Glaukos' Q3 2025 Earnings: A Deep Dive into Growth, Market Dominance, and Strategic Resilience

Glaukos' Q3 2025 Earnings: A Deep Dive into Growth, Market Dominance, and Strategic Resilience

Glaukos Corporation (NYSE: GKOS) has long been a bellwether in the ophthalmic medical device sector, and its third-quarter 2025 earnings release offers a compelling case study in navigating a competitive landscape while maintaining robust growth. With total revenue for the quarter reaching $96.67 million-a 23.9% year-over-year increase-the company continues to solidify its leadership in micro-invasive glaucoma surgery (MIGS) while addressing systemic challenges in reimbursement and market diversification, according to a Yahoo Finance report. This analysis evaluates Glaukos' financial performance, market positioning, and strategic initiatives to determine its trajectory in a rapidly evolving industry.

Financial Performance: Sustained Growth Amid Strategic Rebalancing

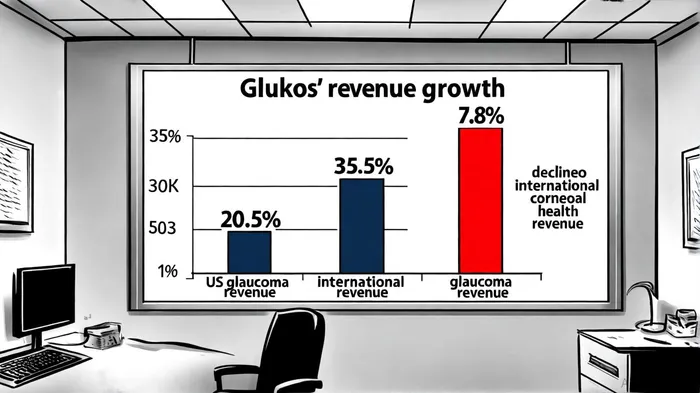

Glaukos' Q3 2025 results underscore its ability to scale revenue while refining its business model. U.S. glaucoma sales surged 35.5% year-over-year to $51.57 million, driven by the adoption of its iDose TR implant, a first-of-its-kind sustained drug-delivery system for glaucoma management, as reported by the Yahoo Finance report. International glaucoma revenue also rose 20.7% to $24.47 million, reflecting the global appeal of its MIGS portfolio. However, the company faced headwinds in its corneal health segment, where international revenue declined 7.8% to $2.19 million, highlighting the need for diversification noted in the Yahoo Finance report.

These results align with Glaukos' broader financial strength. For full-year 2025, the company raised its revenue guidance to $480–486 million, a range that mirrors the $480.8 million consensus estimate, according to MarketBeat. This confidence stems from a $278.6 million cash reserve with no debt, providing flexibility for R&D and market expansion, as detailed in a Panabee report. While Q3 gross margins remain undisclosed, Q2 figures showed an improvement to 78%, up from 76% in 2024, suggesting operational efficiency is keeping pace with growth (Panabee).

Market Positioning: Dominance in MIGS, but Competition Intensifies

Glaukos' dominance in the MIGS segment is unparalleled, with a 65% global market share as of 2025, according to a SWOTAnalysis profile. Its flagship products, including the iStent infinite and iPrime, have been validated in over 300 clinical studies, cementing their reputation for safety and efficacy (SWOTAnalysis). However, this leadership faces mounting pressure. Established players like Alcon (a Novartis subsidiary) and Johnson & Johnson Vision are investing heavily in competitive MIGS platforms, leveraging their broader portfolios and global distribution networks (SWOTAnalysis).

The company's reliance on glaucoma-accounting for 85% of its revenue-remains a vulnerability. To mitigate this, GlaukosGKOS-- is expanding into adjacent markets such as corneal health and retinal disease therapies. For instance, its EpiOXA corneal cross-linking system and iDose TREX (an advanced drug-delivery platform) are positioned to unlock a $15 billion total addressable market (SWOTAnalysis). This diversification is critical, as inconsistent global reimbursement policies and LCD restrictions (e.g., limits on using two MIGS devices per procedure) threaten patient access and revenue stability, as discussed in a Nasdaq article.

Strategic Initiatives: Innovation, Expansion, and Reimbursement Advocacy

Glaukos' 2025 strategic plan emphasizes three pillars: innovation in next-gen MIGS platforms, international expansion, and reimbursement reform. The company is advancing T-REX and TRIO, next-generation MIGS devices designed to enhance surgical outcomes, while scaling production of its iDose TR implant, which generated $31 million in Q2 2025 revenue (Panabee). R&D spending increased 6% year-over-year to $32.4 million in Q2, reflecting a measured approach to innovation while prioritizing commercialization (Panabee).

Internationally, Glaukos is targeting $2 billion in untapped opportunities in Europe and Asia, where MIGS adoption remains nascent (SWOTAnalysis). This expansion is supported by infrastructure investments and a focus on surgeon training, which differentiates Glaukos from competitors relying on traditional sales models (MarketBeat).

Reimbursement challenges, however, persist. While iDose TR has secured coverage through key Medicare Administrative Contractors (MACs) like Noridian and Novitas, broader parity remains elusive. The company is actively advocating for policy changes to remove LCD barriers, a critical step in ensuring long-term profitability (Nasdaq).

Challenges and Opportunities: A Balanced Outlook

Despite its strengths, Glaukos faces structural challenges. The MIGS market is becoming increasingly crowded, with Alcon's Xen Gel Stent and Johnson & Johnson's iStent Supra offering direct competition. Additionally, the company's underperformance in legacy stent sales-notably in cataract + MIGS procedures-highlights the risks of relying on a single therapeutic area (Nasdaq).

Yet, Glaukos' long-term prospects remain bright. Its dual growth engines-MIGS and sustained drug delivery-are well-positioned to capitalize on the $15 billion ophthalmic market (Nasdaq). Moreover, its focus on AI-powered surgical guidance systems and manufacturing automation (aiming to reduce unit costs by 25% through automation (SWOTAnalysis)) positions it to scale profitably.

Conclusion: A Leader Navigating Complexity

Glaukos' Q3 2025 earnings affirm its status as a pioneer in interventional glaucoma, with revenue growth outpacing industry benchmarks. However, the company's future depends on executing its diversification strategy and overcoming reimbursement hurdles. For investors, the key takeaway is clear: Glaukos' innovation pipeline and global expansion efforts provide a strong foundation for sustained growth, but vigilance around competitive dynamics and regulatory headwinds is essential.

As the ophthalmic device sector evolves, Glaukos' ability to balance R&D investment with commercial execution will determine whether it maintains its 65% MIGS market share or cedes ground to rivals. For now, the numbers suggest the former is more likely.

Comentarios

Aún no hay comentarios