Ghana's Producer Price Inflation and Its Implications for Commodity-Linked Investments

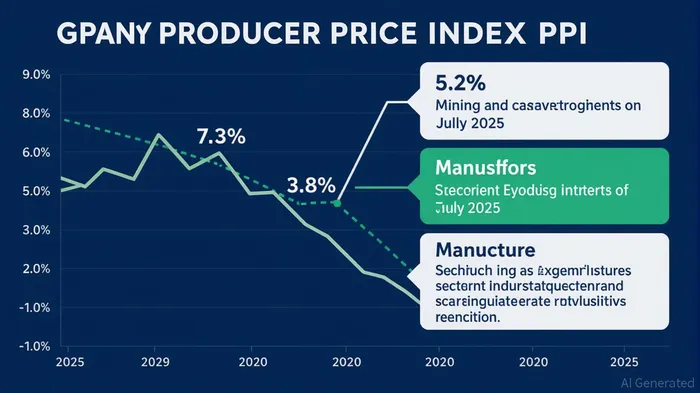

Ghana's economic landscape in 2025 is marked by a significant moderation in producer price inflation, offering both challenges and opportunities for commodity-linked investments. With producer price inflation nosediving to 3.8% in July 2025—the lowest since November 2023—businesses and investors are recalibrating strategies amid easing input costs and a stronger domestic currency[4]. This decline, driven by sharp reductions in the mining and manufacturing sectors, has created a favorable environment for agricultural production and raw material exports, though structural risks remain.

Easing Producer Price Pressures: A Boon for Agriculture

The Ghana Statistical Service (GSS) reported a 2.0 percentage point drop in producer price inflation from June to July 2025, with the mining and quarrying sector alone contributing a 1.9-point reduction[4]. For the agricultural sector, this translates to lower costs for fertilizers, machinery, and energy, which are critical inputs for crop and livestock production. In Q2 2025, agriculture grew by 5.2%, fueled by a 5.9% expansion in the livestock subsector[5]. However, this growth slowed compared to Q1's 6.6%, raising concerns about the sector's long-term resilience[2]. Analysts argue that while lower inflation eases cost burdens, investments in mechanization and infrastructure are essential to sustain productivity gains[2].

The Ghanaian cedi's appreciation of over 30% in 2025 has further reduced import costs for agricultural inputs, indirectly supporting farmers[1]. Yet, this currency strength could also dampen export competitiveness for cash crops like cocoa, which account for $1.09 billion in annual exports[4]. Investors must balance these dynamics, prioritizing sectors where domestic cost advantages outweigh external pressures.

Raw Material Exports: A Mixed Bag of Opportunities

Ghana's export profile remains heavily tilted toward natural resources, with gold, crude oil, and cocoa beans contributing over 70% of total export revenue[2]. While gold exports dipped by 25.3% in 2024 compared to 2023[3], cocoa exports surged by 52.2%, reflecting growing global demand for the commodity. This divergence highlights a strategic opportunity: diversifying export baskets to reduce reliance on volatile sectors like mining.

The manufacturing sector's PPI decline from 7.2% to 3.6% in July 2025[4] suggests improved cost predictability for value-added processing of raw materials. For instance, cocoa processing into chocolate or derivatives could capture higher margins, provided infrastructure gaps are addressed. Similarly, crude oil exports, which shifted from deficit to surplus in 2024[3], present a case for reinvesting in refining capacity to add domestic value.

Risks and the Road Ahead

Despite these positives, Ghana's inflationary trends mask uneven sectoral pressures. While producer prices in agriculture have eased, the services and transport sectors continue to face inflationary headwinds[3]. This disparity complicates investment decisions, as rising logistics costs could offset savings in input prices. Additionally, the real terms of Ghana's exports fell by 16.6% in 2023[2], underscoring the need for policy interventions to enhance competitiveness.

For investors, the key lies in aligning with sectors poised to benefit from both falling costs and structural reforms. Agriculture, particularly livestock and high-value crops, offers immediate upside, while downstream processing of raw materials could yield long-term gains. However, success will depend on navigating currency fluctuations and ensuring that policy frameworks support innovation and infrastructure development[2].

Conclusion

Ghana's moderate producer price inflation in 2025 has created a window of opportunity for commodity-linked investments, particularly in agriculture and value-added exports. Yet, the path forward requires careful navigation of currency risks, sectoral imbalances, and the need for policy continuity. As the Ghanaian cedi stabilizes and input costs ease, investors who prioritize diversification and local value chains may find fertile ground for growth.

Comentarios

Aún no hay comentarios