Gold's Record Rally: Positioning for a Fed-Driven Bull Market

The gold market is experiencing a historic rally, with prices surging to $3,642.45 per troy ounce as of September 2025—a 44.62% increase year-to-date and a 87.23% rise over the past five years [1]. This surge is not merely a short-term anomaly but a reflection of deepening macroeconomic shifts: Federal Reserve policy uncertainty, U.S. dollar weakness, and a global reallocation of reserves toward tangible assets. For investors, the case for strategic gold allocation has never been stronger.

The Fed’s Policy Tightrope and Gold’s Response

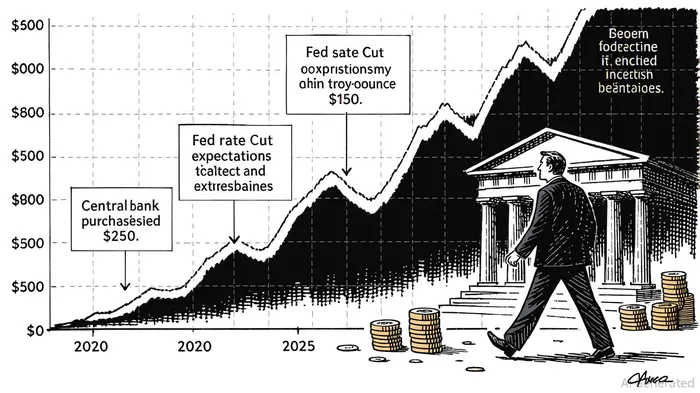

The Federal Reserve’s cautious stance—keeping rates in a 4.25%–4.50% range as of July 2025—has failed to quell market expectations of rate cuts. Weaker labor data and inflation pressures tied to tariffs have pushed the probability of 2.5 rate cuts in 2025 to near certainty [3]. Gold, historically inversely correlated with real interest rates, has thrived in this environment. Lower rates reduce the opportunity cost of holding non-yielding assets like gold, while easing monetary policy fuels inflation hedging demand [1].

Goldman Sachs has warned that gold could reach $5,000 per ounce if the Fed’s institutional credibility erodes further, pushing investors away from U.S. Treasurys [1]. J.P. Morgan’s $3,675 average price forecast for Q4 2025 and $4,000 target for mid-2026 [2] underscore a consensus-driven bullish outlook. These projections hinge on structural demand from central banks and the dollar’s continued decline.

Dollar Weakness and the De-Dollarization Trend

The U.S. dollar index has fallen to 97.5 in late July 2025, its lowest in seven weeks, while the currency’s year-to-date decline of 10% marks its weakest first-half performance since 1980 [1]. This weakness is driven by U.S. growth downgrades, inflationary tariffs, and a global shift away from dollar dependence. Central banks, particularly in emerging markets, are accelerating gold purchases to diversify reserves and hedge against currency volatility.

China’s 225-tonne gold reserve addition in 2023—part of 18 consecutive months of purchases—exemplifies this trend [2]. The People’s Bank of China’s strategy reflects a broader reallocation: gold now accounts for 27% of global central bank reserves, surpassing the euro [2]. As global government debt climbs toward $34 trillion, gold’s finite supply and intrinsic value make it an attractive counterbalance to fiat currencies [3].

Historical Precedents and Strategic Allocation

Gold’s performance during past Fed policy shifts reinforces its role as a macro-hedge. In the 1970s, stagflation and negative real interest rates drove gold from $35/oz to over $800/oz [1]. Today, similar dynamics are emerging: real yields are near zero, and inflation expectations remain anchored to a weak dollar. DelMorgan & Co. notes that gold’s appeal is further amplified by geopolitical instability and concerns over currency devaluation [5].

For investors, the strategic case for gold is threefold:

1. Hedging Against Fed Policy Uncertainty: Rate cuts and prolonged low-yield environments favor gold’s price appreciation.

2. Diversification Amid Dollar Volatility: A weakening dollar reduces gold’s cost in other currencies, broadening its global demand.

3. Central Bank Demand as a Tailwind: Structural purchases from emerging markets ensure sustained upward pressure on prices.

Conclusion: Positioning for the Bull Market

Gold’s record rally is not a speculative bubble but a response to systemic risks: eroding Fed credibility, dollar devaluation, and central bank reallocation. With prices already up 39% in 2025 [1], the asset is increasingly viewed as a cornerstone of macro-resilient portfolios. Investors seeking to hedge against policy-driven volatility and currency instability should consider gold not as a speculative play, but as a strategic allocation.

**Source:[1] Gold - Price - Chart - Historical Data - News [https://tradingeconomics.com/commodity/gold][2] Gold fever: Will central banks keep driving the golden surge? [https://m.economictimes.com/news/economy/policy/gold-fever-will-central-banks-keep-driving-the-golden-surge/articleshow/123744682.cms][3] Gold as a Dollar Alternative: The Evolving Global Safe Haven [https://discoveryalert.com.au/news/gold-evolution-global-finance-2025/]

Comentarios

Aún no hay comentarios