Geopolitical Crossroads: Southeast Asia's Infrastructure Boom and Real Estate Opportunities in 2025

Southeast Asia's cross-border infrastructure landscape in 2025 is a battleground of geopolitical influence, where China's Belt and Road Initiative (BRI), India's trilateral highways, and U.S. trade realignment intersect to shape regional trade and real estate dynamics. As nations like Vietnam, Indonesia, and Thailand navigate these competing forces, the region's infrastructure projects are not only reshaping supply chains but also driving a surge in real estate investment-despite lingering uncertainties tied to U.S.-China tensions and territorial disputes.

China's BRI: Connectivity and Controversy

China's BRI remains the dominant force in Southeast Asia's infrastructure development. Projects such as the Thai-Chinese high-speed railway and the China-Laos Railway have transformed cities like Vientiane and Bangkok into commercial hubs, spurring demand for real estate. In Indonesia, the Jakarta-Bandung high-speed rail has enhanced connectivity between Java's economic centers, while the Sihanoukville Port in Cambodia has turned a once-sleepy town into a bustling economic zone, according to a Southeast Asia real estate outlook.

However, these projects are not without risks. Debt sustainability concerns loom large, particularly in Laos and Cambodia, where smaller economies struggle to absorb the financial burden of large-scale infrastructure, according to Asia-Pacific investment data. Political instability further complicates outcomes: Malaysia's East Coast Rail Link (ECRL) has faced multiple renegotiations and suspensions due to shifting governments, while Myanmar's BRI-linked projects remain stalled amid ethnic conflicts, according to a BRI progress analysis.

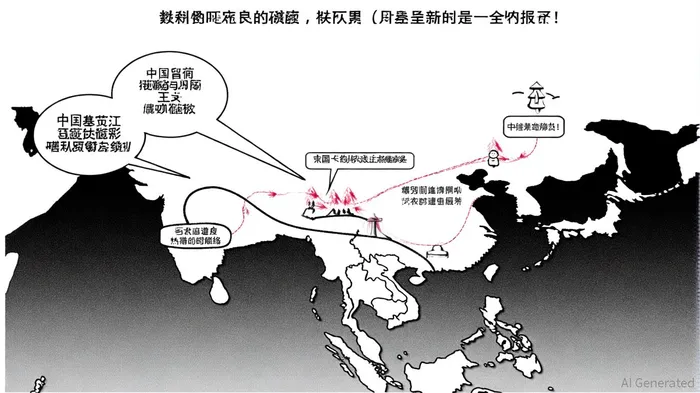

India's Strategic Counterweight

India's India-Myanmar-Thailand Trilateral Highway (IMT-TH) aims to counterbalance China's influence by linking its northeastern states to Southeast Asia. Launched in 2002, the 1,360-km highway is intended to connect Moreh in Manipur to Mae Sot in Thailand, but progress has been hampered by Myanmar's political turmoil. As of 2025, India reports 70% completion of its section, yet ethnic militias control key portions of the route in Myanmar, forcing India to explore alternative diplomatic strategies, according to an ORF analysis.

India's Kaladan Multimodal Transit Transport Project (KMMTTP), which aims to connect India's northeastern states to Sittwe Port in Myanmar, faces similar challenges. While these projects underscore India's commitment to regional connectivity, their success hinges on resolving geopolitical tensions and securing local stakeholder buy-in, as discussed in the ORF analysis.

U.S. Trade Realignment and Real Estate Resilience

The U.S. has recalibrated its trade focus toward Southeast Asia, driven by efforts to reduce dependency on China. This shift has fueled demand for industrial real estate in Vietnam and Thailand, where companies are relocating manufacturing operations under the "China-plus-n" strategy. In 2025, cross-border investment in Asia-Pacific commercial real estate surged to $9.5 billion in Q1 alone, with Japan, Australia, and South Korea emerging as top destinations, according to the ASEAN Center.

Japan's real estate market, for instance, has attracted record investments, including Blackstone's $2.6 billion acquisition of Tokyo Garden Terrace Kioicho-the largest foreign real estate deal in the country's history, according to the ASEAN Center. Meanwhile, Vietnam's industrial parks and logistics hubs are expanding rapidly to accommodate global supply chain diversification, supported by government incentives and rising urbanization, per the Southeast Asia real estate outlook.

Geopolitical Risks and Opportunities

Despite the optimism, geopolitical tensions remain a wildcard. U.S. tariff policies and South China Sea disputes create uncertainty for investors, particularly in export-dependent economies like Vietnam and Japan, according to Asia-Pacific investment data. CBRECBRE-- warns that tariff volatility could reintroduce inflationary pressures, affecting sectors like retail and industrial real estate, a risk highlighted in the ASEAN Center analysis.

Yet Southeast Asia's adaptability offers a counterpoint. Countries are leveraging multilateral frameworks like the Regional Comprehensive Economic Partnership (RCEP) and the Indo-Pacific Economic Framework (IPEF) to diversify trade relationships and mitigate risks, according to the Southeast Asia real estate outlook. Sustainable development is also gaining traction, with over 56% of investors prioritizing green building projects in 2025, per the Southeast Asia real estate outlook.

Conclusion: Navigating the New Normal

Southeast Asia's infrastructure and real estate markets in 2025 reflect a delicate balance between opportunity and risk. While China's BRI and India's trilateral highways drive connectivity, geopolitical tensions and debt sustainability concerns demand cautious investment strategies. For investors, the region's resilience-bolstered by urbanization, supply chain shifts, and sustainability trends-offers compelling long-term prospects, provided they navigate the complex interplay of geopolitics and economics with agility.

Comentarios

Aún no hay comentarios