Givaudan's Sales Performance and Strategic Resilience: Assessing Long-Term Investor Confidence Amid Stable Guidance and Sector Headwinds

Givaudan's Q3 2025 results underscore its ability to thrive amid macroeconomic turbulence, delivering 14.1% organic sales growth (OSG)-a figure that significantly outperformed market expectations, according to Givaudan's half-year results. Total reported sales reached CHF 1,907 million, a 10.2% year-over-year increase, driven by a 12.1% volume surge and a 2% pricing boost. While foreign exchange headwinds reduced the growth rate by approximately 5%, the company's performance highlights its operational agility and pricing discipline. This resilience is further reflected in its divisional breakdown: the Fragrance & Beauty segment achieved 16.0% OSG, while Taste & Wellbeing grew by 12.4%.

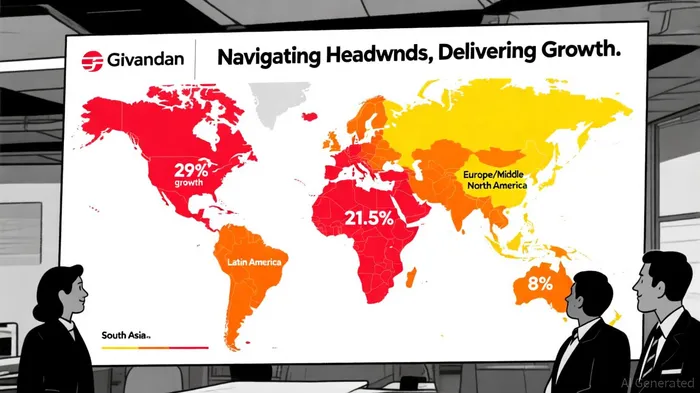

Regional disparities reveal a nuanced picture. South Asia, the Middle East, and Africa led the charge with a staggering 29% OSG, nearly doubling the 12.5% growth recorded in the first half of 2025, as reported by The Financial Analyst. Latin America followed closely with 21.5% growth, whereas Europe and North America posted more modest gains of 8% and 6%, respectively, per Givaudan's half-year results. These figures suggest that Givaudan's geographic diversification is paying dividends, particularly in high-growth emerging markets.

Financially, the company maintained a robust margin profile. For the first half of 2025, EBITDA reached CHF 973 million, with a margin of 25.2%, and net income totaled CHF 592 million, according to Givaudan's market environment and trends. Despite a temporary dip in free cash flow to -0.4% of sales-attributed to timing effects in investments and tax payments-Givaudan reaffirmed its 2025 guidance: 4–5% like-for-like sales growth and free cash flow exceeding 12% of sales, as disclosed in the half-year results. This stability, even amid rising input costs and global trade tariffs, signals strong capital management and strategic foresight.

However, sector-specific challenges persist. Global trade tariffs and inflationary pressures have forced Givaudan to collaborate with customers on strategic price increases to offset rising input costs, a dynamic noted by The Financial Analyst. Meanwhile, the climate crisis and shifting consumer demand for sustainable products necessitate ongoing innovation in supply chain transparency and eco-friendly offerings, as described in Givaudan's market environment and trends. These headwinds, while significant, appear manageable given the company's proactive approach to cost management and R&D investment.

Investor confidence is further bolstered by Givaudan's consistent guidance and financial discipline. Despite a -CHF 16 million free cash flow in the first half of 2025, the company's ability to maintain its EBITDA margin above 25% and its commitment to long-term targets demonstrate resilience, according to a Morningstar report. Analysts note that Givaudan's focus on high-growth markets and its dual-business model (Fragrance & Beauty vs. Taste & Wellbeing) provide a buffer against sector-specific downturns, as reflected in the half-year results.

In conclusion, Givaudan's Q3 performance and strategic adaptability position it as a compelling long-term investment. While global trade tensions and sustainability demands remain risks, the company's pricing power, geographic diversification, and operational efficiency mitigate these concerns. For investors seeking stability in a volatile market, Givaudan's reaffirmed guidance and robust financials offer a compelling case for confidence.

Comentarios

Aún no hay comentarios