Globe Life (GL): Assessing the Recent Share Price Dip as a Potential Value Play

In the volatile landscape of 2025, Globe LifeGL-- (GL) has emerged as a compelling case study for value investors. The recent 4% weekly decline in its share price, while unsettling in the short term, may mask a deeper narrative of earnings resilience and strategic positioning in a high-interest-rate environment. For investors attuned to the principles of value investing-focusing on undervalued fundamentals and long-term growth-GL's current trajectory warrants closer scrutiny.

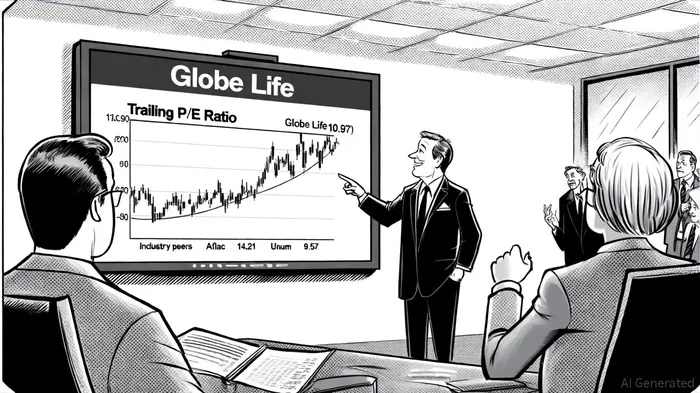

Valuation Metrics: A Discounted Premium

Globe Life's valuation metrics paint a picture of a company trading at a discount relative to its peers, despite maintaining a "GREAT" Financial Health Score of 3.1 out of 4. Its trailing price-to-earnings (P/E) ratio of 10.97 and forward P/E of 8.99 are notably lower than Aflac's 14.21 and Unum Group's 9.57, according to StockAnalysis statistics. This suggests that the market is pricing GL's earnings growth more conservatively, potentially creating a margin of safety for value-oriented investors. Additionally, its price-to-book (P/B) ratio of 2.06 and debt-to-equity ratio of 0.59 indicate a balance sheet that is both robust and moderately leveraged, offering stability in uncertain markets, per StockAnalysis.

The company's operational efficiency further strengthens its case. A return on equity (ROE) of 20.02% and a free cash flow yield of 12.10% underscore its ability to generate returns even as interest rates remain elevated, as shown by StockAnalysis. These metrics are critical in a sector where high rates typically compress bond yields but also reduce discounting pressures on insurance liabilities-a dynamic in which GLGL-- appears to be thriving.

Earnings Resilience in a High-Rate Environment

GL's Q2 2025 earnings report, while mixed, revealed a company adept at navigating macroeconomic headwinds. Despite a 19% decline in excess investment income and significant unrealized losses in its fixed maturity portfolio, the firm exceeded EPS estimates by $0.02, reporting $3.27 per share, according to a Panabee article. This resilience was driven by strategic capital management, including $226 million in share repurchases that reduced diluted shares by 9.5% year-over-year, as noted in the Panabee article. Such actions not only bolster earnings per share but also signal management's confidence in the stock's intrinsic value.

The life insurance segment, a cornerstone of GL's business, delivered a 6% increase in underwriting margin to $340 million, supported by 3% premium growth and disciplined policy obligations, according to the Panabee article. Meanwhile, the health segment, though facing a 2% margin contraction, saw an 8% rise in premiums, reflecting its ability to adapt to shifting demand, as the Panabee article outlines. These results highlight GL's dual strength: a diversified revenue base and operational flexibility to adjust to sector-specific challenges.

The Share Price Dip: Opportunity or Overreaction?

The recent 4% weekly decline in GL's stock price, while concerning, appears to be an overreaction to broader market jitters rather than a reflection of deteriorating fundamentals. Over the past year, GL has delivered a 34% total shareholder return, outperforming many peers in the insurance sector, according to StockAnalysis. Analysts remain cautiously optimistic, with a "Moderate Buy" consensus rating and an average price target of $152.45-implying an 8.58% upside from current levels, per a MarketBeat forecast.

Some projections, however, suggest a more bearish outlook, with forecasts for an average 2025 price of $69.80, per a StockScan forecast. This wide dispersion in analyst expectations underscores the stock's volatility but also highlights its potential for asymmetric returns. For value investors, the current price of $124.81 represents a compelling entry point, especially given the $161.55 fair value estimate cited by some analysts on StockAnalysis.

Strategic Strengths and Long-Term Prospects

GL's long-term appeal lies in its strategic focus on agent growth and direct-to-consumer innovation. The latter, which showed its first positive sales trend in 16 quarters during Q2 2025, signals a pivot toward digital channels that could drive sustainable growth, according to StockAnalysis. Coupled with a strong dividend history and a capital return strategy that prioritizes shareholder value, GL's playbook aligns closely with the tenets of value investing.

Conclusion: A Calculated Bet for Value Investors

While the recent share price dip may test the patience of short-term traders, it presents a calculated opportunity for value investors. GL's undervalued metrics, earnings resilience, and strategic agility position it as a potential winner in a high-interest-rate environment. Risks remain, particularly in the health segment and investment portfolio, but these are outweighed by the company's operational discipline and long-term growth trajectory. For those willing to look beyond near-term volatility, Globe Life offers a compelling case for a value-driven investment.

StockAnalysis statisticsPanabee articleMarketBeat forecastStockScan forecast

Comentarios

Aún no hay comentarios