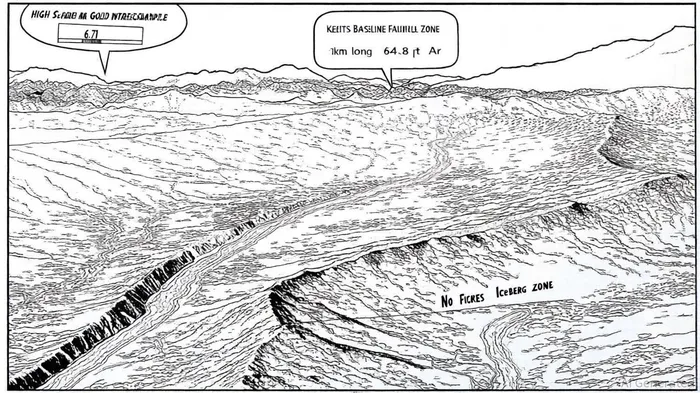

New Found Gold's High-Grade Surface Core Discovery: A Strategic Catalyst for Undervalued Exploration

New Found Gold Corp. (NFGC) has emerged as a compelling case study in the intersection of high-grade mineralization and undervalued exploration potential. Recent channel sampling at the Iceberg zone of its Queensway Gold Project in Newfoundland has confirmed a robust, near-surface gold system with grades that defy conventional expectations for early-stage juniors. The discovery of intervals such as 64.8 g/t Au over 6.71 meters and 113 g/t Au over 2.99 meters[1] underscores the continuity of mineralization across 185 meters of exposure, positioning Iceberg as a critical catalyst for the company's Preliminary Economic Assessment (PEA) and broader resource expansion[2].

Strategic Catalysts: High-Grade Continuity and Geological Potential

The Iceberg zone, part of the Keats Baseline Fault Zone (KBFZ), demonstrates exceptional geological promise. The KBFZ's 2 km strike length and the presence of quartz veining with consistent gold distribution[3] suggest a district-scale system. Notably, the recent 47 g/t Au over 10.55 meters at Iceberg East[4] has extended the high-grade segment to 570 meters of strike, with mineralization remaining open at depth. This depth potential, combined with limited drilling below 200 meters, creates a compelling case for resource growth.

Metallurgical testing further strengthens the narrative. A 96.9% weighted average gold extraction rate from Iceberg and Iceberg East[5] indicates that the mineralization is amenable to gravity separation and carbon-in-leach (CIL) technologies. Such recoveries are rare for polymetallic systems and could significantly reduce processing costs, enhancing the project's economic viability.

Valuation Discrepancy: High P/B vs. Industry Benchmarks

Despite these strengths, NFGC trades at a price-to-book (P/B) ratio of 7.4x[6], far exceeding the Canadian Metals and Mining industry average of 2.3x[7]. This premium appears disconnected from the company's financials, which include a $32.62 million net loss and negative earnings per share of -$0.17[8]. However, this disconnect may reflect market anticipation of resource upgrades and the conversion of inferred resources to indicated categories by late 2025[9].

Analysts have assigned a $5.00 price target (133.65% upside from the current $1.80 level)[10], driven by the PEA's focus on Phase I custom milling and the potential for near-term production. The company's $49.46 million cash position[11] also provides flexibility for exploration without immediate dilution risks, unlike peers reliant on equity financing.

Risks and Mitigants

Critics, including Iceberg Research, have raised concerns about sampling methodologies and the lack of formal resource estimates[12]. However, the alignment of high-grade intercepts with the KBFZ's structural model[13] and the metallurgical validation[14] provide third-party credibility. Additionally, the 70,000-meter drill program[15] aims to address these gaps, with results likely to refine resource classifications and attract institutional interest.

Conclusion: A Mispriced Exploration Play

New Found Gold's Iceberg discovery represents a rare combination of high-grade surface mineralization, scalable infrastructure potential, and favorable metallurgy. While the stock's valuation metrics appear stretched, the company's strategic focus on resource delineation and the PEA's near-term timeline justify the premium. For investors seeking undervalued exploration plays with clear catalysts, NFGC offers a compelling risk-reward profile—provided the company can navigate short-term financial pressures and deliver on its geological promise.

Comentarios

Aún no hay comentarios