Germany's Weakening Industrial Momentum and the DAX: A Divergent Path Amid Structural Risks to European Equities

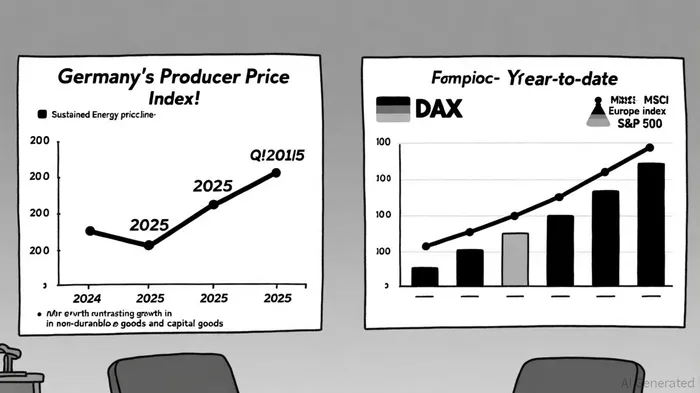

Germany's industrial sector is facing a prolonged slump, with the Producer Price Index (PPI) for industrial products declining by 1.5% year-on-year in Q2 2025, marking six consecutive months of annual declines[1]. This trend, driven by collapsing energy prices (natural gas -11.0%, electricity -10.8%) and weak demand for intermediate goods, signals a structural slowdown in the country's manufacturing base[2]. While non-durable consumer goods and capital goods have posted modest gains (3.3% and 1.8%, respectively), these categories represent a shrinking share of overall industrial activity[3]. The PPI's sustained contraction—a 2.2% year-on-year drop in August 2025—has raised alarms about deflationary pressures and the potential for a broader economic malaise[4].

Yet, the DAX 40, Germany's benchmark equity index, has defied these macroeconomic headwinds. As of September 2025, the index trades near 22,965 points, with a year-to-date return of +27.16%[5]. This divergence between economic fundamentals and equity performance is rooted in the global exposure of DAX constituents. Companies like SAPSAP-- (66% gain in 2024) and Siemens Energy (+106.95% in 2025) derive over 85% of their revenue from international markets, insulating them from domestic stagnation[6]. The index's outperformance—despite Germany's GDP growth remaining negative for six consecutive years—reflects a global rotation into value stocks and the resilience of export-driven sectors like defense (Rheinmetall's +183% surge) and industrial technology[7].

However, this apparent decoupling masks significant structural risks to European equities. Declining producer prices are symptomatic of weak demand, which could force the European Central Bank (ECB) into a dovish policy pivot, exacerbating liquidity-driven equity gains at the expense of real economic recovery[8]. Meanwhile, U.S.-China trade tensions have intensified, with tariffs on European exports rising from 2.5% to 18% in Q2 2025[9]. This has already triggered a 17% decline in the MSCIMSCI-- Europe index since March 2025, as investors priced in higher probabilities of recession and margin compression[10]. For sectors like automotive and apparel—critical to Germany's industrial output—tariff-driven cost inflation and retaliatory measures from China pose existential threats[11].

The ECB's Financial Stability Review underscores these vulnerabilities, noting that European banks' exposure to trade-sensitive sectors amplifies systemic risks[12]. If trade policy uncertainty persists, corporate earnings could face a double squeeze: weaker export demand and higher production costs from energy and raw material bottlenecks. This dynamic is already evident in Germany's energy-intensive industries, where declining PPIs for intermediate goods (-1.0% YoY) signal deteriorating input cost margins[13].

For investors, the DAX's resilience is a double-edged sword. While global demand for German multinational champions offers short-term upside, the index's long-term health depends on resolving structural imbalances. These include energy dependency, demographic decline, and the transition to electric vehicles—a sector where Germany lags its Asian and U.S. counterparts[14]. The ECB's dovish stance and low interest rates may prolong the current bull market, but they cannot offset the drag from weak domestic demand and geopolitical fragmentation[15].

In conclusion, Germany's industrial momentum is weakening, and while the DAX has thrived on global demand, European equities face mounting structural risks. Investors must weigh the short-term allure of multinational champions against the long-term fragility of an export-dependent model in an era of trade wars and deflationary pressures. The coming months will test whether the DAX can sustain its outperformance—or if the cracks in Europe's economic foundation will finally widen.

Comentarios

Aún no hay comentarios