Galata Acquisition Corp. II's IPO: A Strategic Move in a Resurgent SPAC Market

Galata Acquisition Corp. II's recent $150 million initial public offering (IPO) at $10 per unit[1] reflects a calculated approach to navigating the evolving SPAC landscape. As the market for special purpose acquisition companies (SPACs) shows signs of recovery in 2025, Galata's strategy—targeting energy, fintech865201--, real estate, and technology sectors—positions it to capitalize on investor appetite for innovation and capital efficiency. However, the IPO's success will depend on its ability to balance valuation efficiency with the inherent risks of SPAC structures, particularly in sectors with mixed post-merger performance.

SPAC Valuation Efficiency: StructureGPCR-- and Sector Dynamics

Galata's IPO follows a conventional SPAC model, offering units comprising one Class A ordinary share and one-third of a warrant exercisable at $11.50 per share[1]. The inclusion of a greenshoe option—allowing underwriters to purchase an additional 15% of units—provides flexibility to stabilize pricing, a feature increasingly common in SPAC 4.0 offerings[3]. This structure aligns with broader trends toward smaller, more conservative SPAC deals, as companies seek to mitigate the risks of high redemption rates and post-merger underperformance.

Energy SPACs, a key focus for Galata, have historically exhibited positive abnormal returns at merger announcements but face steep declines in the long term[2]. For instance, energy SPACs saw a 17.89% return in the seven days post-merger announcement but a 5.67% loss at the merger event itself, with further declines observed over the following year[2]. These dynamics underscore the importance of governance and execution. Galata's management team, led by Daniel Freifeld and Craig Perry, brings experience in capital markets, which could enhance credibility with investors wary of speculative SPACs[1].

Fintech and technology SPACs, meanwhile, have shown greater resilience. A 2025 report by Woodruff Sawyer notes that SPACs in these sectors benefit from alignment with digital transformation trends, offering quicker access to public markets compared to traditional IPOs[3]. However, the same report cautions that post-merger performance remains mixed, with average returns across most sectors falling below -50% since 2009[2]. Galata's focus on high-growth sectors could mitigate some of these risks, but investors must remain vigilant about the lack of transparency in SPAC mergers[4].

Investor Timing: Navigating a Cyclical Market

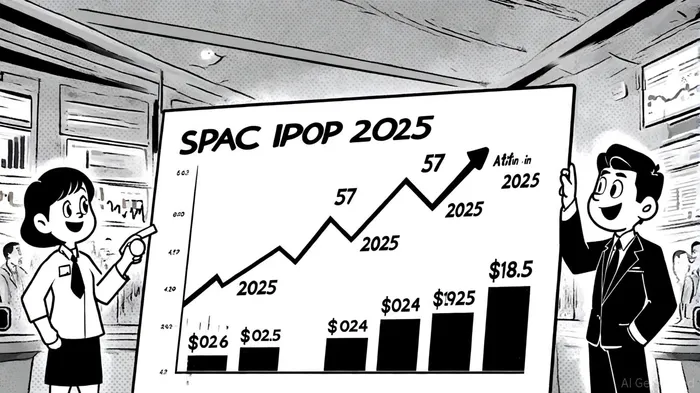

The timing of Galata's IPO—launched on September 19, 2025—coincides with a broader SPAC market rebound. According to SPACAnalytics, 2024 saw 57 SPAC IPOs raising $9.6 billion, while 2025 is projected to reach 90 IPOs and $18.5 billion in proceeds[3]. This resurgence reflects investor demand for alternative capital-raising vehicles, particularly in sectors like energy and technology, where traditional IPOs have struggled due to regulatory uncertainty and market volatility[5].

However, timing is a double-edged sword. Energy SPACs, for example, are sensitive to macroeconomic factors such as interest rates and commodity prices. A 2025 study in Energy SPACs Performance and Governance highlights that foreign CEO origins and weak corporate governance correlate with lower success rates in these SPACs[2]. Galata's management, both U.S.-based, may offer a counterpoint to these risks, but investors should scrutinize the company's prospectus for details on target acquisition criteria and trust fund protections[4].

For fintech and real estate SPACs, timing strategies must also account for sector-specific challenges. Fintech SPACs, while resilient, face regulatory scrutiny and competition from traditional banks[3]. Real estate SPACs, meanwhile, remain vulnerable to high borrowing costs, which could dampen returns for investors seeking stable rental income[2]. Galata's diversified sector focus may help balance these risks, but its ability to execute within the 12- to 18-month merger window—shorter than the traditional 24-month timeline—will be critical[3].

Benchmarking Galata's Strategy

Galata's $150 million IPO size places it in the mid-tier of SPACs, a range that has gained favor in 2025 as sponsors avoid the overhang of large, speculative deals[3]. By comparison, energy SPACs in 2024 averaged $1.2 billion in proceeds, while fintech SPACs typically raised between $3.8x and 7.4x revenue multiples[5]. Galata's smaller size may appeal to investors seeking agility, but it also limits the capital available for post-merger operations—a risk mitigated by the greenshoe option and potential PIPE financing[1].

Valuation metrics further contextualize Galata's approach. While sector-specific P/B and EV/Revenue ratios for 2024-2025 are not publicly available, broader SPAC trends suggest a shift toward conservative valuations. For example, technology SPACs in 2025 traded at an average P/B ratio of 13.09, reflecting investor optimism about growth potential[4]. Galata's $10 unit price, while standard for SPACs, may appear undervalued relative to these metrics, potentially attracting speculative buyers but deterring long-term institutional investors[4].

Conclusion: A Calculated Bet in a Volatile Market

Galata Acquisition Corp. II's IPO represents a strategic bet on the SPAC market's 2025 resurgence, leveraging a diversified sector focus and conservative capital structure. While its pricing aligns with industry norms, the company's success will hinge on its ability to execute a merger within a tight timeframe and navigate sector-specific risks. For investors, the key takeaway is clear: SPACs remain a high-risk, high-reward vehicle, and timing—both in terms of market conditions and management execution—will determine whether Galata's $150 million raise translates into long-term value.

Comentarios

Aún no hay comentarios