Getty Copper's Strategic Acquisition and the Future of Junior Copper Explorers

The global copper market is undergoing a seismic shift driven by the energy transition, with demand projected to surge by over 50% by 2035 due to the electrification of transportation, renewable energy infrastructure, and grid modernization[1]. In this context, junior copper explorers like Getty Copper Inc. (TSX-V: GTC) are positioned at a critical juncture—balancing the high-risk, high-reward nature of exploration with the strategic imperative to consolidate assets in politically stable, resource-rich jurisdictions. Getty's recent binding letter of intent (LOI) to acquire 1390120 B.C. Ltd. (Numberco) and its extension of the exclusivity period to October 31, 2025, offers a compelling case study of how junior miners are navigating this volatile landscape.

Strategic Rationale: Consolidation in a High-Grade District

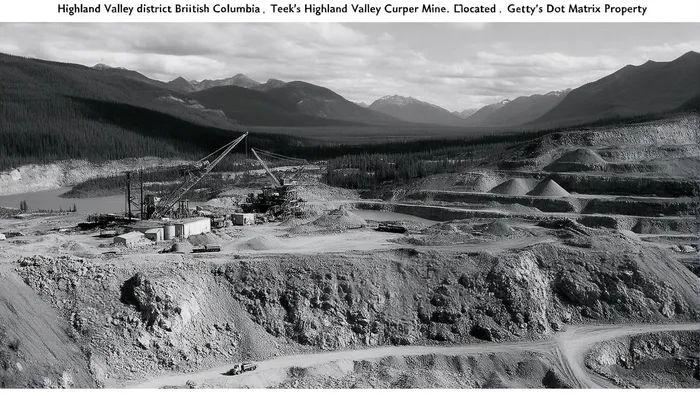

Getty's proposed acquisition of Numberco centers on the 846-hectare Dot Matrix Property, located in the Highland Valley district of British Columbia—a region already home to Teck's Highland Valley Copper Mine, one of Canada's largest copper operations[3]. By consolidating its existing projects with Numberco's land package, Getty aims to create a contiguous landholding that could unlock synergies in exploration, permitting, and infrastructure sharing. The proximity to an established mine reduces exploration risk and operational costs, a critical advantage for a junior explorer with limited capital.

The transaction terms—issuing 13 million common shares and raising $12 million through a concurrent equity financing—reflect a calculated approach to balancing dilution and liquidity[4]. While the 12.3% share issuance may raise eyebrows among risk-averse investors, the $12 million raise is essential for settling existing debt and funding the 2026 exploration season. This aligns with broader industry trends, where junior explorers are increasingly leveraging reverse takeovers and strategic partnerships to fast-track project development[2].

Market Dynamics and Risk Mitigation

Getty's Q2 2025 financial results, though showing a net loss of CAD 0.134 million, represent a marginal improvement over the prior year[3]. This slight uptick, coupled with the extension of the LOI exclusivity period, signals management's confidence in navigating the complex due diligence process. The $500,000 termination fee further underscores the seriousness of the transaction, deterring opportunistic bids while allowing both parties to focus on execution[1].

However, the path to completion is not without hurdles. Regulatory approvals, particularly in British Columbia's stringent mining jurisdiction, and the success of the $12 million financing are critical variables. For junior explorers, the ability to secure capital remains a double-edged sword: while a successful raise could catalyze exploration breakthroughs, over-reliance on equity dilution risks eroding shareholder value. Getty's strategy hinges on demonstrating sufficient geological potential to attract institutional investors—a challenge shared by peers in the space.

Broader Implications for Junior Explorers

Getty's case highlights a broader trend: the survival of junior copper explorers in a rising-demand environment depends on their ability to consolidate assets, secure financing, and align with macroeconomic tailwinds. With copper prices trading near multi-year highs and central banks prioritizing energy transition metals, companies that can de-risk projects through strategic acquisitions and proximity to infrastructure are likely to outperform.

Yet, the sector remains highly fragmented. According to a report by BloombergNEF, over 70% of junior miners lack the balance sheet strength to advance projects beyond the feasibility stage without external partnerships[2]. Getty's reverse takeover model—acquiring a smaller entity with complementary assets—offers a blueprint for overcoming this limitation. By leveraging Numberco's land package and Getty's operational expertise, the combined entity could position itself as a key supplier to Teck and other regional producers, capitalizing on the Highland Valley district's proven geology.

Conclusion: A High-Stakes Bet on the Energy Transition

Getty Copper's LOI represents both a strategic masterstroke and a high-stakes gamble. The acquisition's success will depend on the company's ability to execute the financing, satisfy regulatory requirements, and deliver meaningful exploration results. For investors, the key takeaway is clear: in a world where copper demand is set to outpace supply for the next decade, junior explorers that can de-risk projects through consolidation and proximity to infrastructure will command premium valuations. Getty's journey—fraught with challenges but rich in potential—embodies the resilience required to thrive in this new era of mining.

Comentarios

Aún no hay comentarios