Gadang Holdings Berhad: A Cautionary Tale of Declining ROCE and Capital Employed

Gadang Holdings Berhad, a Malaysian conglomerate spanning construction, property development, and utilities, has become a case study in strategic misalignment and capital misallocation. Despite securing high-profile contracts like the RM280 million Klang Valley Data Centre project in 2024[2], the company's financial metrics tell a troubling story: a Return on Capital Employed (ROCE) of 1.5% as of May 2025, far below the Construction industry average of 10%[1], and a 68% decline in ROCE over five years[1]. Meanwhile, capital employed has shrunk by 23% during the same period[1], while the stock price has plummeted 33%[1]. This divergence between operational performance and capital deployment raises urgent questions about long-term value erosion.

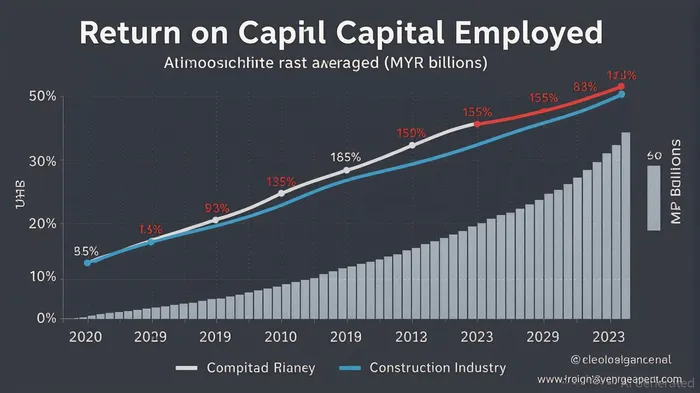

The Erosion of ROCE: A Systemic Decline

ROCE measures a company's efficiency in generating profits from its capital. For Gadang, the metric has deteriorated sharply: from 5.0% in 2020 to 1.5% in 2025[1], despite a modest increase in revenue and net income in Q3 2025 (79% and 40% year-on-year, respectively)[3]. This suggests that while top-line growth is occurring, it is not translating into meaningful returns. The company's net profit margin of 1.3%[2] and earnings decline of -31% annually[2] further underscore operational inefficiencies.

The root cause lies in capital allocation. Gadang's capital employed—calculated as total assets minus current liabilities—has contracted by 23% over five years[1], yet ROCE has fallen at a steeper rate. This implies that the company is not only shrinking its capital base but also failing to deploy it effectively. For context, the Construction industry's earnings have grown at 23.2% annually[2], highlighting Gadang's inability to compete on operational efficiency.

Strategic Capital Allocation: A Missing Link

Gadang's business segments—civil engineering, property development, mechanical/electrical engineering, and utilities—suggest a diversified approach[4]. However, the company's capital allocation decisions remain opaque. While it secured the Klang Valley Data Centre contract[2] and expanded subsidiaries like Alpha IVF Group and Ancom Nylex[5], these initiatives lack transparency in terms of capital deployment. For instance, Alpha IVF's planned fertility centres in Johor and Sabah[5] and Ancom Nylex's MSMA plant expansion[5] could theoretically drive growth, but there is no data on how these projects align with ROCE improvement.

The absence of recent investments or divestitures post-2024[6] is equally concerning. In a competitive sector like Construction, where margins are razor-thin, companies must reinvest profits into high-return projects or divest underperforming assets. Gadang's lack of such activity—coupled with its declining ROCE—suggests a failure to prioritize capital-intensive initiatives that could reverse its downward trajectory.

Mixed Signals and Investor Caution

While Q3 2025 results showed a 40% year-on-year increase in net income[3], the profit margin contraction from 4.6% to 3.6%[3] indicates cost pressures or pricing challenges. This duality—growth in absolute terms but declining margins—reflects a fragile recovery. Investors must also consider the broader context: a stock price drop of 44% over five years[3] and a net loss of MYRMYRG-- 29.32 million in FY 2023, followed by a narrow MYR 4.71 million profit in FY 2024[2]. These swings suggest inconsistent earnings and a lack of sustainable value creation.

Implications for Long-Term Value

Gadang's trajectory exemplifies how poor capital allocation can erode shareholder value. A 68% decline in ROCE[1] and 23% reduction in capital employed[1] signal that the company is not only shrinking its asset base but also failing to generate returns commensurate with its risk. For investors, this raises red flags:

1. Capital Misallocation: Without clear evidence of reinvestment in high-ROCE projects, the company risks perpetuating its underperformance.

2. Strategic Ambiguity: The absence of post-2024 capital decisions[6] leaves uncertainty about management's ability to adapt to industry trends.

3. Valuation Risks: A 33% stock price decline[1] over five years reflects market skepticism, which could deepen if ROCE trends persist.

Conclusion

Gadang Holdings Berhad's declining ROCE and capital erosion are not mere financial anomalies—they are symptoms of a deeper strategic failure. While recent contracts and subsidiary expansions offer glimmers of hope, the lack of transparent capital allocation and persistent operational inefficiencies paint a cautionary picture. For investors, the lesson is clear: without a coherent strategy to redeploy capital toward high-return opportunities, even short-term gains will be insufficient to reverse long-term value destruction.

Comentarios

Aún no hay comentarios