Glanbia (ISE:GL9): A Compelling Undervalued Opportunity in the Global Nutrition and Performance Ingredients Sector

The global nutrition and performance ingredients sector is undergoing a transformative phase, driven by surging demand for functional foods, sports nutrition, and personalized health solutions. Amid this backdrop, Glanbia (ISE:GL9) emerges as a compelling case study in undervaluation, offering investors a unique opportunity to capitalize on its robust cash flows, forward-looking earnings potential, and strategic positioning in a high-growth market.

Financial Performance: Mixed Results with Strong Underlying Fundamentals

Glanbia's first-half 2025 results reflect a challenging operating environment. Revenue rose 6.1% year-over-year to $1.93 billion, demonstrating resilience in core markets, according to Simply Wall St. However, net income contracted by 31% to $99.4 million, with profit margins declining to 5.2% from 7.9% in 2024 - a deterioration the Simply Wall St analysis attributed largely to inflationary pressures and supply chain disruptions, which are expected to moderate in the coming quarters.

Despite these near-term headwinds, Glanbia's financial health remains robust. The company generated $307.94 million in operating cash flow and $266.95 million in free cash flow over the past 12 months, according to StockAnalysis, underscoring its ability to fund operations, reinvest in growth, and reward shareholders. These metrics position Glanbia as a defensive play in an otherwise volatile sector.

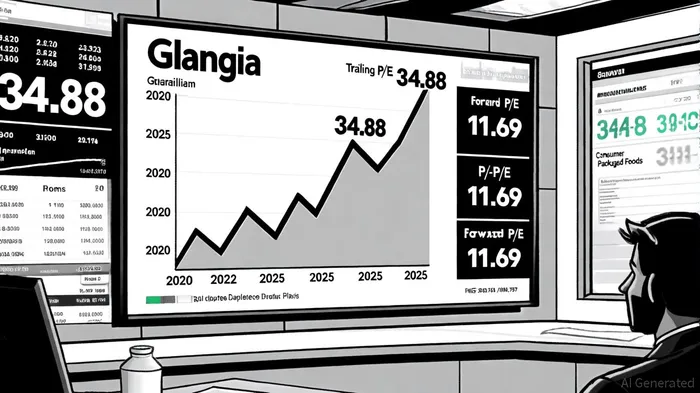

Valuation Metrics: A Tale of Two P/E Ratios

Glanbia's valuation appears paradoxical at first glance. Its trailing price-to-earnings (P/E) ratio of 34.88 is significantly elevated compared to its 10-year average of 17.82 (as reported by StockAnalysis). However, the forward P/E ratio of 11.69-a measure of future earnings expectations-suggests that the market is pricing in substantial growth. This divergence is not uncommon for companies in transition, particularly those navigating macroeconomic challenges while laying the groundwork for long-term expansion.

When benchmarked against industry peers, Glanbia's valuation becomes even more compelling. Proxies such as the Consumer Staples sector (P/E of 24.12 as of October 2025, per Siblis Research) and the Packaged Foods industry (P/E of 18.32, per the Simply Wall St analysis) provide context. Glanbia's trailing P/E of 34.88 exceeds these benchmarks, but its forward P/E of 11.69 is well below, indicating that analysts anticipate a meaningful rebound in earnings. This optimism is supported by consensus forecasts projecting 22.9% annual earnings growth and 2.7% revenue expansion over the next three years, according to Simply Wall St.

Sector Dynamics and Growth Catalysts

The global nutrition and performance ingredients market is forecasted to grow from $482.69 billion in 2025 to $1.11 trillion by 2033, according to Business Research Insights, driven by trends such as the rise of plant-based proteins, demand for clean-label ingredients, and the mainstreaming of performance nutrition. Glanbia's dual focus on Performance Nutrition (13.4% EBITDA margin) and Health & Nutrition (18.5% EBITDA margin) aligns it with these megatrends, per Glanbia analyst coverage.

Moreover, the company's recent strategic investments in R&D and capacity expansion are poised to unlock value. For instance, its $200 million investment in a new European production facility for whey protein isolate-a key ingredient in sports nutrition-is expected to enhance margins and secure long-term supply chain stability, according to the Simply Wall St analysis.

Risks and Mitigants

Investors should remain cognizant of macroeconomic risks, including interest rate volatility and potential regulatory shifts in the food and supplement industries. However, Glanbia's strong balance sheet, with a debt-to-equity ratio of 0.45 (per StockAnalysis), and its history of disciplined capital allocation provide a buffer against these uncertainties. Additionally, the company's diversified geographic footprint-spanning North America, Europe, and Asia-reduces exposure to regional economic shocks.

Conclusion: A Strategic Buy for Long-Term Investors

Glanbia's current valuation appears to discount its long-term potential more than its near-term challenges. While the trailing P/E ratio may seem high, the forward-looking metrics, coupled with analyst projections of 15.1% return on equity (ROE) over the next three years reported by Simply Wall St, suggest that the stock is undervalued relative to its growth trajectory. For investors with a 3–5 year horizon, Glanbia offers an attractive entry point into a sector poised for sustained expansion.

Comentarios

Aún no hay comentarios