Gold Producers' Valuation Momentum Amid a Record-High Gold Price

The gold market in 2025 is experiencing a paradox: record-high gold prices coexist with historically undervalued mining stocks. With gold trading above $3,800 per ounce, driven by macroeconomic tailwinds like geopolitical tensions, inflationary pressures, and a weakening U.S. dollar, according to a DiscoveryAlert analysis. The sector's valuation metrics tell a different story. Gold mining stocks, particularly those of mid-tier and junior producers, trade at multiples far below historical averages, creating a compelling case for strategic investors seeking contrarian opportunities, per an Investopedia roundup.

Valuation Metrics: A Tale of Two Producers

Major gold mining companies like Newmont Corp. (NEM) and AngloGold Ashanti (AU) have demonstrated resilience in a volatile market. NewmontNEM--, a blue-chip producer, trades at a P/E ratio of 15.3, reflecting its operational consistency and financial strength, according to the DiscoveryAlert analysis. AngloGold AshantiAU--, with a P/E of 29.7, has delivered a 31.3% 30-day return, underscoring its appeal to investors seeking growth amid rising gold prices, as noted in the DiscoveryAlert analysis.

However, the story diverges for junior and mid-tier producers. Agnico Eagle Mines (AEM), for instance, commands a premium valuation (P/E of 25.6) due to its exceptional revenue growth and operational efficiency, according to a Visual Capitalist chart. In contrast, McEwen Inc. (MUX) struggles with net losses, rendering traditional metrics like P/E inapplicable, a disparity highlighted by the DiscoveryAlert analysis. This disparity highlights a sector-wide trend: larger, more established companies maintain stable valuations, while smaller producers face heightened volatility.

Historical Context: A Pattern of Undervaluation

Gold mining stocks have historically traded at a discount to gold prices, a pattern that persists in 2025. Senior producers currently trade at 1.5x price-to-net asset value (P/NAV), and mid-tier producers at below 1.0x P/NAV-far below the 3.0x and 2.0–3.0x averages observed during the 2000s bull market, per the DiscoveryAlert analysis. Similarly, enterprise value to EBITDA (EV/EBITDA) multiples hover between 7x–8x, well below the 14x peaks of 2008–2010 cited in the DiscoveryAlert analysis.

This undervaluation is not new. During the 1929–1932 Great Depression, Homestake Mining outperformed the Dow Jones Industrial Average by 49% as the DJIA plummeted, according to a Crescat analysis. In 1973–1974, the Barron's Gold Mining Index surged 193% amid a 48% decline in the S&P 500, and the 2000–2002 tech boom saw gold miners lag as investors flocked to technology stocks, observations also made in the Crescat analysis. These historical cycles suggest that gold stocks often underperform during bull markets for physical gold but outperform during bear markets-a countercyclical dynamic that could favor investors today.

Divergence and Opportunity

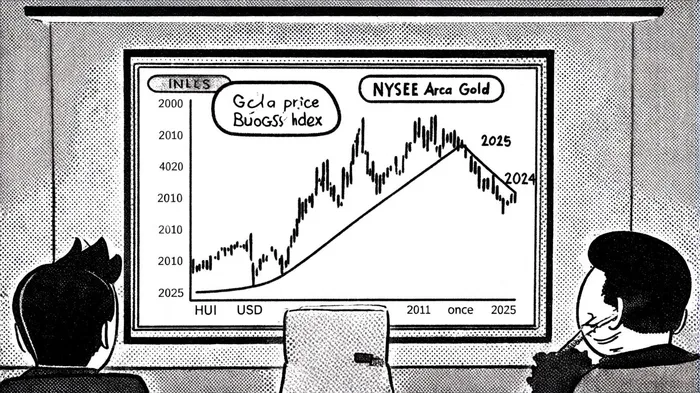

The gap between gold prices and mining stock valuations has widened in recent years. In April 2024, gold hit a record $2,062.92 per ounce, yet the NYSE Arca Gold BUGS Index (HUI) remained at $243.31, far below its 2011 peak of $498.73, a divergence illustrated by the Visual Capitalist chart. This divergence is partly due to operational inefficiencies and poor capital discipline in the sector, points also shown in the Visual Capitalist analysis. However, current fundamentals are robust: with all-in sustaining costs at $1,525 per ounce and gold prices near $3,800, mid-tier miners generate attractive free cash flow yields, as highlighted in the Visual Capitalist chart.

Investors are also overlooking the sector's structural advantages. Gold ETF allocations remain at historic lows despite rising prices, a trend noted in the Investopedia roundup, suggesting untapped demand. Meanwhile, gold mining stocks trade at EV/EBITDA multiples of 7x–8x, compared to 14x during the 2008–2010 recovery per the DiscoveryAlert analysis. This valuation dislocation presents a compelling case for mean reversion, particularly if macroeconomic conditions continue to favor gold.

Strategic Buy Opportunities

For investors, the key lies in identifying undervalued producers with strong balance sheets and operational discipline. Newmont Corp. and AngloGold Ashanti offer stability and consistent cash flows, while Agnico Eagle combines growth potential with a premium valuation justified by its efficiency. Junior producers like Perpetua Resources (PPTA), which doubled in 2025 according to the Crescat analysis, exemplify the sector's potential for high-risk, high-reward plays.

The current environment mirrors historical inflection points. In 1993–2008, gold miners traded at 3.0x P/NAV as prices surged, a period described in the DiscoveryAlert analysis. A similar re-rating could occur if gold prices remain elevated and investor sentiment shifts. For now, the sector's undervaluation offers a margin of safety, particularly for companies with low debt and high-margin operations.

Conclusion

Gold mining stocks are at a critical juncture. While gold prices have reached record highs, the sector's valuation metrics remain depressed, creating a unique opportunity for investors willing to capitalize on market dislocation. By focusing on companies with strong fundamentals and a history of operational excellence, investors can position themselves to benefit from both the ongoing gold rally and a potential sector-wide re-rating. As history shows, the most rewarding investments often emerge when markets fail to price in long-term value.

Comentarios

Aún no hay comentarios