The Global Semiconductor Arms Race: Strategic Investments and Ecosystem Control in 2025

The semiconductor industry has become the epicenter of global technological and geopolitical competition. As nations and corporations vie for dominance in this critical sector, cross-industry investments are reshaping the landscape of long-term competitive positioning and ecosystem control. From China's state-led push for self-sufficiency to the U.S. and its allies reinforcing domestic manufacturing, the stakes have never been higher.

China's State-Backed Push for Localization

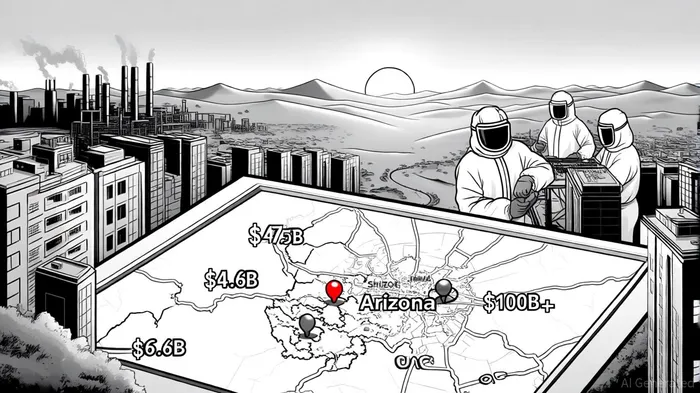

China's third state-backed semiconductor investment fund, valued at $47.5 billion, underscores its determination to localize production and mitigate U.S. export controls[2]. This fund, part of a decade-long strategy initiated in 2014, targets chip manufacturing equipment and supports industry giants like Semiconductor Manufacturing International Corporation (SMIC). By 2025, Beijing aims to reduce its reliance on foreign technologies, a goal accelerated by tightening U.S. restrictions. However, challenges remain: SMIC's 7-nanometer nodes still lag behind TSMC's cutting-edge capabilities, and geopolitical tensions may delay access to advanced tools like EUV lithography.

U.S. and Allies: Reinforcing Domestic Manufacturing

The U.S. and its allies are countering China's ambitions through the CHIPS Act, which allocated $6.6 billion in 2024 to support TSMC's advanced chip production in Arizona[2]. This move not only bolsters domestic manufacturing but also secures a critical ally in global semiconductor leadership. Yet, TSMC's recent suspension of shipments to Chinese firm Sophgo over U.S. export control concerns highlights the fragility of navigating geopolitical fault lines[2]. For the U.S., the challenge lies in balancing strategic partnerships with enforcing export restrictions, a task complicated by the interconnected nature of global supply chains.

Emerging Players: The UAE's Strategic Gambit

While China and the U.S. dominate headlines, the United Arab Emirates is positioning itself as a pivotal player. Reports indicate that TSMCTSM-- and Samsung are considering $100 billion+ investments in large-scale chip fabrication facilities in the UAE[2]. This shift reflects the UAE's strategic advantages: geopolitical neutrality, tax incentives, and proximity to Asian and European markets. If realized, these projects could diversify the global supply chain and reduce reliance on traditional hubs like Taiwan and South Korea.

Market Dynamics: AI-Driven Growth and Structural Shifts

The semiconductor market is projected to reach $697 billion in 2025, driven by insatiable demand for generative AI chips[1]. These chips, which accounted for over 20% of total sales in 2024, are expected to form a $150 billion market by 2025[1]. This surge is reshaping competitive dynamics: companies that secure AI chip production and design capabilities—such as NVIDIANVDA--, AMDAMD--, and TSMC—are gaining disproportionate influence over the ecosystem. Meanwhile, traditional players like IntelINTC-- face headwinds, exemplified by its two-year delay in advanced packaging projects in Poland and Germany[2].

Strategic Implications and Risks

The race for semiconductor dominance is less about short-term gains and more about securing long-term ecosystem control. China's state-led model risks overcapacity and inefficiency but could achieve critical mass in mid-tier chips. The U.S. and allies, meanwhile, must address bottlenecks in domestic manufacturing and R&D funding. For investors, the key lies in identifying firms that can navigate geopolitical risks while capitalizing on AI-driven demand.

However, challenges persist. Intel's restructuring highlights the financial pressures of maintaining advanced manufacturing capabilities. Similarly, the UAE's ambitions hinge on attracting and retaining top talent—a hurdle in a sector dominated by Asian and North American expertise.

Conclusion

The semiconductor industry is no longer just about silicon; it is a battleground for technological sovereignty and economic influence. As cross-industry investments redefine the ecosystem, the winners will be those who align strategic vision with operational agility. For investors, the path forward requires a nuanced understanding of geopolitical currents, technological trends, and the structural shifts reshaping this vital sector.

Comentarios

Aún no hay comentarios