Global Market Euphoria in Late 2025: A Sustainable Bull Market or a Looming Correction?

The global markets in late 2025 are perched on a knife's edge. Optimism, fueled by AI-driven growth narratives and central bank easing, has propelled valuations to levels not seen since the dot-com era. Yet beneath the surface, cracks in the foundation-soaring CAPE ratios, uneven economic growth, and geopolitical tail risks-hint at a precarious balance. This analysis examines whether the current euphoria signals a durable bull market or a replay of history's most infamous overvaluations.

Historical Parallels: When Euphoria Met Reality

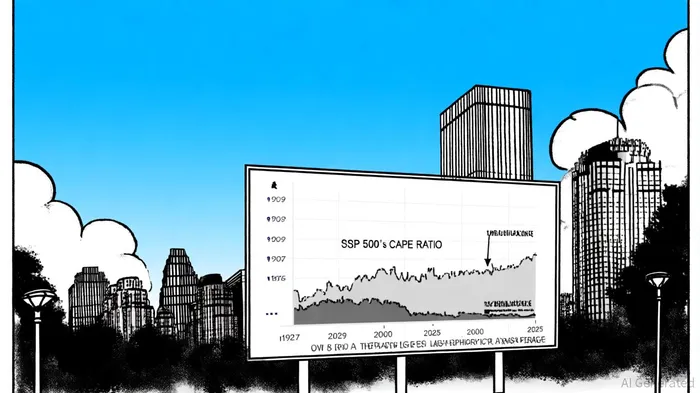

The S&P 500's cyclically adjusted price-to-earnings (CAPE) ratio hit 40x in Q3 2025, far exceeding its long-term average of 16.8 [1]. This metric, a bellwether for overvaluation, mirrors the peaks of 1929 (32.7x) and 2000 (44.2x) [2]. While elevated CAPE ratios do not guarantee collapse, they correlate with prolonged corrections. For instance, the dot-com bubble's 44.2x peak was followed by a 40% decline in the S&P 500 over two years [2]. Similarly, the 2008 crisis, though marked by a lower CAPE of 27.6x, still triggered a 38.5% drop in equities [2].

The 2020–2021 market euphoria offers a more direct comparison. By June 2024, the CAPE ratio reached 35.49, with trailing P/E at 28.64-levels last seen during the 2000 crash [3]. Yet the market avoided a severe correction, buoyed by unprecedented fiscal stimulus and accommodative monetary policy. This raises a critical question: Can the 2025 bull market sustain itself without similar tailwinds?

Macroeconomic Headwinds and Tailwinds

The global economy in Q3 2025 is a patchwork of contradictions. Real GDP growth is forecast at 2.42%, driven by U.S. pre-tariff spending and fiscal stimulus [4]. However, inflation remains stubbornly high at 5.43%, with the Americas and Asia-Pacific seeing upticks [4]. Central banks, including the European Central Bank (ECB), have responded aggressively, with the ECB cutting rates eight times in 2025 to 2.15% [4]. These cuts have eased financial conditions, but they also amplify the risk of asset bubbles.

The U.S. Federal Reserve's rate-cutting cycle, while supportive of equities, has created a "Goldilocks" scenario: low rates boost valuations but also mask underlying vulnerabilities. For example, business and consumer sentiment in the G7 and EU have faltered due to U.S. tariff uncertainty [4]. Meanwhile, the WTO's revised trade growth forecast of 0.9% for 2025-driven by pre-tariff imports-hints at a slowdown in 2026 [4].

Asset Class Valuations: A Tale of Two Markets

Equities: The S&P 500's trailing P/E of 28.3x and forward P/E of 22.6x (Q3 2025) suggest overvaluation, particularly in growth sectors [5]. While AI optimism and strong earnings have justified some premium, the disconnect between valuations and fundamentals is stark. For instance, tech stocks trade at multiples implying perpetual earnings growth-a scenario historically reserved for speculative bubbles.

Bonds: Fixed income markets offer a counterpoint. High-yield bond yields above 7% and a steepening U.S. yield curve suggest value, especially as inflation moderates [6]. However, sector-specific risks-such as exposure to tariff-impacted industries-remain.

Real Estate: The real estate market is polarized. Industrial and data center REITs have thrived, with FFO growth of 21.3% and 8.0%, respectively [7]. Conversely, office and hotel REITs struggle, with office REITs posting -5.5% FFO growth [7]. This divergence reflects structural shifts in demand, not just cyclical factors.

Commodities: Gold and silver benefit from inflation hedging and geopolitical tensions, while copper faces headwinds from short-term supply distortions [8]. Energy markets, particularly WTI crude, hinge on a fragile technical setup, with $55.23 a critical support level [8].

Strategic Implications: Caution in Overvalued Sectors

The current euphoria shares DNA with past bubbles but differs in key ways. Unlike 2000 or 2008, the 2025 bull market is underpinned by genuine technological progress and resilient corporate earnings. However, valuations imply perfection: perpetual AI-driven growth, no trade war escalation, and no inflation resurgence. History suggests such assumptions are dangerous.

Recommendations:

1. Equities: Prioritize quality over growth. Focus on sectors with durable cash flows (e.g., healthcare, utilities) and avoid speculative tech plays.

2. Bonds: Allocate to high-yield and international bonds, which offer better risk-adjusted returns amid easing inflation.

3. Real Estate: Favor industrial and data center REITs while avoiding overleveraged office assets.

4. Commodities: Use gold and silver as hedges but avoid overexposure to cyclical metals like copper.

Conclusion

The 2025 bull market is a product of both innovation and complacency. While AI and rate cuts provide tailwinds, valuations suggest a market pricing in utopian outcomes. Investors must balance optimism with pragmatism, hedging against the inevitable mean reversion. As the adage goes, "Bubbles don't pop-they deflate." The question is not if the euphoria will end, but when and how prepared investors will be.

Comentarios

Aún no hay comentarios