Greenbrier's Beat vs. Headwinds: A Tactical Look at the Q1 Catalyst

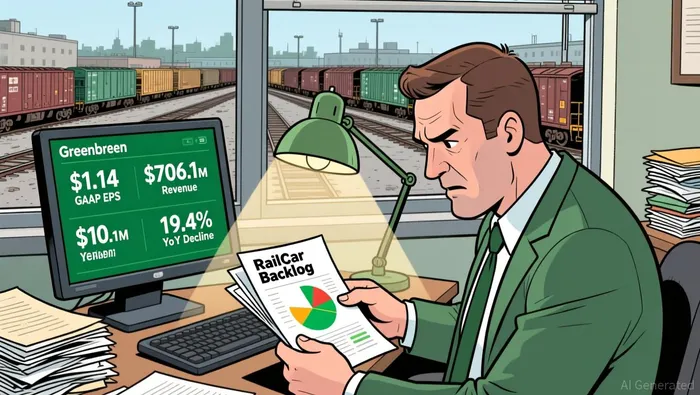

The specific event is clear: Greenbrier's first-quarter results for fiscal 2026, released earlier this week. The company posted a significant earnings beat, with GAAP EPS of $1.14 that crushed the analyst consensus estimate of $0.87 by 31%. Revenue also topped expectations, coming in at $706.1 million against estimates of $655.6 million. Yet this positive surprise came alongside a stark reality: sales fell 19.4% year on year and the company delivered 4,400 railcars against a backlog of 16,300 units.

The immediate market reaction was a classic "sell the news" scenario. The stock initially popped 5.39% in after-hours trading on the beat. But that momentum quickly faded. By mid-day Friday, shares were down 6.1% on the session, trading at around $50.09. The move was accompanied by a notable lack of interest, with volume 73% below average. This pullback sets the tactical stage. The earnings beat itself may not have fundamentally altered the company's valuation, but it did create a temporary mispricing-a gap between the strong quarterly execution and the market's cautious forward view.

The real catalyst here is the disconnect between the reported beat and the broader operational weakness. While management highlighted "resilience" and disciplined cost controls, the underlying trends are clear. Core EBITDA and operating profit fell sharply year-over-year, and the company has trimmed its full-year EPS guidance to a range that sits below analyst consensus. For an event-driven strategist, this is the setup. The market is focusing on the guidance cut and the 19% revenue decline, overshadowing the fact that GreenbrierGBX-- still generated a profit and beat on the bottom line. This creates a potential opportunity where the event's market impact-driven by the beat-may be more significant than any fundamental valuation shift, at least in the near term.

Assessing the Quality of the Beat and Guidance

The earnings beat was real, but its quality hinges on the drivers. Greenbrier posted a 15% aggregate gross margin for the quarter, a key metric that demonstrates the resilience of its integrated model. This margin, coupled with operating income of $61 million and operating cash flow of $76 million, shows the company generated strong cash despite a challenging sales environment. The cash flow figure is particularly telling, providing a buffer and funding the $13 million in stock repurchases during the period.

Yet the top-line story is mixed. While revenue beat estimates, sales volumes fell 2.6% year-on-year. This decline underscores the core headwind: customers remain cautious about capital spending. The beat was achieved through disciplined cost control and margin management, not volume growth. The company secured roughly 3,700 railcar orders late in the quarter, but the backlog of 16,300 units is essentially flat in value, indicating the order pipeline is not yet translating into a production ramp.

Forward guidance provides the clearest signal on sustainability. Management reiterated a full-year revenue range of $2.7 to $3.2 billion, with a midpoint of $2.95 billion that sits 2.1% above analyst estimates. However, the guidance includes a critical qualifier: production is being moderated, with headcount adjusted, primarily in Mexico. This is a direct acknowledgment of weak demand. The company is managing output to align with current orders, which caps near-term growth.

The leasing business is the key stabilizer. With nearly 98% fleet utilization and double-digit renewal increases, it provides a steady, high-margin revenue stream that buffers the cyclical manufacturing side. This integrated model is designed to deliver "higher lows through the cycle," as management noted. For the beat to be sustainable, this leasing engine must continue to perform while manufacturing finds its footing.

The risk/reward here is tactical. The beat shows operational discipline and a solid cash-generating base, which supports the stock's intrinsic value. But the guidance cut and moderated production signal that the fundamental recovery is not yet underway. The market's initial sell-off on the guidance may have been overdone, but the path to a re-rating requires visible growth in manufacturing orders and deliveries, not just margin maintenance. The event created a mispricing on the beat, but the setup for a sustained move depends on the leasing business holding up and manufacturing demand picking up later in the year.

Catalysts and Risks: What to Watch Next

The tactical setup hinges on the next major catalyst: the second-quarter earnings report, expected in April. That release will be the first real test of whether the late-quarter order momentum can translate into visible production and delivery growth. Investors will be watching two key metrics. First, any acceleration in new railcar orders beyond the roughly 3,700 units secured late in Q1 will signal demand is stabilizing. Second, they will scrutinize cost control progress, as management has flagged expectations for margin improvement in the second half of the year as production scales.

The primary risk remains the ongoing weakness in new railcar orders. Management attributes this to customer caution, citing improved rail service and reduced near-term demand pressure for new rolling stock. This headwind is real and has forced the company to moderate production and adjust headcount, primarily in Mexico. The stock's low volume and volatility on the day of the earnings release-trading at 73% below average-suggests the market is waiting for a clearer signal before committing capital. This lack of interest creates potential for a sharp move, either up or down, on the next catalyst.

For a tactical outlook, the post-earnings pullback creates a potential buying opportunity, but only if the core thesis holds. The integrated leasing business, with nearly 98% fleet utilization, provides a critical buffer. If that stabilizer continues to perform while manufacturing finds its footing later in the year, the stock could re-rate. However, the path is not straightforward. The company has trimmed its full-year EPS guidance to a range that sits below consensus, and the fundamental recovery is not yet underway. The event-driven trade here is a bet on the beat's quality and the leasing engine, not on near-term volume growth.

The bottom line is one of patience. The April report is the next clear signal. Until then, the stock's low volume and the persistent operational headwinds mean the setup favors a wait-and-see stance. A decisive break above the recent trading range, supported by stronger order data, would be needed to confirm the pullback was a mispricing.

Comentarios

Aún no hay comentarios