Grail Insider Selling Shares: A Red Flag or Strategic Reallocation?

In the world of biotech investing, insider selling often sparks debate. For GRAILGRAL--, Inc. (NASDAQ: GRAL), the recent wave of executive and major shareholder transactions has drawn particular scrutiny. Between May and October 2025, insiders-including President Joshua J. Ofman, CEO Robert P. Ragusa, and major shareholder Chun R. Ding-sold over 706,000 shares, generating more than $26.4 million in proceeds, according to MarketBeat insider trades. While some of these sales occurred under Rule 10b5-1 trading plans-designed to insulate transactions from accusations of market timing-others, such as Ofman's June 30 sale at $52 per share (a 54% premium over his May price), suggest a more opportunistic approach, as noted in an EdgarIndex analysis.

Insider Selling: Context and Patterns

The most notable recent transaction involved Ofman, who sold 9,692 shares at $64.00 on October 2, 2025, reducing his direct ownership stake by 1.99% to 478,182 shares, according to a MarketBeat alert. This followed multiple sales earlier in the year, including a $52.00-per-share transaction in June. Similarly, Ragusa sold 94,035 shares at $33.93 in May, while CFO Aaron Freidin liquidated 41,150 shares at the same price, per Yahoo Finance insider transactions. These actions, combined with Ding's large-scale sales (e.g., 339,800 shares at $49.53 on July 1), underscore a pattern of significant insider divestment.

Critically, many of these transactions were executed under Rule 10b5-1 plans, which require pre-established guidelines and public disclosure. As documented in an SEC Form 4 filing, such plans are intended to ensure transparency and reduce the risk of insider trading allegations. However, the sheer volume of sales-and their timing relative to key company developments-raises questions about whether these moves reflect strategic portfolio management or a lack of confidence in GRAIL's near-term prospects.

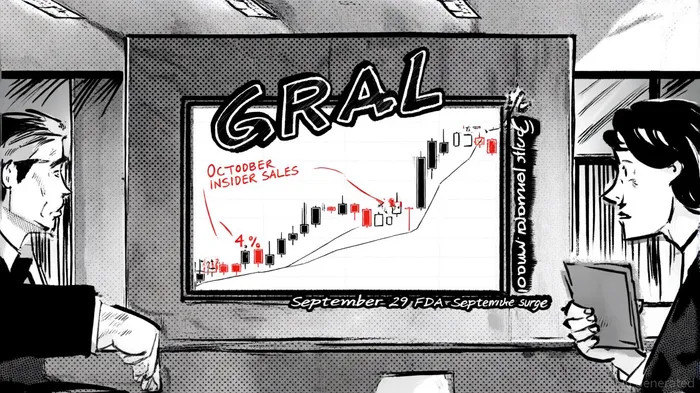

Stock Price Reactions and Investor Sentiment

GRAIL's stock price has shown mixed responses to these insider sales. Following Ofman's October 2 transaction, shares fell 4% to $62.95 by October 6, 2025. This decline contrasted with a 17.33% surge on September 29, driven by a major FDA milestone in the NHS-Galleri Trial, which demonstrated a higher positive predictive value (PPV) than earlier studies, as reported in a GRAIL press release. Analysts questioned whether the spike would sustain, according to a Timothy Sykes note. The stock closed at $58.77 after opening at $50.65 that day, reflecting heightened optimism about GRAIL's multi-cancer early detection (MCED) technology.

Analyst sentiment remains divided. While some, like Canaccord Genuity, raised price targets to $75.00 with a "Buy" rating, others maintain a "Hold" stance, with an average price target of $47.50 implying a projected -34.74% decline over the next year, per the StockAnalysis forecast. Meanwhile, retail investor sentiment is bullish: AltIndex sentiment reports a 100/100 score for GRAIL, indicating strong online forum enthusiasm. This divergence highlights the tension between institutional caution and retail optimism.

Financial Health and Strategic Momentum

Despite the insider selling, GRAIL's financials and strategic initiatives present a compelling case for long-term resilience. The company reported a 19% year-over-year revenue increase in Q1 2025, with U.S. Galleri sales reaching $28.7 million, according to a Seeking Alpha article. Its cash reserves of $677.9 million provide a runway through 2028, supporting clinical trials and commercial expansion. Strategic partnerships, including automation upgrades and collaborations with athenahealth, are streamlining test access and ordering processes, per a StocksToTrade report.

Moreover, GRAIL's recent clinical data-such as the Prevalent Screening Round results from the NHS-Galleri Trial-underscore its progress in validating MCED technology. The company plans to submit registrational data from the PATHFINDER 2 study in late 2025 and aims for premarket approval by mid-2026, according to the MarketBeat forecast. These milestones could catalyze renewed investor confidence, particularly if regulatory hurdles are cleared.

Balancing the Signals

The key question for investors is whether GRAIL's insider selling represents a red flag or a rational reallocation of wealth. On one hand, the cumulative $26.4 million in insider proceeds suggests executives may be hedging against perceived risks. On the other, the company's strong cash position, revenue growth, and strategic advancements indicate a firm foundation for long-term value creation.

Institutional investors appear to share this nuanced view. UBS Asset Management and AQR Capital Management have increased stakes in GRAIL, while analysts like those at StockAnalysis acknowledge the stock's volatility but highlight its potential for recovery, per an Intellectia forecast. The challenge for retail investors lies in distinguishing between short-term noise and long-term fundamentals.

Conclusion

GRAIL's insider selling activities warrant careful scrutiny but should not be interpreted in isolation. While the pattern of transactions raises valid concerns, the company's financial health, regulatory progress, and strategic momentum provide a counterbalance. Investors should monitor upcoming data submissions and partnership developments, which could either validate or undermine current sentiment. For now, GRAIL remains a stock of both risk and reward-a reflection of the high-stakes nature of the biotech sector.

Comentarios

Aún no hay comentarios