Geopolitical Crosswinds: Navigating Investment Risks and Opportunities in Aerospace and Logistics

The aerospace and logistics sectors in 2025 are navigating a turbulent geopolitical landscape, where shifting trade policies, airspace closures, and regional conflicts are reshaping global air cargo and passenger routes. These disruptions present both risks and opportunities for investors, demanding a nuanced understanding of how companies are adapting to volatility.

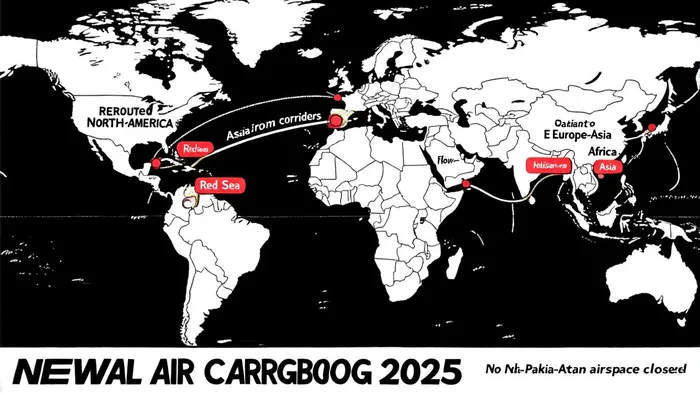

Geopolitical Disruptions Reshape Air Routes

Recent geopolitical tensions have forced a reallocation of air cargo and passenger traffic. U.S. tariff policies have triggered retaliatory measures, shrinking traditional high-volume corridors like Asia–North America while expanding Europe–Asia, intra-Asia, and Africa–Asia routes, according to a Stattimes analysis. Airspace closures-such as those between India and Pakistan, drone sightings over Europe, and military exercises near Russia-have further complicated operations; that analysis also highlighted these operational constraints. Meanwhile, the Red Sea crisis has rerouted maritime and air cargo, increasing shipping times and costs as detailed in a OneUnion Solutions blog. Despite these challenges, global air passenger demand rose 2.6% year-on-year in June 2025, driven by robust international travel, Gulf News reported.

Investment Risks: Supply Chain Vulnerabilities and Regulatory Shifts

The aerospace and logistics industries face heightened risks from geopolitical instability. Protiviti's 2025 report highlights supply chain disruptions, regulatory changes, and trade policy shifts as critical threats. For example, 78% of aerospace and defense firms are prioritizing nearshoring and in-sourcing to mitigate single-source dependencies, according to the report. EY warns that global conflicts and maritime bottlenecks are creating supply chain volatility, particularly in regions like the Red Sea. Additionally, rising defense budgets are pushing companies to invest in advanced technologies like AI-driven drones and cyber defense systems, though this requires significant capital and operational flexibility, as noted in a Dunapress roundup.

Opportunities: Resilience, Innovation, and Strategic Reconfiguration

Amid these challenges, companies are capitalizing on opportunities to build resilience. The adoption of AI, automation, and digital twins in maintenance, repair, and overhaul (MRO) operations is improving efficiency and reducing downtime, according to the Deloitte outlook. Middle Eastern carriers, such as Emirates and Qatar Airways, are uniquely positioned to benefit from geopolitical shifts, as they maintain direct routes to Asia while European airlines face rerouting constraints, an ATPI outlook observes. Furthermore, the surge in air freight demand for time-sensitive goods-like semiconductors and pharmaceuticals-has boosted utilization rates for logistics firms operating in hubs like Dubai and Doha, the Logisym outlook notes.

Case Studies: Lufthansa Cargo and Kuehne+Nagel

A GetTransport piece explains how Lufthansa Cargo exemplifies strategic adaptation, rerouting Asian flights via Dubai and Istanbul to avoid Russian airspace and ensure the safe transport of high-tech goods. The company's use of geopolitical intelligence and partnerships with tech clusters like Silicon Saxony underscores its focus on risk mitigation. Meanwhile, Kuehne+Nagel is leveraging trade turmoil to expand its value-added services, including customs advisory and digital supply chain analytics - the firm reported a 7% year-on-year increase in air freight volumes in the first half of 2025, driven by demand in sectors like semiconductors and cloud infrastructure, according to Kuehne+Nagel.

Financial Outlook: Profitability Amid Uncertainty

Despite challenges, the global airline industry is projected to achieve record revenues in 2025, surpassing $1 trillion, driven by passenger demand and e-commerce growth, IATA projects. IATA forecasts net profits of $36.6 billion for airlines in 2025, supported by lower jet fuel prices and efficiency gains; however, return on invested capital (ROIC) remains below the weighted average cost of capital in many regions, with Europe, the Middle East, and Latin America showing the strongest returns.

Conclusion

The aerospace and logistics sectors in 2025 are at a crossroads, where geopolitical disruptions are both a threat and a catalyst for innovation. Investors must weigh the risks of supply chain volatility and regulatory shifts against opportunities in resilient strategies, technological adoption, and strategic reconfiguration. Companies like Lufthansa Cargo and Kuehne+Nagel demonstrate that agility and foresight can turn uncertainty into competitive advantage. As the industry evolves, a "resilience mindset" will be critical for long-term success, as discussed in a Maersk analysis.

Comentarios

Aún no hay comentarios