Gold's Golden Age: Strategic Entry Points for Long-Term Investors in a Record-Breaking Market

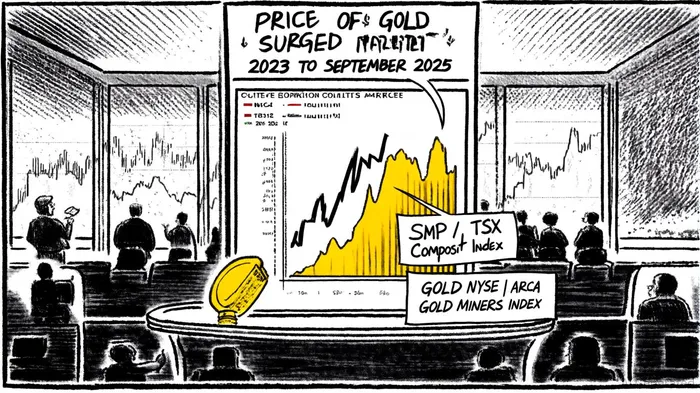

The gold market in 2025 is experiencing a confluence of forces that have propelled the metal to record prices and supercharged the performance of mining equities. By September 2025, gold had surged past $3,847 per ounce, a psychological milestone driven by central bank accumulation, a weakening U.S. dollar, and geopolitical tailwinds, according to JM Bullion's recap. The S&P/TSX Composite Index, buoyed by the materials sector, reached an all-time high of 30,023, with gold miners like Barrick (ABX) and Kinross (K) delivering gains of 80% and 139%, respectively, according to a FinancialContent report. For long-term investors, this presents a critical inflection point: How to navigate a sector at historic highs while balancing risk and reward?

Market Drivers: Central Banks, Geopolitics, and the Dollar

Gold's ascent in 2025 is underpinned by structural shifts. Central banks added 244 tonnes of gold in Q1 2025 alone, with countries like China and Poland diversifying reserves away from the U.S. dollar, according to a Gainesville analysis. This trend, part of a broader de-dollarization push, has created a self-reinforcing cycle: weaker dollar demand boosts gold's appeal, while geopolitical tensions-ranging from Middle East conflicts to U.S. tariff policies-further amplify safe-haven demand, as noted in a Kiplinger post-mortem. Meanwhile, the market anticipates aggressive rate cuts from the Federal Reserve and Bank of Canada, which historically drive gold higher by reducing the opportunity cost of non-yielding assets, as discussed in a Gold Standard piece.

Sector Fundamentals: Peak Production and Rising Costs

Despite gold's price euphoria, the sector faces headwinds. Global gold production is projected to peak at 3,250 tonnes in 2025 before declining 17% by 2030, driven by depleting ore grades and deeper, more costly extraction, according to the Farmonaut mining cost curve. The average cost to mine gold in 2025 ranges between $900–$1,400 per ounce, with energy prices and regulatory compliance inflating All-In Sustaining Costs (AISC) for major producers, per an InvestingNews report. However, technological innovations-such as AI-driven exploration and automation-are mitigating some of these pressures, particularly for mid-tier players like Equinox GoldEQX-- (EQX), which reported 13% higher mill grades in Q3 2025, according to a Sprott insight.

Valuation Metrics: Mining Equities vs. Physical Gold

For investors, the debate between physical gold and mining stocks hinges on leverage and valuation. While gold itself trades at a record $3,850/oz, mining equities have outperformed, with the NYSE Arca Gold Miners Index surging 50% year-to-date versus gold's 25% gain, per the Alchemy Markets outlook. This outperformance reflects the sector's ability to amplify gold's price action through operational efficiency and margin expansion. For example, Kinross Gold reported record free cash flow in Q3 2025, driven by higher throughput at its Fort Knox and Paracatu mines, according to a Yahoo Finance story.

Valuation frameworks must account for key metrics:

- Price-to-Earnings (P/E) Ratios: A low P/E (e.g., Newmont CorporationNEM-- at 12x) suggests undervaluation relative to earnings, while a high P/E (e.g., junior miners at 30x+) reflects speculative growth bets, according to the P/E rankings.

- AISC Trends: Producers with declining AISC, like Gold FieldsGFI-- (-6.5% in Q1 2025), are better positioned to sustain margins as gold prices consolidate, per MiningVisuals data.

- Institutional Positioning: ETFs like the VanEck Vectors Gold Miners ETF (GDX) have attracted $12B in inflows in 2025, signaling institutional confidence in the sector's long-term prospects, according to a CruxInvestor analysis.

Strategic Entry Points: Timing and Diversification

Entering the gold sector at record prices requires a nuanced approach. For long-term investors, the focus should be on dollar-cost averaging into high-conviction names and ETFs rather than timing short-term volatility. Here's how to structure a resilient portfolio:

1. Core Holdings: Allocate 50% to low-cost, high-grade producers like Barrick or NewmontNEM--, which offer stability and dividend yields.

2. Satellite Positions: Use 30% for junior miners with strong exploration pipelines (e.g., Equinox Gold's Valentine Mine) or royalty companies like Franco-Nevada, which benefit from gold's price action without operational risks, as outlined in a Farmonaut guide.

3. Hedging: Deploy 20% in gold ETFs (e.g., SPDR Gold Shares at 0.11% fees) to balance equity risk while maintaining exposure to the metal's safe-haven appeal, following a risk framework.

Timing remains critical. Gold's technical setup-a consolidation pattern above $3,300/oz-suggests a potential breakout in Q4 2025, driven by central bank demand and U.S. election-year uncertainty, according to an Inproved guide. Investors should also monitor macro signals: a sharper-than-expected slowdown in Chinese industrial demand or a Fed pivot delay could trigger short-term corrections.

Risk Mitigation: ESG and Regulatory Vigilance

The gold sector's environmental footprint-20 tons of waste per wedding ring, mercury contamination, and deforestation-remains a wildcard. Companies with robust ESG frameworks, such as Agnico Eagle MinesAEM-- (AEM), are better insulated from regulatory penalties and reputational damage, as detailed in a Yahoo Finance report. Additionally, geopolitical risks, such as Tanzania's 20% domestic gold allocation mandate, highlight the need for geographic diversification, per a Colitco analysis.

Conclusion: A Golden Opportunity, But Not Without Caution

Gold's 2025 rally is a masterclass in macroeconomic tailwinds: inflation hedging, dollar weakness, and central bank demand. For long-term investors, the TSX's mining sector offers a compelling vehicle to capitalize on this momentum, provided entry points are carefully structured. While record prices warrant caution, the sector's structural challenges (declining production, rising costs) and technological innovations create a unique inflection point. As always, diversification, ESG due diligence, and a focus on operational efficiency will separate prudent investors from speculative casualties.

Comentarios

Aún no hay comentarios