressure due to concerns over data privacy and national security[4]. Now, with Zage (a Singaporean national) and Lu (a U.S. citizen of Chinese descent) at the helm, the company faces renewed scrutiny under China's 2023 Company Law amendments[5]. These reforms, effective July 2024, mandate stricter capital contribution timelines and enhanced transparency for foreign-invested enterprises, complicating Grindr's ability to maintain its current ownership structure[6].

The PRC's negative list approach to foreign investment-now reduced to 29 restricted sectors-has also created uncertainty for tech firms. While Grindr is not explicitly barred from operating in China, its data collection practices and LGBTQ+ focus place it in a gray area. As noted in a Legal News Feed analysis, Grindr's General Counsel has emphasized proactive alignment with "technological innovation and privacy norms," a balancing act that may prove challenging in markets where LGBTQ+ advocacy is increasingly framed as a foreign influence[1].

Private Equity Value Creation in Regulated Markets

The Grindr case highlights how private equity strategies must adapt to regulatory headwinds in post-PRC environments. Fortress's proposed buyout, for instance, relies on a $15-per-share offer that assumes Grindr can streamline operations and reduce compliance costs. This mirrors broader trends in tech turnarounds, where private equity firms prioritize operational efficiency and data governance to unlock value[3].

However, the PRC's evolving regulatory landscape introduces asymmetries. For example, the 2024 revision of the Company Law requires foreign investors to contribute registered capital within five years-a constraint that could limit Grindr's flexibility in scaling its international operations[5]. Similarly, the U.S. government's 2025 outbound investment rules, which restrict U.S. persons from investing in PRC firms involved in AI or semiconductors, could complicate Grindr's access to critical technologies[7].

Implications for Tech Turnarounds

Grindr's experience offers three key lessons for tech companies navigating regulated markets:

1. Capital Structure Flexibility: Privatization can shield firms from short-term volatility but requires robust liquidity to meet regulatory capital requirements.

2. Regulatory Proactivity: Companies must anticipate shifts in foreign investment laws, particularly in sectors tied to national security or data privacy.

3. Mission Alignment: Maintaining a clear value proposition-such as Grindr's commitment to LGBTQ+ communities-can mitigate reputational risks in politically sensitive markets[6].

For private equity firms, the Grindr deal underscores the importance of structuring transactions to address cross-border regulatory risks. By embedding compliance frameworks into due diligence processes, investors can better navigate the complexities of post-PRC markets while preserving long-term value.

Conclusion

Grindr's take-private strategy is emblematic of a broader shift in tech turnarounds, where capital structure decisions are increasingly intertwined with regulatory and geopolitical factors. As PRC regulations continue to evolve, companies and investors must adopt a dual focus: optimizing financial performance while aligning with the legal and social norms of their operating environments. In this context, Grindr's success-or failure-could serve as a bellwether for the viability of tech turnarounds in an era of global regulatory fragmentation.

Comentarios

Aún no hay comentarios