Gilead Sciences' Phase 3 ASCENT-03 Study: A Pivotal Moment for Long-Term Growth?

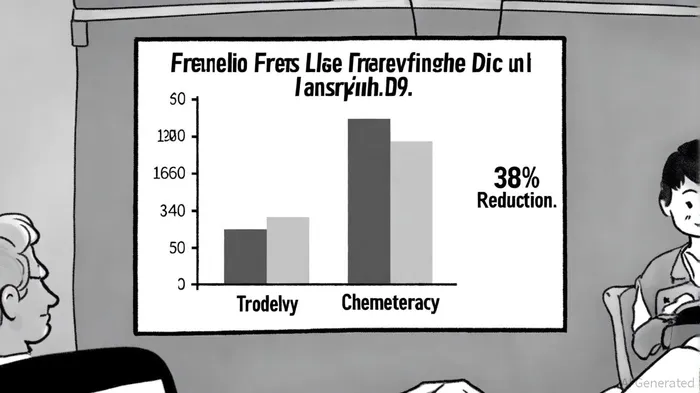

The recent success of GileadGILD-- Sciences' Phase 3 ASCENT-03 study marks a critical inflection point for the company's oncology division. The trial, which evaluated Trodelvy (sacituzumab govitecan-hziy) for first-line treatment of metastatic triple-negative breast cancer (mTNBC), demonstrated a 38% reduction in the risk of disease progression or death compared to chemotherapy (HR: 0.62; p < 0.0001) according to a Gilead press release. With a median progression-free survival (PFS) of 9.7 months for Trodelvy versus 6.9 months for chemotherapy, the results underscore the drug's potential to redefine standards of care in a therapeutic area long starved of innovation. For investors, the question now is whether this clinical milestone translates into durable value creation for Gilead.

Strategic Pipeline Progress: From Clinical Success to Market Expansion

The ASCENT-03 results are not an isolated win but part of a broader strategic pivot by Gilead to solidify its position in oncology. The company's pipeline now includes 30 clinical-stage programs, spanning early-phase trials to late-stage development, with a focus on addressing unmet needs in cancers like mTNBC, according to Gilead Q225 slides. Trodelvy's success in first-line mTNBC-a population previously limited to chemotherapy-opens the door for label expansion and broader market penetration.

According to a Reuters report, Gilead is preparing FDA submissions in H2 2025 to expand Trodelvy's indication, which could unlock new revenue streams. This aligns with the drug's current market performance: in Q2 2025, Trodelvy generated $364 million in sales, maintaining its #1 market share in second-line mTNBC in the U.S. and EU (Gilead Q225 slides). Analysts at Oppenheimer have raised their price target for Gilead to $132.00, citing the "highly statistically significant" ASCENT-03 results and the potential for Trodelvy to become a backbone therapy for all first-line mTNBC patients, regardless of PD-L1 status.

Competitive Positioning: Navigating a Crowded Oncology Landscape

While Trodelvy's clinical profile is compelling, Gilead faces competition from established players and emerging therapies. However, the drug's consistent safety profile-with neutropenia and diarrhea as the most frequent grade ≥3 adverse events-positions it as a viable alternative to PD-1/PD-L1 inhibitors, which are not suitable for all patients (Gilead press release). This differentiation is critical in a market where personalized treatment and treatment accessibility are growing priorities.

Moreover, Gilead's investment in cell therapy programs and collaborations, such as its Gilead Research Scholars Program, signals a long-term commitment to innovation. These initiatives aim to advance epigenetic therapies and digital healthcare tools, further diversifying the company's oncology portfolio (Gilead Q225 slides). Such strategic depth reduces reliance on any single asset and enhances resilience against competitive pressures.

Financial Metrics and Valuation Implications

From a financial perspective, Gilead's balance sheet remains robust. The company's HIV business continues to drive stable cash flows, while oncology advancements like Trodelvy provide growth tailwinds. In Q2 2025, Gilead raised its full-year guidance, reflecting confidence in its pipeline and market execution (Gilead Q225 slides).

The ASCENT-03 results have already spurred a positive stock reaction, with analysts emphasizing the drug's potential to drive $1 billion+ in annual sales if approved for first-line use. This optimism is reflected in the $132.00 price target set by Oppenheimer, a 12% increase from previous estimates (Oppenheimer). For long-term investors, the key metric will be how quickly Gilead can scale Trodelvy's adoption post-approval and whether the drug's label expansion leads to premium pricing in a market where novel therapies command higher margins.

Conclusion: A Pivotal Moment, But Not Without Risks

The ASCENT-03 study represents a pivotal moment for Gilead SciencesGILD--, validating its strategic focus on oncology and demonstrating the transformative potential of Trodelvy. However, the path to sustained growth is not without challenges. Regulatory delays, competitive responses, and pricing pressures could temper the drug's market impact. That said, the clinical data, combined with Gilead's financial strength and pipeline depth, suggest that the company is well-positioned to capitalize on this breakthrough. For investors, the ASCENT-03 results are a compelling catalyst-but patience will be required to fully realize the long-term value.

Comentarios

Aún no hay comentarios